Local currency is defined as the official legal tender issued by a nation’s central bank for use within its own borders, covering wages, taxes, and everyday purchases. For travellers heading to Thailand, Turkey, or the United States, understanding what local currency means is the difference between spending confidently and losing money to avoidable fees. Students moving abroad and expats managing monthly finances face the same challenge. This guide explains how local currency works, why paying in it matters, and how to handle it without getting caught out.

What is local currency and how is it defined?

Local currency is the primary medium of exchange within a specific country. Every transaction you make in that country, from buying a coffee in Bangkok to paying rent in Barcelona, is priced in the local currency. The Thai Baht, the Euro, the US Dollar, and the Turkish Lira are all examples of local currencies within their respective territories.

The term is sometimes used loosely, so the standard industry term is worth knowing: legal tender. Legal tender is the currency a government has officially designated for settling debts and financial obligations. When a shop in Japan prices goods in Japanese Yen, that is the legal tender at work. Local currency also serves as the standard unit for contracts, ensuring all parties in a transaction agree on the same denomination.

There is a second, narrower meaning of “local currency” that applies to community schemes. Alternative currencies such as LETS (Local Exchange Trading Systems) or time-banks circulate within small geographic areas to stimulate local trade when national currency is scarce. These are not backed by a central government. For most travellers and expats, however, local currency simply means the official national currency of the country they are visiting or living in.

How does local currency work with exchange rates?

Exchange rates determine how much of one currency you receive in exchange for another. The global foreign exchange market operates 24 hours a day and sets these rates based on supply and demand. Several factors push rates up or down:

- Interest rates: Higher interest rates attract foreign investment, which increases demand for the local currency and raises its value.

- GDP growth: A growing economy signals strength, which tends to support a stronger currency.

- Political stability: Uncertainty or instability causes investors to move money out of a currency, weakening it.

- Inflation: High inflation erodes purchasing power and typically weakens the local currency over time.

Exchange rate regimes also vary by country. Some currencies are free-floating or fixed, meaning their value is either set by market forces or pegged to a major currency like the US Dollar by a central bank. The Hong Kong Dollar, for example, is pegged to the USD. The British Pound floats freely. Understanding this distinction matters because a pegged currency is more predictable, while a floating one can shift significantly between the day you book a trip and the day you land.

For travellers, currency fluctuations affect your travel budget directly. A weaker pound means your spending money buys less abroad. A stronger pound means the opposite. Monitoring rates before you travel gives you a real advantage.

Why is paying in local currency important when abroad?

Paying in local currency is almost always the cheaper option when you are abroad. Card networks such as Visa and Mastercard set exchange rates for card transactions, and your bank may then add its own markup on top. Those markups can range from 1% to 5% above the mid-market rate. That is a meaningful cost on a two-week holiday.

The trap most travellers fall into is called Dynamic Currency Conversion (DCC). This happens when a card terminal abroad offers to charge you in your home currency rather than the local one. It sounds convenient, but the merchant or their bank sets the conversion rate, and it is almost always worse than what your card network would apply. Always choose to pay in local currency when given the option.

Here is a practical checklist for avoiding unnecessary costs when paying abroad:

- Always select local currency at card terminals when prompted to choose between currencies.

- Use a card with no foreign transaction fees to avoid the standard 2–3% charge many UK banks apply.

- Withdraw cash from bank ATMs rather than independent cash machines, which often add their own fees.

- Avoid airport exchange booths for large amounts. Their rates are consistently worse than high street or online providers.

- Check your bank’s fee schedule before you travel so there are no surprises on your statement.

Pro Tip: If an ATM abroad asks whether you want to “lock in” the exchange rate or be charged in your home currency, always decline. Accepting means the ATM operator sets the rate, not your bank.

What are the economic and practical roles of local currency?

Local currency is a tool of economic sovereignty. A nation’s ability to manage its own interest rates and money supply depends on controlling its own currency. Without that control, a government cannot respond to inflation, unemployment, or recession on its own terms.

