Dynamic currency conversion (DCC) is a payment service that lets you pay in your home currency at foreign point-of-sale terminals and ATMs, rather than the local currency of the country you are visiting. It sounds convenient, but markups can reach 18% above the standard exchange rate. That extra cost is real money leaving your wallet on every transaction. Understanding how DCC works, and when to decline it, is one of the most practical financial skills a traveller can have. Payment networks like Visa and Mastercard operate within the DCC ecosystem, and processors like Stripe have built it directly into modern payment gateways.

How does dynamic currency conversion work?

DCC begins the moment a foreign card is inserted or tapped at a payment terminal. The POS system detects your card’s country of origin from the card’s BIN (Bank Identification Number) and identifies your home currency automatically. The terminal then presents you with a choice: pay in the local currency or pay in your home currency at a rate calculated on the spot.

That on-the-spot rate is where the cost lies. The DCC operator takes the wholesale interbank rate, which is the rate banks use when trading currencies between themselves, and adds a markup. This markup covers the DCC operator’s profit and a commission paid back to the merchant. The rate you see on the screen is already inflated before you press a single button.

Here is how the process unfolds step by step:

- Card detection. The terminal reads your card’s BIN and identifies your home currency.

- DCC offer presented. The screen shows you a choice between the local currency amount and your home currency equivalent.

- Rate calculation. The DCC operator applies a marked-up rate to the interbank wholesale rate.

- Merchant commission. Merchants receive commissions from DCC transactions, credited monthly, which incentivises staff to steer you towards accepting DCC.

- Transaction processed. Your card is charged in your home currency at the inflated rate.

Payment technology advancements have integrated DCC automatically into POS systems and e-commerce platforms, making it more prevalent than ever. The same process applies at ATMs abroad, where the machine may ask whether you want to “lock in” a rate in pounds sterling before dispensing cash.

Pro Tip: If a terminal or ATM asks whether you want to pay in your home currency or the local currency, always choose the local currency. That single choice can save you a meaningful percentage on every transaction.

The pros and cons of dynamic currency conversion

DCC is not entirely without merit, but its drawbacks far outweigh its benefits for most travellers. Here is an honest breakdown.

Perceived advantages

- Immediate cost visibility. You see the charge in pounds sterling before confirming, which removes the uncertainty of not knowing what your bank will charge.

- Budgeting clarity. Some travellers find it easier to track spending when all amounts appear in their home currency.

- Receipt confirmation. The home currency amount appears on your receipt, making expense reporting simpler for business travellers.

