Standing at an airport bureau de change, watching the board flash numbers that seem disconnected from anything you’ve seen online, is one of the most reliably confusing moments of any holiday. Plenty of UK travellers hand over their pounds without truly understanding what rate they are receiving or why it differs so dramatically from what Google showed them moments before. That gap in understanding costs real money. This guide decodes the essential exchange rate terminology, from currency pairs and spreads to DCC and forward rates, so you can walk into any exchange knowing exactly what you are paying for and where the value lies.

Table of Contents

- Understanding basic exchange rate terminology

- The rates behind the rates: bid, ask, and the spread

- Spot, forward, and cross rates: what do they mean for your trip?

- Other essential terms: regime, pip, spread, and the retail catch

- Why knowing the terminology truly pays off

- Find and compare the best travel money rates

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Master core terms | Learning the basics like base/quote currency and spread helps you understand what you’re really getting. |

| Compare against mid-market | Always check provider rates against the mid-market rate to avoid hidden markups. |

| Avoid common traps | Decline DCC, watch for weekend fees, and make larger ATM withdrawals to save money. |

| Small details add up | Ignoring minor terms or markups can cost more than choosing the wrong provider. |

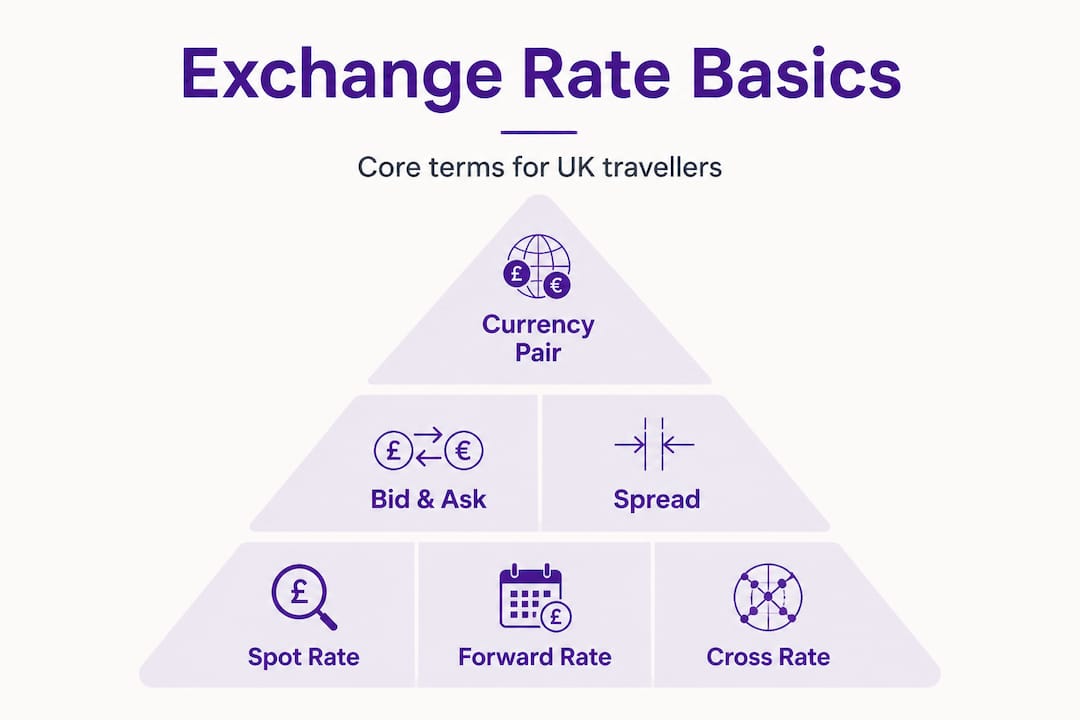

Understanding basic exchange rate terminology

Every rate you see displayed, whether on a board at Gatwick, a website, or a bank app, is built on a small set of core concepts. Learn these and everything else starts to make sense.

