A currency card is a prepaid payment card that lets you load and spend multiple foreign currencies securely while abroad, giving you far more control over your exchange rates than a standard debit card ever could. Providers such as Wise, Revolut, and the Post Office offer prepaid travel cards that are now a fixture in the UK travel money market. This currency card usage guide walks you through choosing the right card, setting it up correctly, using it abroad without losing money to hidden fees, and building a backup strategy that keeps you covered when things go wrong.

What does a good currency card usage guide actually cover?

The term “currency card” is widely used, but the recognised industry term is prepaid travel card or multi-currency prepaid card. Understanding that distinction matters because different card types carry different protections, fee structures, and reload options. A prepaid travel card is not linked to your bank account, which limits your exposure if the card is lost or stolen. A travel credit card, by contrast, offers Section 75 protection under the Consumer Credit Act 1974 for purchases over £100. Both have a place in a well-planned trip, and this guide covers both.

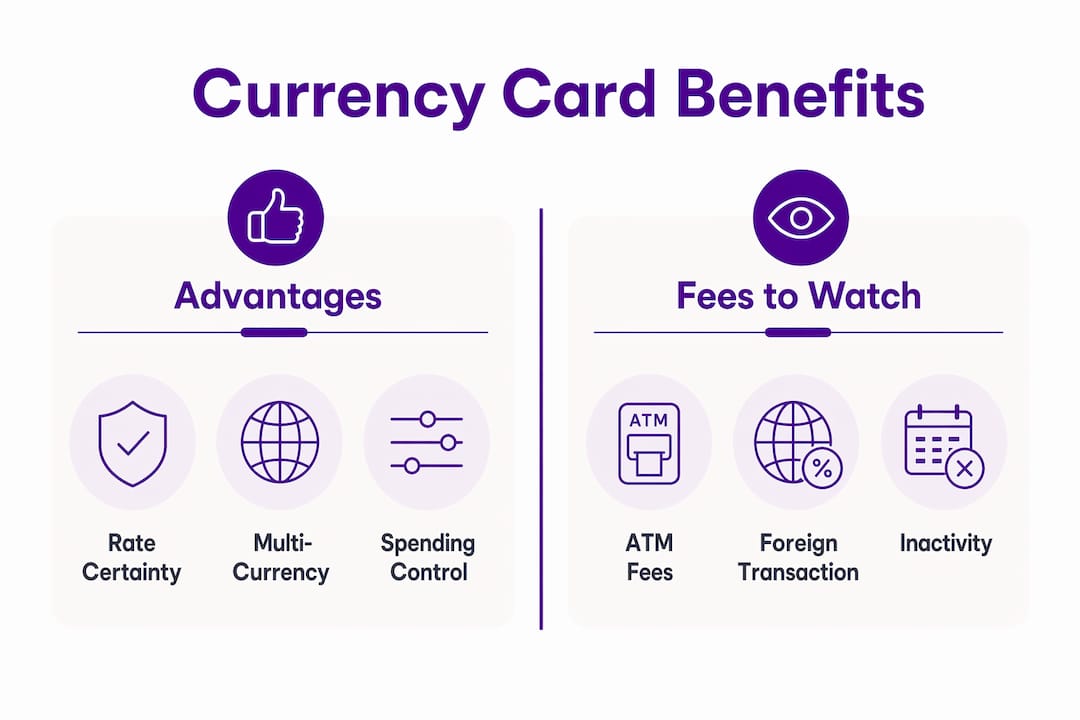

The core benefit of a prepaid travel card is rate certainty. You load a currency at a rate you choose, and that rate is locked in. If sterling weakens after you travel, your euros or dollars are unaffected. That predictability is something neither a standard debit card nor cash from an airport bureau can reliably offer.

How to choose the right currency card for your trip

No single card suits every traveller. The right choice depends on your destination, trip length, and how you actually spend money when you travel.

Destination cash culture

Some countries are still heavily cash-dependent. Rural areas of Turkey, Thailand, and parts of Eastern Europe rely on notes far more than contactless payments. If your destination falls into that category, a card with low ATM withdrawal fees matters more than one with premium contactless features. For cash-light destinations such as the Netherlands or Sweden, a card with zero foreign transaction fees and strong app support is the priority.