The real drawbacks

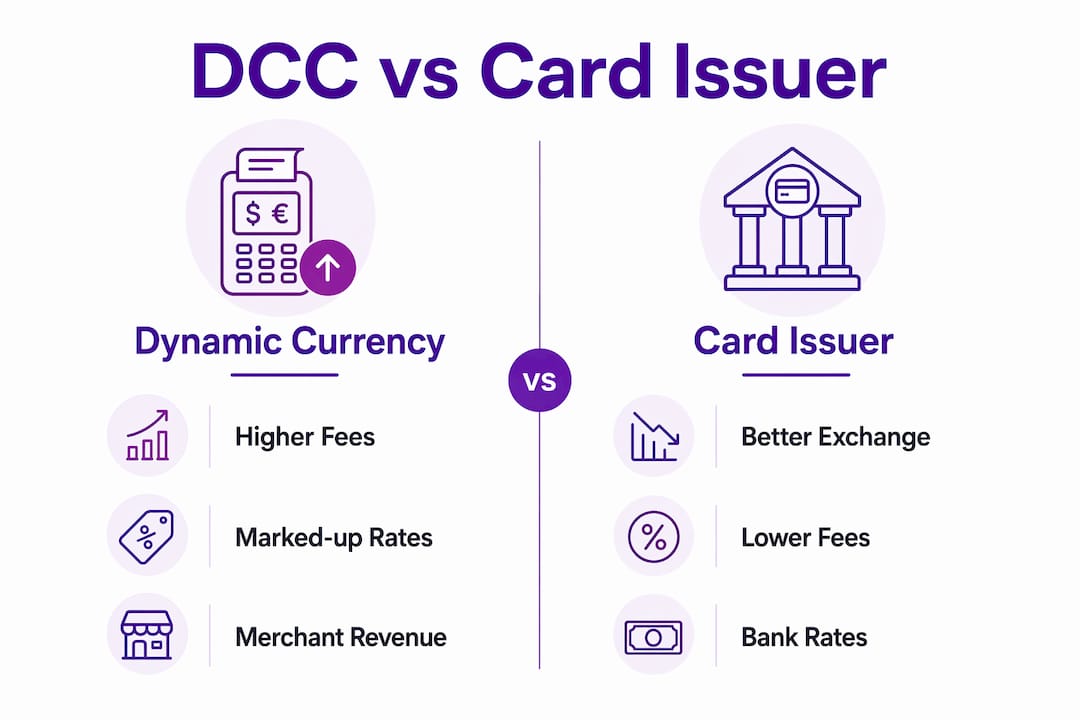

- High markups. DCC markups can reach 18% above the standard exchange rate. On a £500 hotel bill, that is up to £90 in unnecessary fees.

- Opaque fees. DCC exchange rates bundle conversion fees that are difficult to assess, making it hard to judge the true cost at the point of payment.

- Double fees risk. Additional foreign transaction fees may still be charged by your card issuer on top of the already inflated DCC rate. Accepting DCC does not exempt you from your bank’s own charges.

- Merchant bias. DCC operators exist primarily to generate revenue for merchants and operators, not to add value for cardholders.

- Pressure tactics. Some terminals are designed to make the home currency option appear as the default or the “safer” choice, nudging travellers into accepting DCC without realising the cost.

The supposed benefit of transparency is largely an illusion. Seeing a pound amount on screen feels reassuring, but the marked-up rate obscures the true cost compared to what your bank would charge. You are paying for the comfort of a familiar number.

Pro Tip: Before travelling, check whether your card charges a foreign transaction fee. If it does, that fee applies regardless of whether you accept or decline DCC, so choosing a card with no foreign transaction fees is a separate but equally important step.

Dynamic currency conversion vs regular exchange: which costs more?

The difference between DCC and letting your own bank handle the conversion is significant. The table below shows the key contrasts.

| Factor | Dynamic currency conversion | Card issuer conversion |

|---|---|---|

| Exchange rate used | Interbank rate plus DCC markup | Wholesale interbank rate |

| Typical markup | Up to 18% above interbank rate | Usually 0%–3% depending on card |

| Fee transparency | Rate shown on screen but markup hidden | Fee listed in card terms |

| Who controls the rate | Third-party DCC operator | Your bank or card network |

| Merchant incentive | Merchant earns commission | No merchant benefit |

| Your control | You can decline at the terminal | Applied automatically when paying in local currency |

Card issuer rates almost invariably offer better exchange rates than DCC providers. Paying in local currency lets your bank perform the conversion at the wholesale interbank rate, which is consistently cheaper than any DCC rate you will encounter at a terminal.

Visa and Mastercard do require disclosure of exchange rates and margins during DCC offers, but compliance varies and some terminals pressure customers to choose DCC. The disclosure rules exist on paper, yet enforcement is inconsistent across markets. In practice, many travellers accept DCC without realising they have been shown a rate that is materially worse than their bank’s rate.

A common misconception is that DCC provides a better rate because it is “confirmed” at the point of sale. The rate is confirmed, but it is confirmed at an inflated level. Your bank’s rate, applied when you pay in local currency, is nearly always lower. Understanding local currency benefits for travellers is the clearest way to see why declining DCC is the financially sound choice.

When to accept or decline dynamic currency conversion

Knowing the theory is one thing. Knowing exactly what to do at a terminal abroad is another. Follow this checklist every time you use your card overseas.

- Read the screen carefully. When a terminal presents a currency choice, pause before tapping confirm. Look for the words “dynamic currency conversion,” “pay in GBP,” or “pay in [your home currency].”

