Prepaid currency cards are one of the most misunderstood travel money tools available to UK holidaymakers. Many travellers assume they work like a credit card abroad, or that they are simply a rebranded debit card. Neither is true. Understanding what is a prepaid currency card, how it actually functions, and where it fits within your travel money plan can save you real money and genuine stress before you leave home. This guide covers everything you need to know, from the basics of how prepaid currency works to the fees, protections, and practical tips that make the difference between a smooth trip and an expensive lesson.

Table of Contents

- What is a prepaid currency card and how does it work?

- Key benefits for travellers

- Prepaid cards vs other payment options

- How to use prepaid currency cards effectively

- Fees, restrictions, and security

- My honest take on prepaid currency cards

- Compare prepaid currency cards with Comparetravelcash

- Frequently asked questions

What is a prepaid currency card and how does it work?

A prepaid currency card is a stored-value payment card that you load with money before you spend it. There is no credit facility attached. No borrowing, no monthly billing, and no interest charges. You load funds onto the card, and you spend from that balance. When the balance runs out, the card simply declines until you top it up again.

Loading money onto the card is straightforward. Most issuers allow you to do this via a linked app, online portal, or bank transfer. Once loaded, you can use the card at any payment terminal that accepts Visa or Mastercard, which covers most retailers, restaurants, and ATMs worldwide.

The key mechanics to understand:

- Spend limit tied to balance. You can only spend what you have loaded. No overdrafts, no hidden credit.

- Reloadable. Unlike a single-use prepaid gift card, travel prepaid currency cards can be topped up multiple times throughout your trip.

- Transaction authorisation. Every payment draws directly from your loaded balance. If insufficient funds are available, the transaction is declined.

- Multi-currency wallets. Many cards let you hold and spend in different currencies from a single card, converting at rates set when you load.

Pro Tip: Load your card a day or two before departure. This gives you time to spot any issues with the activation process and confirm the balance is showing correctly before you land.

The simplicity of this model is exactly what makes it appealing. You know precisely how much you have, and the card will never let you spend beyond it.

Key benefits for travellers

The benefits of prepaid currency cards extend well beyond convenience. Here is where they genuinely stand out.

Security without exposure. A prepaid currency card is not linked to your main bank account. If the card is lost or stolen abroad, a thief cannot access your savings or current account. You report it, freeze it through the app, and the damage is limited to whatever remains on the card balance. For anyone who has ever experienced card fraud abroad, this separation is worth a great deal.

Budget control from day one. Because transactions require sufficient funds and no credit is available, the card enforces your spending limit naturally. This is particularly useful for families travelling with teenagers or for travellers who know they overspend when a bank account feels abstract.

Multi-currency support. The better travel cards on the market support multiple currencies simultaneously. Some cards support up to 22 currencies, allowing you to hold Euros, US Dollars, and Thai Baht at the same time without needing separate cards or accounts. This is the core appeal of the multi currency prepaid card for frequent or multi-destination travellers.

Rate locking. When you load a currency at a specific rate, that rate is locked in. If the pound weakens after you load, you are protected. This is a meaningful advantage over paying with a debit card abroad, where the exchange rate applied at the point of sale is entirely out of your control.

- Contactless and mobile wallet compatibility. Most travel prepaid cards support contactless payments, Apple Pay, and Google Pay, so day-to-day spending abroad feels no different from at home.

- No credit impact. Using a prepaid card has zero effect on your credit score, which matters if you are planning a mortgage application or other credit event around your travel dates.

Pro Tip: If you are travelling across Europe and the US on the same trip, load both currencies before you leave. Exchange rates at airports and foreign ATMs are almost always worse than rates you can secure in advance.

