The interbank rate is the wholesale price at which banks lend money to one another and trade currencies between themselves, with no markups or retail fees attached. You will never see this rate quoted at a bureau de change or airport kiosk. What you see instead is a derived version, adjusted upward to cover the provider’s costs and profit. Understanding interbank rates is the single most useful piece of financial knowledge for anyone exchanging currency, whether you are a student heading abroad, an expat sending money home, or a UK holidaymaker buying euros before a summer trip.

The industry also refers to this rate as the mid-market rate or spot rate. All three terms describe the same concept: the true midpoint between what buyers and sellers are willing to pay in the global foreign exchange market at any given moment. Platforms like EBS and Reuters Matching are where this price discovery actually happens, processing vast volumes of currency trades between major banks every second.

How do interbank rates and the interbank market actually work?

The interbank market is a decentralised, global network where banks trade currencies and lend funds to one another. There is no central exchange. Instead, major institutions connect directly or through electronic platforms, competing continuously on price.

Interbank lending is mostly short-term, ranging from overnight to seven days, and banks use it primarily to manage daily liquidity and meet regulatory reserve requirements. A bank that ends the day short of cash borrows from one with a surplus. The rate agreed between them is the interbank lending rate, which benchmarks products like mortgages and business loans across the wider economy. Historically, LIBOR served this function globally; it has since been replaced by alternatives such as SOFR in the United States.

On the foreign exchange side, over 70% of interbank transactions occur via electronic platforms like EBS or Reuters Matching. That scale means prices update in milliseconds, with anonymity and credit risk managed automatically by the platform. The key instruments traded include:

- Spot contracts: currency exchanged immediately at the current rate

- Forward contracts: currency exchanged at a fixed rate on a future date

- Currency swaps: simultaneous buy and sell of a currency at different dates

- Options: the right, but not the obligation, to exchange at a set rate

Access to this market is not open to the public. Prime brokerage relationships, large minimum trade sizes, and established credit lines are required to participate. Retail customers see only aggregated prices, already marked up by the time they reach a comparison site or high street provider.

Interbank rates vs retail exchange rates: what is the real difference?

