Most people assume the rate they see on Google is the rate they’ll get at a bureau de change or bank. It isn’t. The interbank exchange rate is the wholesale rate that banks use when trading currencies directly with one another, and it represents the closest thing to a currency’s true value at any given moment. Retail customers, including individuals buying holiday money and businesses making international payments, almost never receive this rate. Understanding what sits between the interbank rate and the rate you’re actually offered is where the real money is made or lost.

Table of Contents

- What is the interbank exchange rate?

- Why you won’t get the interbank rate

- Factors affecting the interbank rate

- Using interbank rates to make better decisions

- My take on interbank rates and the retail reality

- Compare providers and keep more of your money

- Frequently asked questions

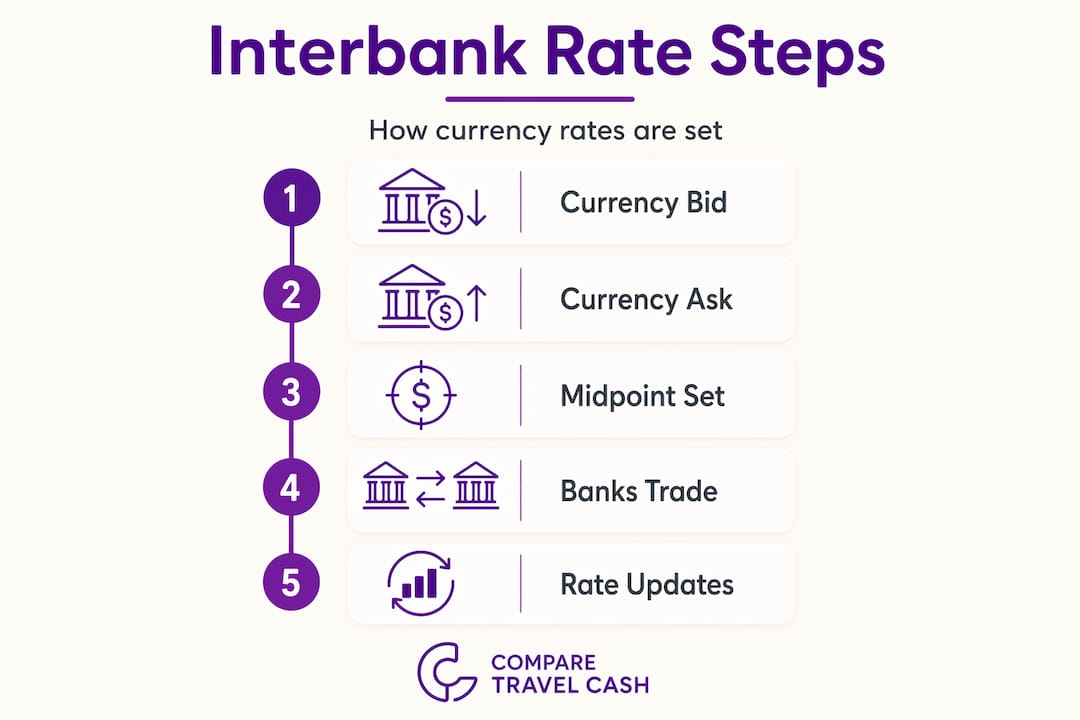

What is the interbank exchange rate?

The interbank exchange rate is, at its core, the price at which banks buy and sell currencies from each other. Think of it as the wholesale price of foreign currency. It is also commonly referred to as the mid-market rate or spot rate, terms you will encounter frequently when comparing travel money or international transfer services.

The rate itself is calculated as the midpoint between two prices: the bid price and the ask price.

- Bid price: the price at which a bank is willing to buy a currency

- Ask price: the price at which a bank is willing to sell a currency

- Spread: the difference between the bid and ask prices, which represents the bank’s profit on the trade

- Mid-market rate: the exact midpoint between bid and ask, often treated as the “true” rate

Here is a simple example. If the bid price for EUR/GBP is 1.0795 and the ask price is 1.0805, then the midpoint is 1.0800. That 1.0800 figure is the interbank or mid-market rate. No fee, no markup. Just the mathematical midpoint between what buyers and sellers are offering at that instant.