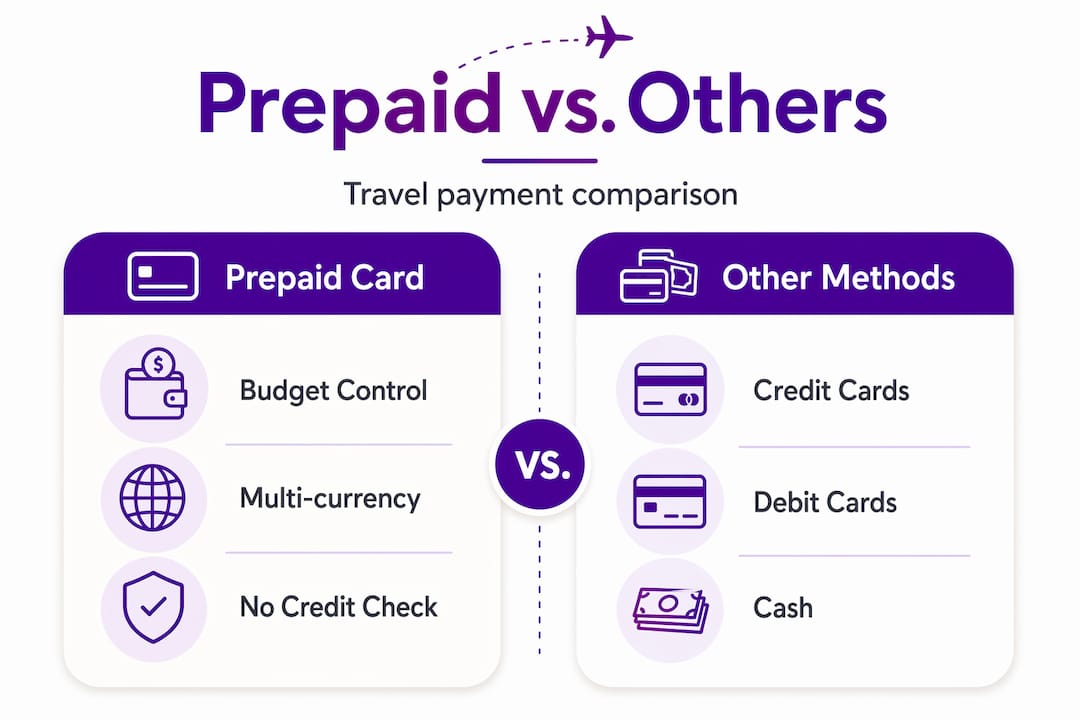

Prepaid cards vs other payment options

Understanding where prepaid currency cards sit relative to your other options helps you use them strategically rather than replacing everything blindly.

| Payment method | Linked to bank account | Credit extended | Affects credit score | Accepted worldwide | Rate control |

|---|---|---|---|---|---|

| Prepaid currency card | No | No | No | Yes (Visa/MC) | Yes, at load |

| Debit card | Yes | No (usually) | No | Yes | No |

| Credit card | No | Yes | Yes | Yes | No |

| Secured credit card | Deposit held | Yes | Yes | Yes | No |

| Cash | N/A | No | No | Widely | Varies by source |

The distinction between prepaid cards and secured credit cards catches many people out. A secured credit card requires a deposit but still extends credit, still appears on your credit file, and still carries the risk of debt if you do not pay the balance. Prepaid cards don’t report to credit bureaus at all. They are entirely separate from the credit ecosystem.

Debit cards are the closest comparison. Both spend real money you already have. The critical difference is that your debit card is a direct window into your bank account. One fraudulent transaction on a debit card can drain your account immediately. A prepaid card contains only the funds you placed on it.

Cash still has its place, particularly in rural areas, local markets, and countries with lower card acceptance. But cash offers zero fraud protection and no ability to freeze or recover funds. For the travel cash vs currency card question, the practical answer for most travellers is: carry some cash as a backup, and use a prepaid card as your primary spending tool.

Credit cards offer stronger consumer protections under Section 75 of the Consumer Credit Act, which is worth considering for large purchases. For everyday travel spending, the risk of accumulating debt or paying foreign transaction fees typically outweighs that benefit.

How to use prepaid currency cards effectively

Getting the most from your prepaid travel card comes down to preparation and awareness. Follow these steps before and during your trip.

-

Choose the right card for your destinations. Not all prepaid cards support all currencies. Check which currencies the card holds natively before buying. Spending in an unsupported currency triggers a conversion fee that can erode your savings quickly.

-

Load more than you think you will spend. Incidental holds for hotel deposits or car rental guarantees can temporarily freeze a portion of your balance. A hotel might place a £200 hold that sits on the card for several days. If your balance is too tight, genuine spending can be declined.

-

Manage currencies in the app. Most multi currency prepaid card providers offer an app that shows each currency wallet separately. Use it. Monitor balances in real time so you are never caught short at a restaurant or taxi rank.

-

Check ATM withdrawal terms before travelling. Many prepaid cards allow free ATM withdrawals up to a monthly limit, after which fees apply. Knowing your limit helps you plan whether to withdraw a larger amount in one go rather than making multiple trips.

