A holiday cash guide UK is a practical framework covering how to buy, carry, and protect foreign currency before and during a trip abroad. Most UK travellers lose money not through bad luck but through avoidable decisions: exchanging currency at the airport, accepting dynamic currency conversion without realising it, or carrying cash without understanding declaration rules. This guide covers the full picture, from ordering euros or dollars at the best rate using providers like M&S Travel Money and The Currency Club, to using cards like Monzo and Revolut smartly abroad, and staying on the right side of HMRC’s cash declaration rules.

What are the best ways to order holiday cash in the UK?

Ordering currency in advance is the single most effective way to save money on travel money. Airport exchange rates are typically among the worst available, and the convenience comes at a real cost. On larger amounts, the difference between an airport kiosk rate and an online rate can run to hundreds of pounds.

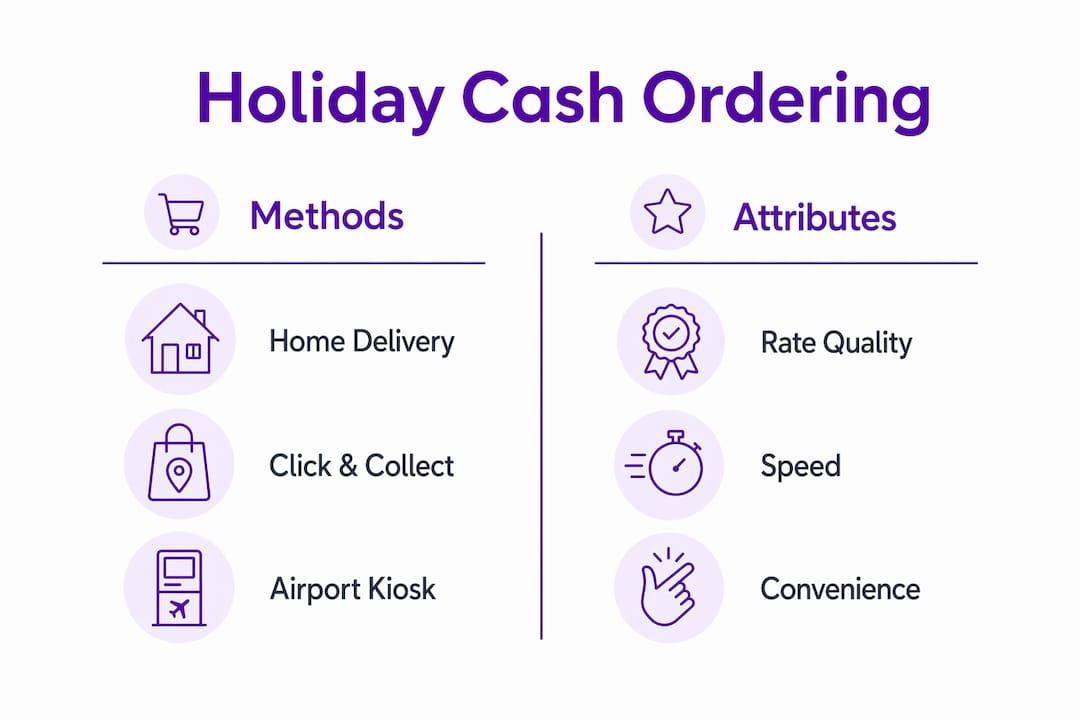

The two main ordering methods are home delivery and click-and-collect. Home delivery suits those who plan ahead by a week or more. Click-and-collect, offered by providers including M&S Travel Money and The Post Office, lets you order online at the better web rate and pick up in store, sometimes on the same day. Both options beat walking up to an exchange desk without a pre-booked rate.

When comparing providers, look beyond the headline exchange rate. Some providers advertise a strong rate but add a delivery fee or a minimum order charge. Use a comparison tool to see the total cost for your specific amount. The rate you see on a comparison site is the rate you lock in at the time of ordering, which protects you from short-term market movements.

Timing your purchase also matters. Exchange rates move daily in response to economic data, political events, and central bank decisions. Buying in stages, splitting your order across two or three purchases over several weeks, reduces the risk of buying everything at a poor moment. This is sometimes called pound-cost averaging, and it works for currency just as it does for investments.

Pro Tip: Before ordering any new currency, check your drawers and coat pockets for leftover foreign notes from previous trips. Many UK travellers have €50 to €100 sitting unused at home. Providers including M&S Travel Money and The Currency Club offer buyback services, so you can sell old currency and offset the cost of your new order.