The most fundamental idea is the currency pair. Exchange rates are quoted as currency pairs with a base currency and a quote currency. The base currency is the first one listed, and the quote currency is the second. So in GBP/EUR, British pounds (GBP) is the base and euros (EUR) is the quote. A rate of GBP/EUR 1.17 means one pound buys 1.17 euros.

For UK travellers, GBP will usually be the base currency, because you are starting with pounds. But you will also see pairs listed the other way around, such as EUR/GBP, which tells you how many pounds one euro costs. It sounds simple, but flipping the pair is one of the easiest ways to misread a rate and assume you are getting more than you actually are.

Direct vs indirect quotes is another concept worth pinning down. A direct quote tells you how much of your home currency you need to buy one unit of the foreign currency. An indirect quote flips that, showing how many foreign units one pound buys. Most UK sites show indirect quotes (GBP/EUR 1.17 means your pound buys 1.17 euros), which is generally the more intuitive format for holidaymakers.

Cross rates matter when you are travelling somewhere outside the major pairs. If you are heading to Thailand and the market has no direct GBP/THB price, providers calculate the rate via a third currency, usually USD. This intermediate step can introduce an extra margin, making the market exchange rate basics slightly less favourable than you might expect.

Here are the currency pairs most commonly relevant for UK travellers:

- GBP/EUR (Eurozone: France, Spain, Italy, Greece, Portugal)

- GBP/USD (USA, and widely accepted in the Caribbean)

- GBP/TRY (Turkey)

- GBP/THB (Thailand)

- GBP/AED (UAE and Dubai)

- GBP/MXN (Mexico)

- GBP/AUD (Australia)

The table below shows a simplified example of how the same £500 converts differently depending on the base/quote direction:

| Pair displayed | Rate shown | What you receive for £500 |

|---|---|---|

| GBP/EUR (indirect) | 1.1700 | €585.00 |

| EUR/GBP (direct) | 0.8547 | Costs £500 to buy €585.00 |

| GBP/USD (indirect) | 1.2700 | $635.00 |

Seeing both presentations on different platforms and understanding they refer to the same rate is genuinely useful for avoiding confusion.

The rates behind the rates: bid, ask, and the spread

Now that you know the lingo, let’s look closer at the numbers that shape what you’ll really pay and how providers profit from every transaction.

When you look at a live rate, you are actually seeing two prices layered on top of each other. Bid and ask rates, spread, and mid-market rates are what providers actually use, while retail customers receive marked-up rates that quietly pad the provider’s revenue.

The bid rate is what the provider will pay you to buy your foreign currency back. The ask rate (also called the sell rate) is what you pay to purchase foreign currency from them. The spread is the gap between those two numbers. That gap is the provider’s margin.

The mid-market rate sits exactly halfway between the bid and ask on the wholesale market. It is the figure Google and XE display. It is also almost never the rate a traveller receives. Think of it as a benchmark, not a shopping price. Knowing it lets you measure how much any given provider is marking up their rates.

“Retail exchange rates are always a reflection of wholesale markets, with additional margins layered on for risk, operations, and profit. The wider the spread, the more the provider earns from each transaction.”

In practice, why retail rates differ from the mid-market rate depends heavily on who is offering the exchange. Banks typically add 3 to 5% on top of the mid-market rate. Specialist currency providers on the high street or online generally charge 0.5 to 2%. Fintech apps and digital-first services often charge 0 to 1%, though sometimes with a small flat fee or a weekend surcharge.

| Provider type | Typical markup over mid-market | On £1,000 exchanged |

|---|---|---|

| Airport bureau de change | 5-10% | £50-£100 lost |

| High street bank | 3-5% | £30-£50 lost |

| High street specialist | 1-2% | £10-£20 lost |

| Online specialist | 0.5-1.5% | £5-£15 lost |

| Fintech app | 0-1% | £0-£10 lost |

The differences are stark. Exchanging £1,000 at an airport versus an online specialist could easily cost you £60 to £80 more, money that could cover a decent meal abroad. Checking Currency Club rates alongside other providers before you travel is one of the most straightforward ways to see these differences side by side.