-

Understand the inactivity fee. If you leave a balance on the card after returning home and do not use it for several months, some providers charge a monthly inactivity fee. Either spend the balance, transfer it back, or sell your leftover currency rather than letting fees chip away at it.

-

Know your card’s fraud process before you need it. If the card is lost or stolen, checking issuer safeguards ahead of time means you know exactly which number to call and how quickly a replacement can be issued.

Pro Tip: When hiring a car abroad, consider using a credit card for the deposit and your prepaid card for all other spending. Rental companies often require a credit card for the excess hold, and using a prepaid card for that purpose can leave your balance uncomfortably restricted.

Fees, restrictions, and security

A prepaid currency card can save you money. It can also cost you money if you are not paying attention to the fee schedule. Here is what to watch for.

- Loading fees. Some providers charge a percentage or flat fee each time you add funds. Compare these rates before committing to a card.

- ATM withdrawal fees. Free withdrawals are often capped at a monthly amount, typically around £200 to £500 depending on the provider. Withdrawals beyond that incur a fee per transaction.

- Currency conversion fees. If you spend in a currency your card does not hold natively, a conversion markup applies. This is the equivalent of the hidden exchange rate margin charged by banks. Understanding currency conversion fees before you travel is worth the ten minutes it takes.

- Inactivity fees. Typically charged after 12 months of no card activity. The amount varies by provider.

- Replacement card fees. If your card is lost abroad, some providers charge for express delivery of a replacement.

On the security side, most travel prepaid cards include chip and PIN, contactless payments, and one-time passcodes for online transactions. Regulatory protections like the CFPB Prepaid Accounts Rule in the US mandate fee disclosures and error resolution rights, and similar frameworks exist in the UK under the Payment Services Regulations. If a transaction on your prepaid card is disputed, you have formal channels to pursue a resolution through your card issuer.

My honest take on prepaid currency cards

I have watched a lot of travellers make the same mistake with prepaid currency cards. They buy one at the airport on the day of departure, load it with just enough to cover what they expect to spend, and then wonder why the card keeps declining. The card works exactly as designed. The problem is the planning, not the product.

In my view, a well-chosen multi currency prepaid card is one of the best travel tools available for UK holidaymakers. The security benefit alone justifies it. Knowing that a pickpocket in Barcelona or a skimmer in Bangkok can only access the £300 on your card rather than everything in your current account is genuinely reassuring.

What I see misunderstood most often is the rate-locking feature. Travellers load a card and assume the rate they got is automatically the best available. It may not be. Rates at loading vary between providers, sometimes quite significantly. The smart move is to compare rates at the point of loading, not just compare cards at the point of purchase.

I would also push back on the idea that prepaid cards are only for budget travellers or those with poor financial discipline. They suit anyone who wants clean separation between travel spending and home finances. That is good practice regardless of how much you earn.

— Jason

Compare prepaid currency cards with Comparetravelcash

Finding the right prepaid travel card means looking beyond the headline features and comparing the actual rates and fees you will pay.

Comparetravelcash makes it straightforward to compare prepaid currency cards from multiple UK providers in one place. You can see the exchange rates on offer, the fee structures, and the currencies supported, so you are choosing based on real numbers rather than marketing copy. If you are still weighing up whether a prepaid card or cash suits your trip better, the best value travel currency guide on the site walks through the decision clearly. You can also compare currency buyback rates for any leftover foreign currency when you return. The comparison tools are free, updated regularly, and built specifically for UK travellers planning trips where every pound counts.

Frequently asked questions

What is a prepaid currency card?

A prepaid currency card is a stored-value card loaded with money before use. You spend from the loaded balance only, with no credit extended and no link to your bank account.

How does a multi currency prepaid card work?

A multi-currency card holds separate currency wallets on a single card, allowing you to load and spend in multiple currencies at rates locked when you load, rather than at the point of sale.

Do prepaid currency cards affect my credit score?

No. Prepaid cards do not report activity to credit reference agencies and do not affect your credit score in any way, unlike secured credit cards which do.

What fees should I watch for on a prepaid travel card?

The main fees to check are loading fees, ATM withdrawal fees beyond any free allowance, currency conversion fees for unsupported currencies, and monthly inactivity fees after extended periods without use.

Is a prepaid travel card safer than a debit card abroad?

Yes, for most purposes. Because a prepaid card is not linked to your main bank account, any loss or fraud is contained to the card balance only, which cannot be said for a standard debit card.