Currency hedging for travellers is the practice of managing foreign exchange risk by securing a rate or splitting currency purchases to protect your holiday budget from adverse exchange rate movements. The industry term is “foreign exchange risk management,” and understanding it is the first step to spending less on your next trip abroad. For UK travellers, the stakes are real. The pound’s value against the euro, US dollar, or Turkish lira can shift significantly between the day you book a holiday and the day you land. Currency hedging gives you tools to reduce that uncertainty, whether you are heading to Florida, the Algarve, or Bangkok.

How does currency hedging work for travellers?

Currency hedging works by reducing the time gap between agreeing to spend in a foreign currency and actually converting your pounds. FX risk emerges from this timing gap, not simply from the act of exchanging money. The longer the gap between booking and travelling, the greater the potential for rates to move against you.

Two practical methods dominate travel currency strategies for UK holidaymakers.

-

Split-exchange method. You exchange roughly half your planned spending money shortly after booking, then convert the remainder closer to your departure date. This approach limits losses if rates worsen, while still allowing you to benefit if rates improve on the second portion. It requires no specialist product and works with any reputable travel money provider.

-

Forward contracts. A forward contract lets you lock today’s exchange rate for a conversion that settles on a future date. Forward contracts typically settle from the third business day after agreement. Banks and some specialist currency brokers offer these, though availability for personal travellers varies by provider.

The split-exchange method suits most UK holidaymakers because it requires no upfront premium and no specialist account. Forward contracts suit travellers with large, fixed payments to make in a foreign currency, such as a villa deposit or a prepaid tour package.

Pro Tip: When you plan currency exchange in advance, even a simple split across two purchase dates can meaningfully reduce your exposure to a sudden rate drop.

Timing matters enormously. Hedging is most effective when you have months between booking and travel. Hedging is less worthwhile for imminent trips because exchange rate movements over short timeframes are limited, reducing any potential benefit.