Here is a quick comparison of the main ordering methods:

| Method | Rate quality | Speed | Convenience |

|---|---|---|---|

| Airport kiosk (walk-up) | Poor | Immediate | High |

| High street bureau (walk-up) | Fair | Immediate | Moderate |

| Online order with home delivery | Good to excellent | 2 to 5 days | High |

| Online order with click-and-collect | Good to excellent | Same day to 48 hours | Moderate |

| Prepaid travel card (loaded online) | Good | Instant to 24 hours | High |

The table makes clear that the trade-off is almost always between convenience and rate quality. Planning ahead removes that trade-off entirely.

How to use cards and ATMs abroad without paying extra fees

Prepaid travel cards and fee-free debit cards have changed how UK travellers manage money abroad. Cards like Monzo and Revolut use the mid-market exchange rate with no foreign transaction fee, which is consistently better than what most high-street banks offer. The mid-market rate is the rate you see on Google or XE.com. It is the midpoint between the buy and sell rates on the wholesale currency market, and it is the fairest benchmark for any exchange.

However, fee-free does not mean unlimited. Monzo allows fee-free ATM withdrawals across the EEA with no cap, but outside the EEA the limit is £200 per 30-day period before fees apply. Revolut has similar tiered limits depending on your account plan. Exceeding these limits triggers a percentage fee on each withdrawal, which adds up quickly on a two-week trip. Planning your withdrawals around these fee-free windows is the practical way to avoid surprise charges.

Understanding dynamic currency conversion

Dynamic currency conversion (DCC) is the practice where a foreign ATM or card terminal offers to process your payment in pounds sterling rather than the local currency. It sounds helpful. It is not. Choosing local currency every time you pay or withdraw abroad avoids the DCC markup, which typically adds 3 to 5% on top of the transaction, plus your card issuer’s own foreign transaction fee on top of that.

The problem is that DCC is often pre-selected on payment terminals. The screen may say “Pay in GBP for your convenience” or show a pre-ticked box. You must actively choose the local currency option every single time. This applies at hotel checkouts, restaurants, car hire desks, and ATMs. The largest savings on any trip often come from this one habit alone.

Here is a step-by-step approach to managing cards and ATMs abroad:

- Before you travel, check your card’s fee-free ATM withdrawal limit and note the reset date.

- Enable spending notifications on your card app so every transaction is visible in real time.

- At any ATM or terminal, always select “pay in [local currency]” and decline any offer to pay in GBP.

- Withdraw larger amounts less frequently rather than small amounts repeatedly, to stay within fee-free limits.

- Keep a small amount of local cash for markets, taxis, and small vendors who do not accept cards.

- If your card is lost or stolen, freeze it immediately via the app and contact your provider. Keep the emergency number saved offline.

Pro Tip: Set a daily spending limit on your travel card before you leave. Most card apps, including Monzo and Revolut, let you customise limits and receive instant alerts. This gives you a real-time budget tracker and an early warning if your card details are compromised.

For a deeper look at how currency conversion fees work and where they hide, Comparetravelcash has a dedicated explainer worth reading before you travel.

What are the legal cash limits for travelling to and from the UK?

Carrying cash above £10,000 into or out of Great Britain triggers a legal declaration requirement at customs. This is not a tax. It is a disclosure rule designed to prevent money laundering and financial crime. Carrying large sums is entirely legal. Failing to declare is not.

The rules differ slightly depending on where you are travelling:

- Great Britain (England, Scotland, Wales): Declare cash of £10,000 or more when crossing the border.

- Northern Ireland: The threshold is €10,000 or the equivalent in another currency, reflecting the land border with the Republic of Ireland.

- Travelling as a group or family: Each person’s cash is counted separately, but if you are carrying cash on behalf of others, the total amount you are physically carrying counts as yours for declaration purposes.

- Overseas destinations: Many countries have their own declaration rules. The USA requires declaration of $10,000 or more. Australia requires AUD 10,000. Always check the rules for your destination before you travel.

You can declare cash online via gov.uk before you travel or at the border on arrival or departure. The process is straightforward and takes a few minutes. Integrating this check into your packing routine, rather than leaving it to the last minute, avoids delays at the border.

Know the penalty: Failing to declare cash above the threshold can result in seizure of the entire sum and a fine of up to £5,000. Border Force officers have the authority to detain undeclared cash even if you can prove it is legitimately yours. The burden of proof falls on the traveller, not the officer.

Routine declaration checks should be part of every trip preparation, not an afterthought. Even legitimate holiday cash can trigger obligations if the amount is close to or above the threshold.