The contrast between strong and weak currency positions is stark. Countries that can borrow internationally in their own local currency have far more flexibility. Those that cannot face what economists call “original sin.” Emerging market economies often cannot borrow from international lenders in their own currency and are forced to issue debt in US Dollars or Euros. If their local currency then depreciates, the cost of repaying that debt rises sharply. This is a systemic risk that has triggered financial crises in several developing economies.

The table below compares local currency and reserve currency characteristics at a glance:

| Feature | Local currency | Reserve currency (e.g. USD, EUR) |

|---|---|---|

| Issuing authority | National central bank | Major economy central bank |

| Primary use | Domestic transactions, wages, taxes | International trade, debt, reserves |

| Exchange rate risk | Higher for emerging markets | Lower, widely accepted globally |

| Monetary policy control | Full, if freely issued | Limited for countries using it |

| Borrowing flexibility | High for developed nations | Dependent on issuer’s policy |

Pro Tip: When living abroad as an expat, keep track of whether your salary is paid in local currency or your home currency. A salary in local currency protects you from exchange rate swings on day-to-day spending, but exposes you if you are sending money home regularly.

How travellers, students, and expats can manage local currency effectively

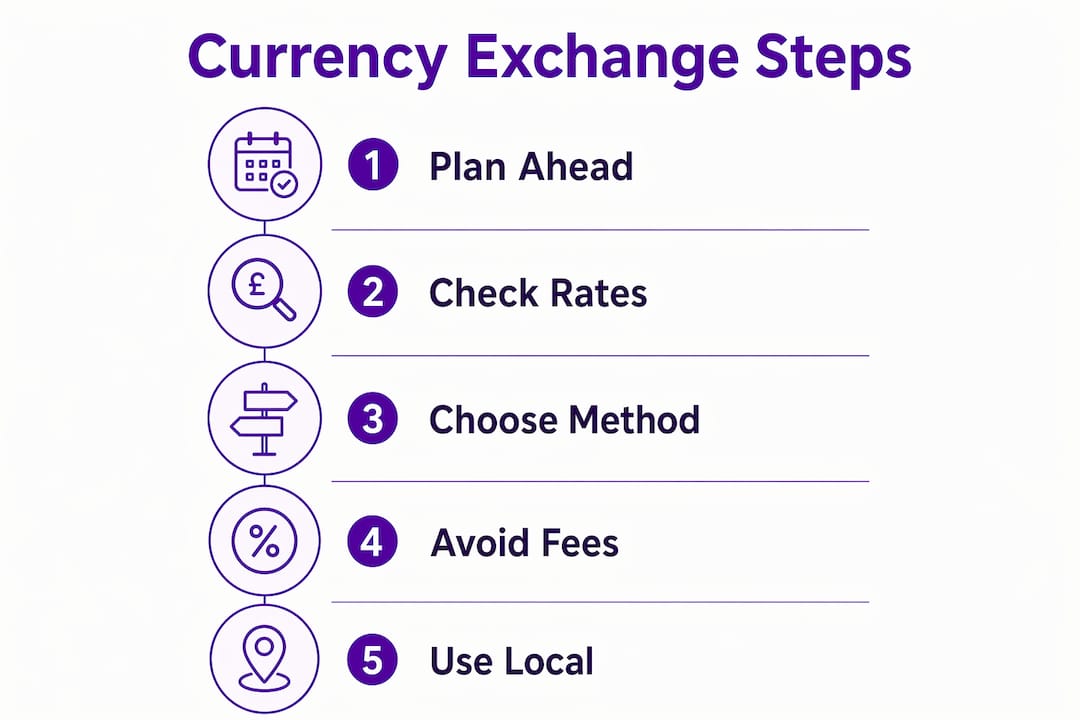

Getting local currency at a fair rate requires planning. Leaving it to the airport or the hotel desk is the most expensive approach. Here are the most effective strategies:

- Order currency online before you travel. Online travel money providers typically offer rates closer to the mid-market rate than high street branches or airports. Comparetravelcash lets you compare travel money rates from multiple UK providers in one place.