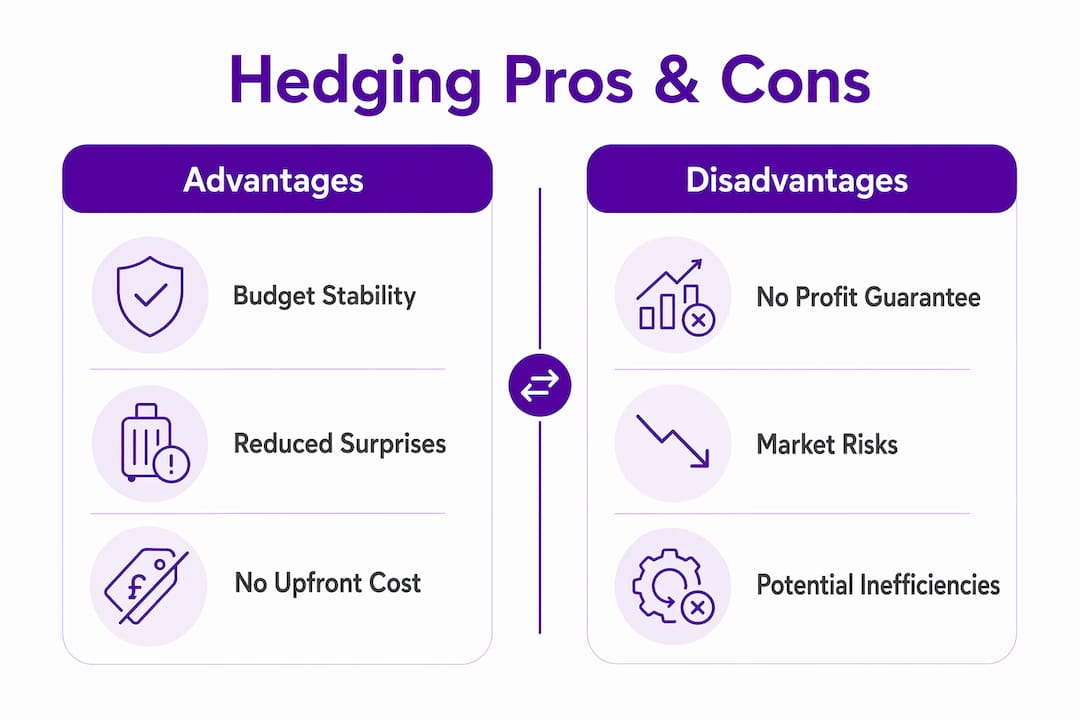

What are the advantages and disadvantages of hedging currency for trips?

Hedging travel money delivers one primary benefit: budget certainty. You know what your holiday costs in pounds before you leave. That predictability is particularly valuable for longer trips or destinations with volatile currencies.

Key advantages:

- Fixed costs become genuinely fixed. A prepaid villa deposit converted at a locked rate will not cost you more if sterling weakens.

- Reduces financial stress. You can plan spending without constantly checking exchange rate apps.

- Protects against sudden political or economic shocks that can move currencies sharply overnight.

- Partial hedging through split-exchange costs nothing extra beyond the standard spread on your travel money.

Key disadvantages:

- Forward contracts involve a trade-off between certainty and flexibility. If the pound strengthens after you lock a rate, you miss out on a better deal.

- Premiums or wider spreads may apply on forward-style products, adding a cost to the certainty you gain.

- Over-hedging creates idle currency. Converting too much in advance leaves you with leftover foreign cash that costs money to buy back.

- Hedging variable or unpredictable spending is inefficient and can waste money.

Pro Tip: Hedging reduces surprises rather than guaranteeing savings. Traveller advice consistently emphasises that the goal is planning certainty, not speculative profit from currency movements.

The most common pitfall is treating hedging as a way to “beat” the market. It is not. It is a way to remove uncertainty from your travel budget so you can focus on the holiday itself.

Which travel expenses should you hedge and why?

Not every pound you spend abroad deserves the same treatment. Forward-style hedging suits large, fixed costs such as deposits and prepaid tours, while day-to-day spending is better left flexible. The table below shows how to categorise your travel expenses.

| Expense type | Hedge it? | Reason |

|---|---|---|

| Villa or hotel deposit | Yes | Fixed amount, fixed date, high value |

| Prepaid tour or excursion | Yes | Known cost, paid in advance |

| Flight ancillaries in foreign currency | Yes | Fixed and predictable |

| Daily food and drink | No | Variable amount, impossible to predict |

| Shopping and souvenirs | No | Discretionary, amount unknown |

| Local transport | No | Small, variable, flexible |

| Emergency cash buffer | No | Needs to remain liquid and accessible |

Hedging variable amounts leads to inefficiencies and idle currency balances. The discipline is to hedge only what you can measure and predict. If you know you are paying £2,000 for a prepaid safari in Kenya, that is a candidate for a forward contract or early exchange. If you are budgeting roughly £50 a day for meals, leave that flexible.

Locking in rates for significant fixed payments stabilises your overall budget without sacrificing the flexibility you need for daily spending. This targeted approach also prevents you from converting more currency than you actually use, which costs money when you sell it back.

How to implement travel currency strategies as a UK traveller

Applying hedging in practice does not require a financial adviser. These steps cover the core approach for most UK holidaymakers.

- Identify your fixed foreign currency costs. List every prepaid expense in the destination currency: deposits, tours, transfers, and accommodation paid upfront. These are your hedgeable exposures.

- Split your discretionary budget into two tranches. Convert the first half shortly after booking. Convert the second half four to six weeks before departure. This is the split-exchange method in practice.

- Use a forward contract for large fixed payments. Contact your bank or a specialist currency broker if you have a single large payment to make in a foreign currency. Confirm whether a personal forward contract is available and what the total cost is, including any spread or fee.