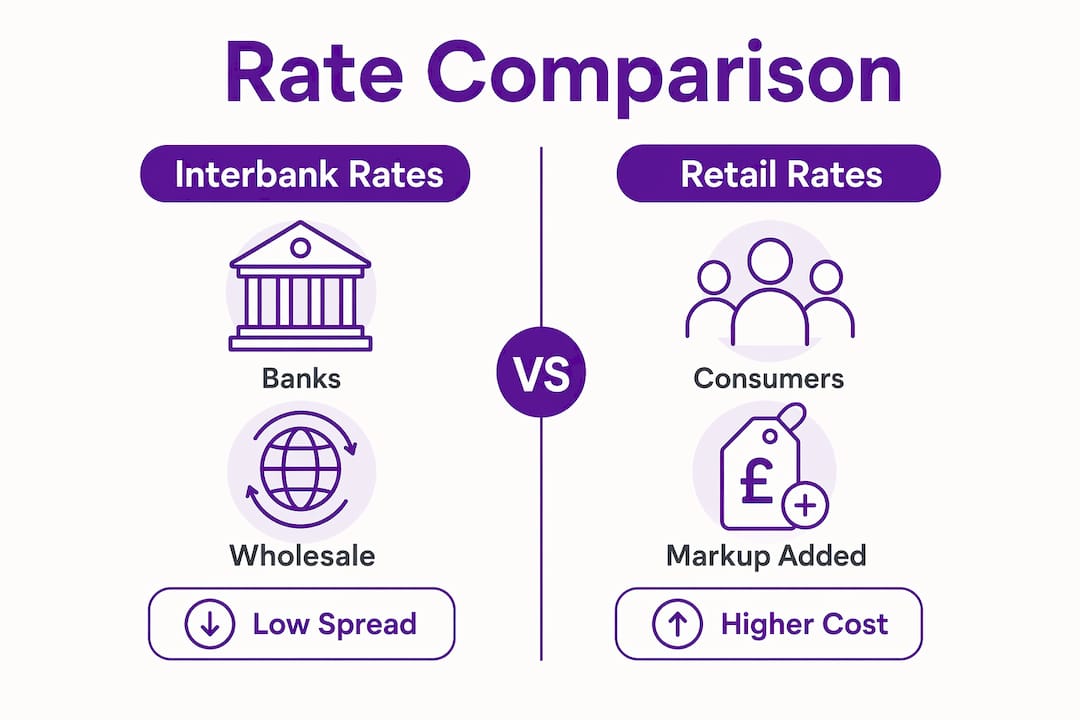

The gap between the interbank rate and the rate you are offered is where providers make their money. The mid-market rate is the fairest indication of currency value, sitting exactly halfway between the buy and sell prices in the global market. Retail providers add a margin on top of this reference rate before quoting you a price.

Here is a simple comparison to illustrate how this works in practice:

| Rate type | Who uses it | Typical spread |

|---|---|---|

| Interbank (mid-market) rate | Banks and liquidity providers | Extremely tight, fractions of a percent |

| Online specialist provider | Consumers via comparison sites | 0.5%–1.5% above mid-market |

| High street bank | Walk-in retail customers | 2%–4% above mid-market |

| Airport bureau de change | Last-minute travellers | 5%–10% above mid-market |

The figures above are illustrative ranges based on general market knowledge, not published data. The core point is directional: the further you are from the interbank market, the more you pay.

Providers that hide their profit margin inside the exchange rate rather than showing a separate fee are generally more expensive and less transparent. A provider advertising “zero commission” is not offering you the interbank rate. The commission is simply embedded in the rate itself.

Pro Tip: Check the live mid-market rate on Google Finance or XE.com before you buy any currency. Compare it to the rate you are being offered. A gap of more than 1% above mid-market is a signal to shop around.

You can read more about exchange rate terminology to get comfortable with terms like bid, ask, spread, and markup before you commit to any provider.

What factors cause interbank rates to move throughout the day?

Interbank rates are not fixed. They shift constantly in response to supply and demand, economic news, and the ebb and flow of global trading sessions.

Central banks are the most powerful single influence on interbank lending rates. Institutions like the Bank of England and the US Federal Reserve set target bands for short-term borrowing costs. When market rates drift outside those bands, the central bank intervenes directly, either injecting liquidity or absorbing it, to pull rates back into range. This is how monetary policy transmits into the real economy.

On the foreign exchange side, the key drivers of intraday movement include:

- Trading session overlap: the London and New York overlap (roughly 1pm–5pm UK time) is the most liquid period of the day. Spreads are tightest here.

- Economic data releases: inflation figures, employment reports, and central bank announcements cause sharp, immediate rate moves.

- Geopolitical events: elections, conflicts, and unexpected policy shifts create sudden demand for safe-haven currencies like the US dollar or Swiss franc.

- Low liquidity periods: during Asian hours or public holidays, spreads widen and volatility increases, pushing retail rates further from the interbank benchmark.

Interbank rates are quoted to five decimal places during liquid sessions, with competition among major banks keeping spreads extremely tight. That precision matters less to retail customers, but it illustrates how efficient the wholesale market is compared to what consumers experience.

The practical implication is straightforward. If you exchange currency during a low-liquidity period, you are likely to receive a worse rate than if you transact during peak London or New York hours.

Practical steps for getting a fairer rate when exchanging currency

Knowing how the interbank market works gives you a real advantage when buying travel money. The goal is not to access the interbank rate directly. That is not possible for retail customers. The goal is to minimise the gap between the interbank rate and the rate you actually receive.

Follow these steps to reduce unnecessary cost:

-

Check the mid-market rate first. Look up your currency pair on Google Finance or XE.com before approaching any provider. This gives you a baseline for comparison.