How do you keep holiday cash and cards safe while travelling?

Physical cash requires a different security mindset to cards. Once cash is gone, it is gone. There is no fraud team to call and no chargeback process. The following practices reduce the risk significantly.

- Divide cash among your travel party. If one person is pickpocketed, the rest of the group still has funds. Never keep all your cash in one wallet or bag.

- Use your hotel safe. Most hotels provide in-room safes. Store the bulk of your cash and your backup card there, and carry only what you need for the day.

- Choose ATMs carefully. Use machines attached to banks or located inside well-lit, busy areas. Inspect the card slot and keypad before inserting your card. A loose or bulky card reader is a common sign of a skimming device.

- Use an RFID-blocking wallet. Contactless card data can be read remotely in crowded spaces. An RFID-blocking wallet or card sleeve prevents this. They cost a few pounds and are widely available from retailers including Amazon and Travelsmith.

- Keep emergency contacts offline. Save your bank’s emergency number in your phone and write it on a piece of paper kept separately from your wallet. If your phone and wallet are stolen together, you still have the number.

Splitting cash among travellers combined with spending alerts and secure storage is the most reliable combination of safety measures available to a UK holidaymaker. No single measure is foolproof, but layering several together makes opportunistic theft far less rewarding.

Pro Tip: Take a photo of your cards (front only, never the CVV) and store it in a password-protected folder on your phone. If your wallet is stolen, you will have the card numbers and expiry dates ready when you call to cancel, which speeds up the process considerably.

For more on exchanging money safely and avoiding fraud when buying currency, Comparetravelcash has a practical guide covering the most common scams targeting UK travellers.

What I have learned from watching UK travellers get this wrong

After years of tracking how UK holidaymakers handle travel money, the pattern of mistakes is remarkably consistent. The airport exchange is the most expensive and the most common. People know it is bad value and do it anyway because they ran out of time. The fix is not discipline. It is a 10-minute online order placed three weeks before departure.

The DCC problem is subtler and, in some ways, more costly. Travellers who use fee-free cards like Monzo correctly but then accept DCC at every restaurant and hotel checkout are effectively cancelling out the savings. The card is doing its job. The terminal is undoing it. You have to stay alert every single time.

I would also push back on the idea that cash is old-fashioned. Cards fail. Systems go down. Some of the best markets, local restaurants, and transport options in popular destinations are cash-only. A balanced approach, a fee-free card for most spending and a modest amount of pre-ordered local cash for flexibility, is more practical than going fully cashless.

The declaration rules catch people off guard more than they should. Carrying £12,000 in cash to buy a car abroad is perfectly legal. Not declaring it at the border is not. Check the rules before you pack, not at the departure gate.

— Jason

Compare rates and find your best deal with Comparetravelcash

Ready to put this guide into practice? Comparetravelcash makes it straightforward to find the best travel money rates available to UK holidaymakers right now.

The platform compares live exchange rates from multiple UK providers in one place, so you can see exactly how much local currency your pounds will buy before you commit. You can check The Currency Club’s latest rates for competitive euro and dollar deals, or browse the prepaid multi-currency card comparison to find a card that suits your destination and spending habits. Whether you are buying cash online, loading a travel card, or comparing buyback rates for leftover currency, Comparetravelcash gives you the numbers you need to make a confident decision.

FAQ

What is the best way to get holiday cash in the UK?

Order currency online in advance from a reputable provider and collect in store or arrange home delivery. Airport exchange rates are consistently among the worst available, so early ordering saves the most money.

How much cash can I take abroad from the UK?

You can take any amount of cash abroad, but you must declare £10,000 or more when leaving Great Britain. Failure to declare can result in seizure of the cash and a fine of up to £5,000.

What is dynamic currency conversion and should I avoid it?

Dynamic currency conversion (DCC) is when a foreign terminal offers to charge you in pounds instead of the local currency. You should always decline it. DCC adds 3 to 5% to the transaction cost on top of any card fees your provider charges.

Are prepaid travel cards worth using abroad?

Yes, for most travellers. Cards like Monzo and Revolut use the mid-market rate with no foreign transaction fee. Be aware that fee-free ATM withdrawals outside the EEA are capped at £200 per 30 days on Monzo’s standard account, so plan withdrawals accordingly.

Do I need to declare cash when entering the UK?

Yes. If you are carrying £10,000 or more in cash when entering Great Britain, you must declare it to customs. The same threshold applies on departure, and declaration is mandatory regardless of whether the money is in sterling or foreign currency.