A multi-currency card is a single payment card that holds and spends multiple foreign currencies from separate digital wallets, eliminating the need to carry several cards or exchange cash at every border. These cards come in two main forms: prepaid cards, such as those offered by Wise and FairFX, and debit or credit-linked cards from providers like Starling Bank. Both types have grown sharply in popularity among UK travellers and expatriates who want to control spending costs abroad without being ambushed by poor exchange rates. Understanding how they work, what they cost, and when to use them is the difference between saving money and quietly losing it.

How do multi-currency cards work?

Multi-currency cards automatically debit the correct currency wallet at the point of sale, rather than converting your pounds on the spot like a standard debit card does. This is the core mechanic that makes them useful. When you tap your card at a café in Paris, the card checks whether you hold euros in your wallet and charges from that balance directly. No conversion takes place, and no markup is applied.

The process differs slightly depending on card type:

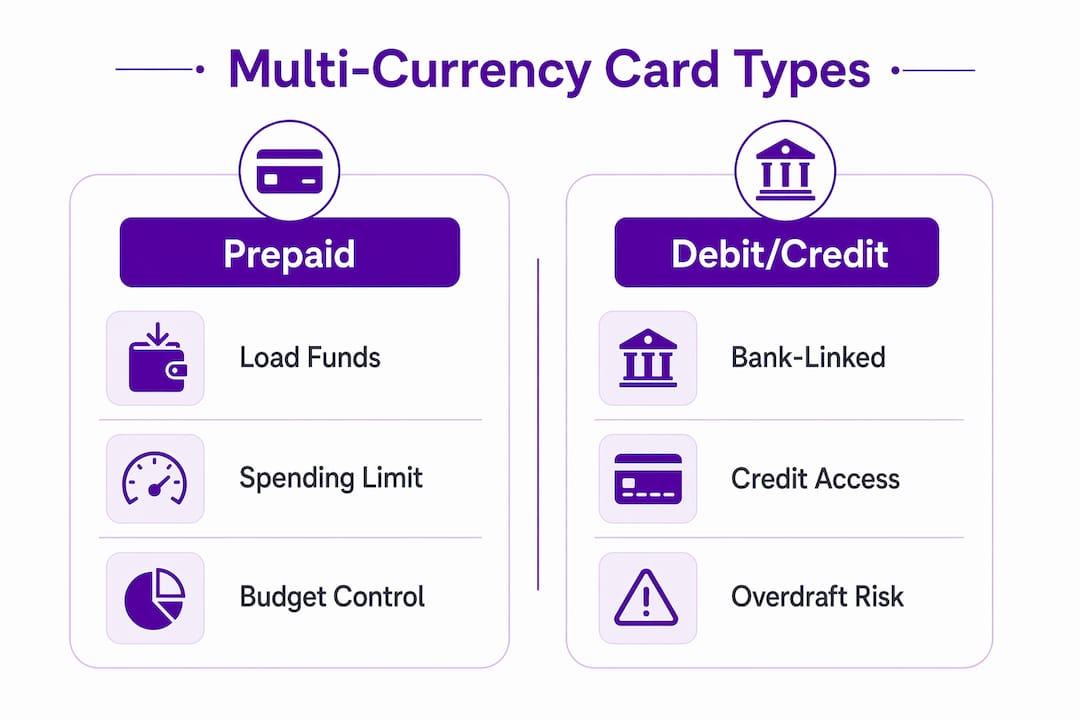

- Prepaid cards require you to load funds before travel. You top up specific currencies at the exchange rate available at that moment, locking in that rate for future spending.

- Debit and credit-linked cards draw from your account in real time, converting at the live mid-market rate or a small margin above it, without requiring pre-loading.

- Fallback conversion occurs when your matching currency wallet is empty. The card auto-converts from another wallet, which can trigger unexpected fees depending on your provider’s policy.

One trap that catches many travellers is Dynamic Currency Conversion, or DCC. This happens when a foreign merchant or ATM offers to charge you in pounds rather than the local currency. DCC typically imposes poor exchange rates, eroding the very savings your card was designed to protect. Always select the local currency option at the terminal.

Pro Tip: When an ATM or card machine asks whether you want to pay in pounds or the local currency, always choose the local currency. Choosing pounds hands the exchange rate calculation to the merchant, not your card provider.

What are the main types of multi-currency cards?

Prepaid multi-currency cards require funds to be loaded before use and will decline transactions if the balance runs out. This limitation is also their strength: you cannot overspend, which makes them a reliable budgeting tool. Debit and credit-linked multi-currency cards offer more flexibility, drawing directly from your bank account or credit line and converting currencies in real time. The trade-off is less predictability over the exact rate you will receive.

Here is a direct comparison of the two types:

| Feature | Prepaid multi-currency card | Debit/credit-linked card |

|---|---|---|

| Currency loading | Pre-loaded before travel | Real-time conversion at purchase |

| Budgeting control | High. Spend only what you load | Lower. Draws from account balance |

| Exchange rate certainty | Locked in at time of loading | Variable, based on live rates |

| Flexibility | Lower. Requires planning ahead | Higher. No pre-loading needed |

| Typical fees | Loading fees, ATM charges, inactivity fees | Conversion margins, possible ATM fees |

| Security if lost | Card blocked; loaded funds protected | Card blocked; account funds protected |

| Best for | Budget-conscious travellers, multi-destination trips | Frequent travellers, spontaneous spending |

Prepaid cards offer budgeting control by limiting spending to loaded funds, whereas debit and credit-linked cards provide convenience with real-time currency conversions. Neither type is universally superior. A traveller visiting three countries in two weeks benefits from pre-loading euros, US dollars, and Thai baht on a prepaid card. A business traveller making irregular trips to unpredictable destinations may prefer the flexibility of a linked card.