Multi-currency capability

Multi-currency cards can hold 15 to 40 or more currencies, which significantly reduces cross-currency conversion charges for travellers visiting several countries on one trip. If you are doing a two-week trip through France, Croatia, and Morocco, a card that holds euros, Croatian kuna, and Moroccan dirhams separately will save you from paying conversion fees every time you switch countries.

Fees to watch before you commit

| Fee type | What to look for |

|---|---|

| ATM withdrawal fee | Zero or capped fee per withdrawal |

| Foreign transaction fee | 0% is standard on good travel cards |

| Inactivity fee | Charged after 6 to 12 months of no use |

| Reload fee | Free via bank transfer; fees may apply for debit card loads |

| Currency conversion fee | Check the markup above the mid-market rate |

Pro Tip: Compare the mid-market rate on Google against the rate your card provider offers at the point of loading. A 1.5% markup sounds small but adds up quickly on a £2,000 holiday budget.

Currency card vs credit card: which wins?

The currency card vs credit card debate does not have a clean winner. Prepaid travel cards give you rate control and spending discipline because you can only spend what you load. Travel credit cards offer purchase protection and often earn rewards, but they can carry foreign transaction fees of 2 to 3% if you choose the wrong product. For most UK travellers, the answer is to use both, which is covered in section five.

How to set up and load your currency card

Getting your card ready before you leave is where most problems are avoided. Most card failures happen before departure due to incomplete verification or skipped activation steps. Follow this process to avoid that entirely.

- Order early. Apply at least two weeks before travel to allow for postal delivery and identity verification. Wise and Revolut offer digital-first cards that arrive faster, but Post Office travel cards require in-branch or online ordering with standard delivery times.

- Complete identity verification. Most providers require a passport or driving licence scan via their app. Do not skip this step. Unverified accounts often have lower spending limits or restricted ATM access.

- Activate the card. Log into the provider’s app or web portal and follow the activation steps. This usually involves setting a PIN and confirming your identity.

- Load your chosen currencies. Use the app or online portal to transfer funds from your UK bank account. Bank transfer is almost always free; debit card loads may carry a small fee.

- Lock in your exchange rate. Load the currencies you need before you travel, particularly if you expect sterling to weaken. Once loaded, that rate is fixed regardless of market movements.

- Test the card. Make a small purchase or ATM withdrawal before you leave the UK to confirm the card is working correctly.

Reloads are typically available for spending within two hours of initiation during standard business hours, which means you can top up from abroad if needed. However, relying on this while standing at a foreign ATM is not a position you want to be in.

Pro Tip: Load funds in smaller batches rather than one large sum. Unused balances can attract inactivity fees if left untouched for six to twelve months, and loading incrementally keeps your money working rather than sitting idle.

How to use your currency card abroad without losing money

This is where most travellers make expensive mistakes, often without realising it until they check their statement at home.

Always pay in local currency

Dynamic Currency Conversion (DCC) is the single biggest hidden cost trap for UK travellers abroad. When a card terminal or ATM offers to process your payment in pounds sterling rather than the local currency, it is applying its own exchange rate, not your card provider’s. Accepting DCC can add a markup of 3 to 7% above the standard exchange rate. On a €500 restaurant bill, that is a silent charge of up to €35 that goes straight to the merchant’s payment processor.

Always select “pay in local currency” at every terminal and ATM. If a machine automatically processes in sterling, cancel the transaction and try again or use a different machine.

ATM withdrawal strategy

- Use ATMs attached to major banks rather than standalone machines in tourist areas, which often apply their own conversion fees on top of DCC.

- Withdraw larger amounts less frequently to reduce per-transaction fees where your card charges them.

- Check your card’s daily ATM limit before you travel. Some providers cap withdrawals at £200 to £300 per day, which can be restrictive in cash-heavy destinations.

- Avoid airport ATMs for your first withdrawal. Rates and fees at airports are consistently worse than in-town bank ATMs.

Security and spending controls

Strong app support lets you set spending limits, freeze your card instantly, and receive real-time transaction alerts. Wise, Revolut, and Caxton all offer this functionality. If your card is used fraudulently, you can freeze it within seconds from your phone rather than waiting on hold with a call centre. Set up transaction notifications before you leave the UK so that every payment triggers an alert. This is not just a security measure. It is also the most effective way to track your spending against your holiday budget in real time.