Pro Tip: Before committing to any exchange, pull up the mid-market rate on Google or XE for your pair, then compare it to the rate being offered. The difference, expressed as a percentage, is your true cost. Anything above 2% deserves scrutiny.

Spot, forward, and cross rates: what do they mean for your trip?

Understanding retail and wholesale rates helps, but trips often raise questions about changing rates over time or obscure currency combinations.

Three terms come up regularly in any deeper reading about exchange rates: spot, forward, and cross.

The spot rate is the rate available right now, for immediate (or near-immediate) delivery. Spot rate is for immediate delivery, forward rate is for future delivery, and cross rates use a third currency as an intermediary step to reach the final pair. For the vast majority of UK holidaymakers, the spot rate is the only one that matters. When you buy euros today for a trip next month, you are still buying at the spot rate available when you make the transaction.

The forward rate is a price agreed today for currency delivered at a future date. This is primarily a tool for businesses managing foreign currency risk, such as an importer wanting to lock in costs on goods paid for in dollars three months from now. Most travellers will never need a forward contract, but knowing the term means you will not be confused if a provider or financial article mentions it.

Forward premiums and discounts, which describe whether the forward rate is higher or lower than the current spot, can offer a loose signal about where markets expect rate timing to impact your budget over time. If you are taking an extended trip of several months, monitoring these signals might inform whether to exchange more currency earlier.

Here is when each rate type actually matters in practice:

- Spot rate: Every standard travel money purchase, ATM withdrawal, or card transaction abroad

- Forward rate: Large international transfers, business currency hedging, long-term property purchases abroad

- Cross rate: Purchasing less common currencies like the Thai Baht, Indonesian Rupiah, or Moroccan Dirham, where providers route via USD

One practical implication of cross rates is that they can slightly widen the margin you pay. If your provider converts GBP to USD internally and then USD to THB, there are two points at which a spread is applied. Asking a provider whether they quote directly or via a cross rate is a legitimate question when exchanging less common currencies in larger amounts.

Other essential terms: regime, pip, spread, and the retail catch

Now we have tackled the big terms, let’s cover the extra jargon and traps that catch out even experienced travellers.

Exchange rate regimes describe how a country manages its currency. A floating exchange rate, like GBP, moves freely based on market supply and demand. A fixed (or pegged) rate, such as the Hong Kong Dollar (HKD) tied to the USD, stays within a narrow band by government or central bank action. A managed float sits in between, where a currency broadly floats but authorities intervene to prevent excessive volatility. Floating, fixed, and managed float regimes, along with pips and DCC, all affect what travellers ultimately pay at the point of exchange.

Understanding regime types helps explain why some currencies appear stable (the UAE Dirham almost never shifts against the dollar) while others, like the Turkish Lira, can move substantially within a single week. If you are travelling to a country with a volatile floating currency, timing your exchange or buying in tranches can reduce exposure.

A pip is the smallest unit of movement in an exchange rate, typically the fourth decimal place. Moving from 1.1700 to 1.1705 is a 5-pip change. For regular holiday spending, individual pips rarely matter in isolation. But if you are exchanging a larger sum, say £5,000 or more, even a 10-pip difference in rate can result in a meaningful variation in what you receive.

Dynamic Currency Conversion (DCC) is one of the most common and costly traps for UK travellers. When you pay by card at a foreign retailer or withdraw from a foreign ATM, you may be offered the option to pay in pounds rather than local currency. This sounds reassuring. It is not. DCC allows the foreign bank or merchant’s payment processor to apply their own exchange rate, and that rate typically includes a 3 to 7% markup on top of what your own card provider would charge. Always decline DCC. Always pay in local currency. There are no exceptions where DCC works in your favour.