- Use a prepaid currency card. These cards let you load a set amount of foreign currency at a fixed rate before you travel. They protect you from rate fluctuations during your trip and are widely accepted. Prepaid currency cards are particularly useful for students and expats managing a fixed monthly budget abroad.

- Monitor exchange rates in advance. Rates shift daily. Setting a rate alert means you can buy currency when the rate is in your favour rather than scrambling at the last minute.

- Understand the mid-market rate. This is the midpoint between the buy and sell rates on the global forex market. Any rate you are offered will include a markup above this. The smaller the markup, the better the deal.

- Sell unused currency back after your trip. Many UK providers offer buyback services. Rates vary, so comparing them before you hand over your leftover notes saves money.

Understanding how currency fluctuations affect travellers is also worth your time if you travel regularly or live abroad. Rate movements of even 5–10% over a few months can significantly change what your money is worth on the ground.

Pro Tip: For longer stays abroad, consider opening a local bank account in the destination country. It removes card fees entirely for day-to-day spending and gives you access to local currency at interbank rates.

What I have learned about local currency after years of watching travellers get it wrong

Most people treat currency exchange as an afterthought. They land, find the nearest ATM or exchange booth, and accept whatever rate appears. That approach costs real money, and the frustrating part is that the better options are not complicated.

The single most common mistake I see is accepting Dynamic Currency Conversion at a card terminal. The merchant’s rate is almost always worse than the card network rate, yet the prompt is designed to look helpful. Saying no takes one second and can save you several pounds per transaction.

The second mistake is conflating “convenient” with “cheap.” Airport bureaux de change are convenient. They are not cheap. The spread between their buy and sell rates is often the widest you will find anywhere. If you need cash on arrival, withdraw a small amount from an airport ATM using a fee-free card, then exchange the bulk of your money through a better provider once you are settled.

For expats, the stakes are higher. If your income is in local currency but your mortgage or savings are back in the UK, you are exposed to exchange rate risk every month. Tracking currency value changes and using forward contracts or rate alerts can protect your finances in ways that reactive exchanging never will.

The travellers who manage their money best are not financial experts. They are simply the ones who plan ahead, compare rates, and pay in local currency every time.

— Jason

Get the best rates on local currency with Comparetravelcash

Knowing what local currency is only gets you so far. Acting on that knowledge before you travel is where the real savings happen.

Comparetravelcash compares travel money rates from providers across the UK, so you can see at a glance who is offering the best deal on your destination currency. Whether you need Euros, US Dollars, Thai Baht, or Turkish Lira, the latest travel money rates are updated regularly to reflect real market conditions. You can also compare prepaid currency cards to find the right option for managing your spending abroad without surprise fees. Check rates before you book, not at the airport.

FAQ

What is local currency in simple terms?

Local currency is the official money issued by a country’s central bank for use within its own borders. It is used for wages, taxes, contracts, and everyday purchases.

What is the difference between local currency and foreign currency?

Local currency is the legal tender of the country you are in. Foreign currency is any currency from outside that country. When you travel from the UK to France, Euros are the local currency and Pounds are foreign currency.

Why should I always pay in local currency when abroad?

Paying in local currency avoids Dynamic Currency Conversion, where merchants apply their own exchange rate. Card networks such as Visa and Mastercard typically offer better rates than merchant-set conversions.

What fees apply when using foreign currency abroad?

Banks and card networks add markups of 1% to 5% above the mid-market rate on foreign transactions. Using a fee-free travel card and paying in local currency reduces these costs significantly.

What is currency exchange and how does it relate to local currency?

Currency exchange is the process of converting one currency into another. The rate you receive reflects the value of your home currency relative to the local currency of your destination, as set by the global forex market.