Pro Tip: Take a photo of your card’s customer service number and store it separately from the card itself. If your phone and card are both lost, you will still be able to report the card from a local phone.

How to manage currency cards alongside other payment methods

A single currency card is not a complete travel payment strategy. A hybrid approach using a multi-currency card for daily spending and a travel credit card for larger purchases gives you flexibility, redundancy, and the best of both worlds in terms of fees and protections.

- Carry two cards from different networks. Cards from different issuers and networks reduce the risk of a single point of failure. If your Mastercard-based prepaid card is declined, a Visa travel credit card gives you an immediate fallback.

- Use your travel credit card for hotels and car hire. Many hotels and car rental companies place temporary holds on funds. A credit card handles these without locking up your prepaid card balance.

- Keep a small cash reserve. Markets, rural taxis, and small guesthouses in many destinations do not accept cards. Carrying the equivalent of £50 to £100 in local currency covers these gaps without exposing you to significant exchange rate risk.

- Set up alerts on all cards. Monitoring transactions across both your prepaid card and travel credit card via their respective apps gives you a complete picture of your spending.

- Adjust your currency balance if plans change. If your itinerary shifts and you no longer need a particular currency, convert the balance back or to another currency before leaving the country. Most providers allow this within the app, though some charge a small conversion fee.

Staying connected abroad is also part of the equation. If you need reliable mobile data to reload your card or monitor transactions, an international eSIM can keep you online without roaming charges, which is particularly useful in destinations where your UK network coverage is limited.

What I have learnt from using currency cards on multi-country trips

After years of watching UK travellers make the same expensive errors, the pattern is clear. The biggest losses do not come from poor exchange rates. They come from complacency at the point of payment. DCC is the most consistent culprit. Travellers who understand it intellectually still accept it at the terminal because the machine presents it as the default option and the queue behind them is growing.

My advice is to treat every card terminal abroad as a potential DCC trap until proven otherwise. Make it a habit to look for the currency selection screen before you tap or insert. It takes three seconds and can save you more than any rate comparison you did before leaving home.

The second lesson is about preparation. Travellers who test their cards, complete verification, and load currencies before departure almost never have problems. Those who leave it until the airport, or assume the card will just work, are the ones calling their provider from a hotel lobby at 11pm. Use a prepaid travel card comparison tool before you commit to a provider, and check the fee schedule in detail rather than relying on headline marketing claims.

Finally, do not underestimate the value of familiarity with your card’s app before you travel. Spend ten minutes exploring the freeze function, the transaction history, and the reload process while you are still at home. That ten minutes is worth more than any travel insurance add-on.

— Jason

Compare currency cards and travel money deals before you go

Finding the right prepaid travel card is straightforward when you can see all the fees, exchange rates, and features side by side in one place.

Comparetravelcash brings together the latest rates and card deals from providers across the UK, so you can see exactly what you are getting before you commit. Whether you are looking for the lowest ATM fees, the best euro rate, or a card that covers a dozen currencies for a longer trip, the currency card comparison tool gives you a clear, up-to-date picture. You can also compare travel money rates across bureaux and online providers to make sure your cash spending is just as cost-effective as your card spending.

FAQ

What is a prepaid currency card?

A prepaid currency card is a payment card loaded with foreign currency in advance, allowing you to spend abroad at a pre-agreed exchange rate without connecting to your bank account. Providers such as Wise, Revolut, and the Post Office offer these cards to UK travellers.

How do I avoid fees when using a currency card abroad?

Always pay in local currency to avoid Dynamic Currency Conversion markups of 3 to 7%, use ATMs attached to major banks, and withdraw larger amounts less frequently to minimise per-transaction charges.

Can I reload a currency card while I am abroad?

Yes. Reloads are typically available within two hours of initiation during standard business hours, provided you have a reliable internet connection and your account verification is complete.

Is a currency card better than a travel credit card?

The optimal choice depends on your spending habits and trip length. A prepaid currency card offers rate certainty and spending control, while a travel credit card provides purchase protection and potential rewards. Most experienced travellers use both.

What happens to unused currency on my card after the trip?

Unused balances can be converted back to sterling via the provider’s app, though a small conversion fee may apply. Leaving balances unused for six to twelve months risks triggering inactivity fees, so it is worth clearing or converting leftover funds promptly after returning home.