The interbank market itself is a decentralised network where banks trade currencies and derivatives directly, usually settling transactions within two business days. Major financial institutions use it primarily to manage exchange rate risk and balance their currency positions. The trades are enormous in scale, often running into millions of pounds per transaction, which is precisely why the pricing is so tight.

Pro Tip: When you look up an exchange rate on Google or a financial website, you are almost certainly seeing the mid-market rate. Use it as a benchmark, not as an expectation of what you will receive.

For a broader grounding in exchange rate terminology, it helps to understand these terms before comparing any provider’s offer.

Why you won’t get the interbank rate

This is where the reality check comes in. Retail customers generally do not receive interbank rates. Providers add a markup to the mid-market rate before offering it to consumers, and that markup is how they generate profit on each transaction.

The markup can come in several forms:

- Spread adjustment: the provider widens the gap between the buy and sell price, so your rate sits further from the true mid-market rate

- Flat service fee: a fixed charge added on top of the exchange rate, sometimes called a transaction fee or commission

- Combined charges: a seemingly low rate paired with a hidden fee, making comparison difficult unless you calculate the total cost of the transaction

- Dynamic pricing: some providers apply internal service rates rather than live mid-market quotes, meaning the rate displayed on their website may differ from the rate applied at checkout

The size of the markup generally correlates with transaction size. Smaller transfers and lower-value currency purchases tend to attract proportionally higher markups because the fixed costs of processing a transaction are spread across a smaller amount. A business converting £50,000 will typically receive a tighter rate than an individual buying £500 in holiday euros.

Detecting the markup is straightforward once you know how. Check the current interbank rate on a reliable financial data site, then compare it directly against what a provider is quoting you. The gap between interbank and offered rates tells you the true cost of the transaction, regardless of how the provider labels it. A bureau de change advertising “no commission” may still apply a rate so far from the mid-market rate that the implied markup is higher than a competitor charging an explicit fee.

Pro Tip: Always calculate total cost rather than comparing headline rates. Take the mid-market rate, apply it to your amount, then compare the result against what the provider will actually give you after all charges.

Understanding how choosing the right exchange provider affects your final amount received is one of the most practical things you can do before any currency purchase.

Factors affecting the interbank rate

Interbank exchange rates do not sit still. They shift constantly, reflecting the collective judgement of millions of market participants reacting to economic data, political news, and shifts in global sentiment. Rates fluctuate minute by minute, which means the rate you see at 9am may look quite different by mid-afternoon.

Several forces drive these movements:

| Factor | How it affects the rate |

|---|---|

| Supply and demand | High demand for a currency pushes its value up; excess supply pushes it down |

| Central bank policy | Interest rate decisions and direct market interventions shift rates significantly |

| Economic data releases | Inflation figures, employment reports, and GDP data move markets quickly |

| Market sentiment | Risk appetite or aversion drives flows into or out of currencies perceived as safe |

| Liquidity conditions | Reduced market activity can widen spreads, raising effective exchange costs |

Central banks hold particular sway. A notable example: the Central Bank of Sri Lanka capped its interbank spot USD rate to stabilise the rupee during a period of acute currency volatility. That single intervention directly changed the rate available across the entire market, demonstrating how policy decisions at the institutional level can ripple through to every transaction.

It is also worth understanding that interbank spreads can widen during periods of low liquidity, such as during public holidays, overnight sessions, or around major news events. When the spread widens, the effective cost of converting currency increases even if the mid-market rate itself has not moved dramatically.

“The rate you see is a snapshot. The rate you get is shaped by when you transact, who you use, and what is happening in global markets at that precise moment.”

Using interbank rates to make better decisions

Knowing what the interbank rate is gives you a reliable starting point for every currency decision, whether you are booking holiday money, paying an overseas supplier, or sending money abroad. Interbank rates serve as the benchmark against which every retail rate should be measured.

Here is how to put that knowledge to work:

- Set a benchmark before you shop. Look up the current mid-market rate for your currency pair before approaching any provider. This takes thirty seconds and gives you an objective measure to compare against.