Weekend and holiday markups are another lesser-known cost. Because wholesale currency markets are closed on weekends, fintech providers and some card issuers buffer against potential Monday rate movements by adding 0.5 to 1% to weekend transactions. If possible, make large exchanges or card-linked conversions on weekdays.

The main traps to watch for include:

- DCC: Offered at foreign ATMs and card terminals; always decline

- Weekend markups: 0.5-1% added by some cards and fintechs on Saturdays and Sundays

- Poor ATM rates: Local ATMs operated by foreign banks may quote low rates and charge flat fees

- Small, frequent withdrawals: Each withdrawal may carry a flat fee, making 10 small withdrawals far more costly than two larger ones

- Airport bureaux: Convenience comes at a serious price, often 5-10% above mid-market

Pro Tip: When using an ATM abroad, always choose to be charged in the local currency, and withdraw larger amounts less frequently to minimise flat fees. Knowing how to avoid travel rate traps and reviewing currency exchange options before you leave will save you far more than any last-minute deal at the departures terminal.

Why knowing the terminology truly pays off

Most travel money guides focus on the headline: “don’t exchange at the airport.” That is correct but incomplete. The travellers who consistently get good rates are not just avoiding one bad venue. They understand the mechanics well enough to spot a poor deal anywhere.

Here is the uncomfortable truth. The biggest losses rarely come from one obvious rip-off. They accumulate quietly. A DCC charge here. A weekend markup there. A cross-rate margin on a less common currency. Individually, each feels trivial. Together, across a two-week trip with multiple transactions, they can easily add up to £50, £80, or more in avoidable costs.

Most guides also focus heavily on provider comparison, which matters, but they underplay the role of understanding terms. If you do not know what a spread is, you cannot properly evaluate a “zero commission” claim. If you do not understand DCC, a prompt at an ATM will catch you off guard regardless of which card you are holding. The terminology is not academic. It is operational.

There is also a confidence dividend. Knowing the terms means you are not intimidated by the jargon providers use. You can ask direct questions: “What is your rate versus mid-market?” or “Is that a direct rate or via USD?” Those questions often result in better service and, occasionally, a slightly better rate. Providers know when a customer understands what they are looking at.

Understanding the best rates for travellers begins with understanding the language of exchange, not just the numbers on a board.

Find and compare the best travel money rates

Armed with this knowledge, here is how you can use trusted resources to get the best deal for your next holiday.

Knowing the terminology only takes you so far. The next step is putting it into action by comparing live rates before you commit to any exchange.

CompareTravelCash.co.uk lets you compare travel cash rates from multiple providers in one place, so you can see immediately who is offering the closest rate to mid-market for your chosen currency. Rather than checking individual provider sites or trusting a bureau de change board, you get a transparent side-by-side view that includes both the rate and any associated fees. You can also review specific provider rates such as Hays Travel rates or explore multi-currency card deals if you prefer the flexibility of loading money onto a prepaid card before you go. Spending five minutes comparing before you travel could save you more than the cost of airport parking.

Frequently asked questions

What is the mid-market rate and why can’t I get it?

The mid-market rate is the true midpoint between wholesale buy and sell prices; retail customers rarely receive it because providers add a markup to cover profit and operational risk.

How do I know if I’m getting a bad exchange rate?

Compare the provider’s offered rate against the current mid-market rate and factor in any fees; typical markups are 3 to 5% at banks, 0.5 to 2% at specialists, and 0 to 1% at fintechs.

Should I use DCC when offered abroad?

No. Always pay in local currency because DCC adds 3 to 7% extra to your transaction, benefiting the foreign merchant’s payment processor rather than you.

What does ‘pip’ mean in exchange rates?

A pip is the smallest unit of rate movement, usually the fourth decimal place; for example, a shift from 1.1000 to 1.1005 represents a 5-pip change.

Will weekend markups really cost me more?

Yes. Some cards and providers apply a 0.5 to 1% weekend surcharge, meaning on a £1,000 exchange you could pay £5 to £10 more simply because of the day you transact.