- Check the rate shown. If the terminal displays a rate, compare it mentally to the mid-market rate you can look up on Google or XE.com. A difference of more than 1%–2% is a red flag.

- Always choose local currency. Experts consistently advise travellers to decline DCC at the point of sale. Select the local currency option every time unless you have a specific reason not to.

- At ATMs, decline the “guaranteed rate.” ATMs often phrase DCC as a “guaranteed exchange rate” or ask you to “lock in” a rate. Decline this and choose to be charged in local currency.

- Use a card with no foreign transaction fees. Travel cards with no foreign transaction fees reduce overall costs regardless of conversion choice. Cards from providers such as Starling Bank, Chase UK, and Monzo currently offer fee-free foreign spending.

- Consider a prepaid multi-currency card. Loading a card with euros, US dollars, or another currency before you travel means you are spending at the rate you loaded, bypassing DCC entirely.

- Withdraw local cash from reputable sources. If you need cash, use a bank-affiliated ATM rather than independent machines in tourist areas, which are more likely to push DCC aggressively.

For a broader view of how to avoid costly travel traps, including poor exchange rate offers beyond DCC, Comparetravelcash has detailed guidance on recognising bad rates before they cost you.

Understanding currency conversion fees for UK travellers in full gives you the complete picture of every charge that can appear on a foreign transaction, not just DCC.

My honest view on DCC: it is designed to catch you off guard

I have watched travellers accept DCC at hotel checkouts, restaurant terminals, and airport ATMs without a second thought. The screen looks official. The rate appears “confirmed.” The whole experience is designed to feel like a service rather than a charge.

The reality is that DCC primarily exists to generate revenue for merchants and operators. The traveller gains nothing material. The convenience of seeing a pound figure on screen costs you real money, and the system is deliberately structured so that the cost is not obvious at the moment you pay.

What frustrates me most is the pressure element. Some terminals default to the home currency option, requiring you to actively scroll or press an extra button to pay in local currency. That friction is not accidental. It is a design choice that benefits the merchant at your expense.

My advice is simple: treat every DCC offer as a fee you are being asked to pay voluntarily. Because that is exactly what it is. Decline it, pay in local currency, and let your bank apply its rate. If you are using a card with no foreign transaction fees, you will almost always pay less. The cross-border payments market is valued in the hundreds of billions, and a meaningful slice of that revenue flows from travellers who did not know they could simply say no.

— Jason

Compare travel money rates before you go

Avoiding DCC at the terminal is only half the battle. The other half is making sure the currency you carry, or the card you use, is already working in your favour before you board the plane.

Comparetravelcash compares live travel money exchange rates from providers across the UK, so you can see at a glance who is offering the best rate for your destination currency. Whether you want to compare prepaid multi-currency cards that sidestep DCC entirely, or find the best rate for buying euros or dollars before you travel, the tools are free to use. You can also compare travel money rates online from multiple providers in one place, avoiding the guesswork of checking each supplier individually. Sorting your currency before you travel puts you in control from the start.

FAQ

What is dynamic currency conversion in simple terms?

Dynamic currency conversion is a service that lets you pay in your home currency at a foreign terminal or ATM, rather than the local currency. The rate used includes a markup above the standard interbank rate, which makes it more expensive than letting your own bank handle the conversion.

Is dynamic currency conversion worth it?

For most travellers, dynamic currency conversion is not worth it. Markups can reach 18% above the standard rate, and your card issuer’s conversion rate is almost always cheaper.

How do I decline dynamic currency conversion?

When a terminal or ATM presents a currency choice, select the local currency option rather than your home currency. If the screen defaults to your home currency, look for a button or option to change it before confirming.

Does declining DCC mean I pay no fees at all?

Not necessarily. Your card issuer may still charge a foreign transaction fee even when you pay in local currency. Using a card with no foreign transaction fees, such as those from Starling Bank or Monzo, removes this charge entirely.

Can merchants force me to accept dynamic currency conversion?

No. Travellers have the right to decline DCC and opt for their card issuer’s conversion instead. If a terminal does not offer a clear choice, ask the cashier to process the payment in local currency.