- Compare rates before every purchase. Rates vary significantly between providers. Comparetravelcash lets you compare travel money rates across multiple UK suppliers in one place, so you are not guessing which provider offers the best deal.

- Always pay in local currency at card terminals abroad. Dynamic currency conversion at foreign terminals applies heavily marked-up exchange rates. Choosing to pay in the local currency uses your card network’s rate instead, which is almost always cheaper.

- Consider a prepaid multi-currency card for daily spending. These cards let you load foreign currency at a competitive rate before you travel, separating your daily spending from your hedged fixed costs. They also reduce the risk of carrying large amounts of cash.

- Monitor rates but set a target. Decide in advance what rate you would be satisfied with for your second tranche. If rates hit that level, convert. Avoid obsessing over daily movements.

For longer trips or larger budgets, partial pre-funding through forward contracts is more realistic than locking all currency at once. It preserves flexibility and prevents over-hedging. Separating your budgeting decisions from your day-to-day spending decisions gives you better control over total travel costs.

Why hedging is really about peace of mind, not profit

Having spent years writing about travel money for UK holidaymakers, I have seen the same mistake repeated constantly. Travellers treat currency hedging as a way to win against the market. They agonise over whether to convert now or wait for a better rate. They end up doing nothing, then panic-buy currency at the airport at a terrible rate.

The honest truth is that hedging is not about profit. It is about removing a variable from your holiday budget that you cannot control. When you lock in the rate for your villa deposit or your prepaid tour, you are not trying to beat the bank. You are simply making sure that a 10% swing in sterling does not turn a well-planned holiday into a financial headache.

The split-exchange method is the most practical tool for most UK travellers because it requires no specialist product and no minimum amount. You do not need a broker or a forward contract account. You just need to understand how currency fluctuations affect travellers and act on that knowledge early.

The other mistake I see regularly is ignoring execution costs. You can plan a perfect hedging strategy and then lose a chunk of it to dynamic currency conversion at a restaurant terminal in Lisbon. Always pay in local currency. Always. That single habit saves more money for most travellers than any sophisticated hedging strategy.

Plan ahead, hedge what you can measure, stay flexible on the rest, and pay in local currency every time. That is the entire strategy, and it works.

— Jason

How Comparetravelcash supports your currency planning

Planning your travel money strategy is straightforward when you have the right tools. Comparetravelcash compares live buy and sell rates from multiple UK travel money providers, so you can see at a glance which supplier offers the best rate for your destination currency today.

Whether you are looking to buy euros for a summer break, US dollars for a transatlantic trip, or want to check prepaid multi-currency cards for managing daily spending abroad, Comparetravelcash puts the comparison in one place. You can also check current travel money rates across providers to time your purchases more effectively. Avoid airport rates, avoid hidden markups, and go into your next trip knowing your money is working as hard as possible.

FAQ

What is currency hedging for travellers in simple terms?

Currency hedging for travellers means converting or locking foreign currency in advance to protect your holiday budget from exchange rate movements. The goal is budget certainty, not profit.

Is the split-exchange method suitable for all UK travellers?

The split-exchange method suits most UK travellers planning trips at least a few weeks in advance. It costs nothing extra and reduces exposure to rate movements without requiring specialist financial products.

When does a forward contract make sense for a holiday?

A forward contract makes sense when you have a large, fixed payment to make in a foreign currency, such as a villa deposit or prepaid tour. It locks today’s rate for a future conversion, removing uncertainty from that specific cost.

Should I hedge my daily spending money?

Daily spending is variable and unpredictable, so hedging it leads to inefficiencies and leftover currency. Focus hedging on fixed, known costs and leave discretionary spending flexible.

What is dynamic currency conversion and why should I avoid it?

Dynamic currency conversion is when a foreign card terminal converts your payment into pounds at the merchant’s exchange rate rather than your card network’s rate. The merchant rate is almost always worse, so always choose to pay in the local currency instead.