-

Calculate the markup. Divide the mid-market rate by the rate you are being offered. A result below 1 means you are paying a markup. A gap exceeding 1% above mid-market is a meaningful cost worth avoiding.

-

Compare multiple providers. Rates vary significantly between providers. A comparison platform like Comparetravelcash lets you see live rates from multiple UK suppliers side by side, so you are not relying on a single quote.

-

Avoid airport and hotel exchanges. These consistently offer the widest spreads. The convenience comes at a measurable cost.

-

Consider a prepaid currency card. Prepaid multi-currency cards often load currency at rates closer to the mid-market rate than high street providers. They also protect you from carrying large amounts of cash.

-

Check buyback rates before you travel. If you return with leftover currency, the rate at which a provider buys it back matters. Buyback rates vary as much as buy rates do, and comparing them in advance saves money on the return leg.

Pro Tip: Timing your purchase matters. Rates shift throughout the day. If you are not in a rush, monitor rates over a few days using a rate alert tool and buy when the rate moves in your favour.

Spotting bad exchange rates before you commit is a learnable skill. The more familiar you become with the mid-market rate as your reference point, the easier it is to identify when a provider is offering poor value.

Why I think most people misunderstand what “no fees” actually means

The phrase “no fees” is one of the most misleading in currency exchange. Consumers read it and assume they are getting something close to the interbank rate. They are not. The spread between the mid-market rate and the offered rate is the main profit channel for banks and providers, and it is invisible unless you know to look for it.

I have seen this play out repeatedly. A traveller walks past a bureau de change displaying “0% commission” in large letters, exchanges £500, and loses £30 to £40 in the embedded markup without realising it. That is not a fee. It is a rate adjustment. The distinction is semantic, but the cost is real.

The interbank market itself has become far more efficient over the past two decades. Electronic platforms like EBS have compressed spreads at the wholesale level to fractions of a percent. The problem is that this efficiency does not automatically pass through to retail customers. Providers absorb the benefit and maintain their margins.

What has changed is transparency. Tools like rate comparison sites and mid-market trackers give ordinary consumers a reference point that simply did not exist in a practical form twenty years ago. Using them is not complicated. It takes thirty seconds to check the mid-market rate before you buy. That thirty seconds can save you a meaningful sum on any sizeable exchange.

My advice is simple: treat the mid-market rate as the price of the currency, and treat any markup as the cost of the service. Once you frame it that way, comparing providers becomes straightforward. You are just comparing service costs.

— Jason

Where to compare live travel money rates in the UK

Understanding the interbank rate is only half the job. The other half is finding a provider whose retail rate sits as close to that benchmark as possible.

Comparetravelcash aggregates live rates from multiple UK travel money providers, so you can see at a glance who is offering the best deal for your currency. Whether you are buying euros, US dollars, or Thai baht, the platform shows you the full picture without you having to visit each provider individually. You can check Hays Travel rates or The Currency Club rates directly, compare prepaid card options, and review buyback rates for any leftover currency when you return. Compare travel money rates now and see how much difference the right provider makes.

FAQ

What is the interbank rate in simple terms?

The interbank rate is the wholesale exchange rate banks use when trading currencies with one another. Retail customers cannot access it directly and always pay a marked-up version.

Is the interbank rate the same as the mid-market rate?

Yes. The interbank rate, mid-market rate, and spot rate all refer to the same thing: the midpoint between the buy and sell prices in the global forex market at a given moment.

Why do consumers pay more than the interbank rate?

Retail providers add a markup to the interbank rate to cover their costs and generate profit. This margin is often embedded in the rate itself rather than shown as a separate fee.

How can I check the current interbank rate?

Google Finance, XE.com, and similar tools display the live mid-market rate for most currency pairs. Use these as your reference before buying travel money from any provider.

Does the interbank rate change throughout the day?

Yes. Interbank rates fluctuate continuously based on supply and demand, economic news, and trading session liquidity. Spreads are tightest during the London and New York session overlap.