- Compare total costs, not headline rates. A provider offering a rate that looks close to mid-market but charging a £10 transaction fee may still be worse than a provider with a slightly wider spread and no fee. Run the full calculation.

- Be wary of “interbank-like” claims. Providers may advertise rates that closely mirror interbank quotes, but the actual applied rate at the point of transaction can include spreads or fees not immediately visible. Always check the final amount you receive.

- Larger amounts command better rates. If you are exchanging a significant sum, you often have room to negotiate or access tighter rates. Providers hedge and price transactions differently based on size, and a larger transfer can unlock better pricing.

- Timing matters more than most people realise. Exchanging currency during periods of lower market volatility, when spreads are tighter, can yield a meaningfully better rate than transacting during or immediately after a major news event.

- Use comparison tools. Rather than checking each provider individually, use a platform that aggregates live rates from multiple sources, allowing you to see at a glance which provider is closest to the interbank rate for your specific currency and amount.

For context on how specific providers price their travel money, checking live data for providers such as Barclays travel money rates or The Currency Club can quickly reveal how far each sits from the mid-market rate on any given day.

My take on interbank rates and the retail reality

I’ve spent a long time watching how people approach currency exchange, and the same mistake comes up repeatedly. Travellers and business owners alike fixate on whether a provider charges a fee rather than asking the more revealing question: what rate are they actually applying?

In my experience, the most transparent providers are those who show you the mid-market rate, show you their fee, and let you calculate the total cost yourself. The least transparent are those who bury the markup inside a “fee-free” offering where the rate is so far from mid-market that the implied charge is higher than it appears. I’ve seen markups of 3 to 5 percent presented as a courtesy to the customer.

What I’ve also learned is that major financial institutions manage their FX exposure in ways that retail customers simply cannot replicate. The interbank market is not designed for consumers. But understanding it changes how you evaluate every rate you are offered. When you know what the true mid-market rate is, you stop accepting whatever a provider shows you and start asking what it costs you to access that rate.

Technology is closing the gap. Some services now offer rates that sit very close to the mid-market rate, passing on near-wholesale pricing to retail customers with a transparent flat fee. That shift has been the most meaningful development for everyday currency users in the past decade.

The interbank rate is not something you will ever receive directly. But it is the most useful number you have when deciding whether you are getting a fair deal.

— Jason

Compare providers and keep more of your money

Understanding the interbank rate is only useful if you act on it. The practical next step is seeing exactly how much different providers charge above the mid-market rate for your specific currency and amount.

Comparetravelcash pulls live rates from dozens of UK travel money providers, letting you see side by side which is closest to the interbank rate for euros, dollars, or any other currency you need. There is no guesswork about fees or markups. You can compare travel money rates from top providers including Hays Travel, giving you a clear view of total costs before you commit. For a specific look at what one competitive provider is currently offering, check the latest Hays Travel rates and see how they stack up against the mid-market rate today.

Frequently asked questions

What does “interbank exchange rate” mean?

The interbank exchange rate is the rate at which banks buy and sell currencies from each other in the wholesale foreign exchange market. It is also known as the mid-market rate or spot rate, and it represents the midpoint between the buy (bid) and sell (ask) prices at any given moment.

Do individuals ever get the interbank rate?

Retail customers very rarely receive the interbank rate. Providers add a markup above the mid-market rate to cover costs and generate profit, meaning the rate you are offered is almost always less favourable than the true interbank rate.

How is the interbank rate calculated?

The interbank rate is calculated as the midpoint between the bid price (what a buyer will pay) and the ask price (what a seller will accept). For example, a bid of 1.0795 and an ask of 1.0805 produces a mid-market rate of 1.0800.

Why does the interbank rate change so often?

Interbank rates change minute by minute because they reflect live supply and demand in the global foreign exchange market. Economic data releases, central bank decisions, and shifts in market sentiment can all move rates rapidly throughout the trading day.

How can I use the interbank rate to get a better deal on travel money?

Look up the current mid-market rate before approaching any provider, then calculate the full cost of the transaction including all fees. The closer a provider’s offered rate is to the interbank rate, the less you are paying in markup. Comparison platforms such as Comparetravelcash make this calculation quick and easy.