Security is a genuine advantage for both types. Multi-currency cards use chip and PIN technology and can be blocked immediately if lost or stolen, unlike cash, which is gone for good the moment it leaves your wallet.

How to manage multiple currencies on one card

Effective management of a multi-currency card starts before you board the plane. Follow these steps to get the most from your card without paying avoidable fees.

- Research your destination currencies. Identify every currency you will need and check whether your card supports them. Multi-currency cards typically support major currencies including USD, EUR, GBP, AUD, CAD, and JPY, covering most popular travel destinations.

- Load currencies at the right time. Timing your reloads to lock in favourable rates matters. Loading too early risks exchange rate fluctuations working against you; loading at the last minute at an airport kiosk almost always means a worse rate.

- Avoid over-loading. Load a realistic estimate of your spending, not the maximum you might conceivably spend. Unused balances left on a card can lose value if exchange rates shift, and some providers charge inactivity fees after a set period.

- Top up mid-trip when rates are favourable. Most prepaid card apps let you reload remotely. If the rate improves during your trip, topping up then rather than before departure can save a meaningful amount on longer stays.

- Use ATMs strategically. Withdraw larger amounts less frequently rather than small amounts often, since many cards charge a flat fee per ATM transaction. Check your provider’s fee schedule before travel so you know the threshold where cash withdrawals become cost-effective versus paying by card.

- Always pay in local currency. Refusing DCC at every terminal is the single most consistent way to protect the savings your card provides.

Pro Tip: Before travelling, download your card provider’s app and set up rate alerts. Many providers, including Wise, notify you when a target exchange rate is reached, letting you load at the optimal moment rather than guessing.

What fees and charges should you expect?

Multi-currency cards do not guarantee zero fees. Fee schedules vary widely between providers and have a direct impact on the overall value of the card. Knowing what to look for before you sign up prevents unpleasant surprises on your statement.

Common charges to check before choosing a card:

- Issuance fee: A one-off charge to receive the physical card, ranging from free to around £10 depending on the provider.

- Loading fee: Some providers charge a percentage of the amount you load, typically between 0.5% and 2%.

- ATM withdrawal fee: Usually a flat fee per withdrawal, often between £1.50 and £2, sometimes with a free monthly allowance.

- Currency conversion margin: When you spend in a currency you have not pre-loaded, the provider converts from your default wallet at a rate that includes a markup above the mid-market rate.

- Inactivity fee: Charged monthly after a period of no card use, typically six to twelve months. This quietly erodes balances on cards you forget about after a trip.

- Fallback conversion fee: Using a secondary currency wallet triggers hidden fees with some providers, so understanding your card’s fallback policy is not optional reading.

The exchange rate margin deserves particular attention. A card advertised as having no foreign transaction fee may still apply a 1.5% to 2.5% markup on the mid-market rate during conversion. That markup is the fee. Comparing the effective rate you receive, not just the listed charges, gives you the true cost of using a card. Comparetravelcash publishes up-to-date rate comparisons across providers, which makes this calculation straightforward rather than a guessing game.

My honest view on multi-currency cards for UK travellers

Multi-currency cards are genuinely useful for a specific type of traveller: someone visiting two or more countries, spending in predictable amounts, and willing to spend ten minutes loading currencies before departure. For that person, the savings over a standard debit card are real and consistent.

Where I see travellers go wrong is treating these cards as a set-and-forget solution. The fallback conversion problem is more common than providers advertise. If you run out of euros in Rome and your card silently converts from your dollar wallet at an unfavourable rate, you have lost the advantage you signed up for. Knowing your card’s fallback policy is as important as knowing the loading fee.

I also think the comparison between multi-currency cards and multi-currency accounts is worth making. Accounts give you more control over currency management and often better rates for larger sums, which suits expatriates more than occasional travellers. For a two-week holiday, a prepaid card is the more practical choice. For someone living between London and Barcelona, a full multi-currency account may serve better.

The travel payment space in 2026 has matured considerably. Providers have improved their apps, fee transparency has increased under regulatory pressure, and the best prepaid travel cards now offer genuinely competitive rates. The key is still comparison. No single card is best for every traveller, and the difference between a good deal and a poor one often comes down to one or two percentage points on the conversion rate.

— Jason

Find the best multi-currency card deals before you travel

Choosing the right card without comparing rates first is the most common and most avoidable mistake UK travellers make.

Comparetravelcash makes it straightforward to compare currency card deals across multiple providers in one place, so you can see the real rates and fees side by side before committing. The platform also tracks live travel money rates, helping you time your currency loading to get more for your pounds. Whether you are heading to Europe, the US, or further afield, checking the comparison tools at Comparetravelcash before you travel takes minutes and can save you a meaningful amount over the course of a trip. You can also review currency conversion fees in detail to understand exactly what each provider charges.

FAQ

What is a multi-currency card?

A multi-currency card is a payment card that holds multiple foreign currencies in separate digital wallets, allowing you to spend in each currency without triggering a conversion fee at the point of sale.

How do multi-currency cards differ from standard debit cards?

Standard debit cards convert your pounds to the local currency at every transaction, usually at a marked-up rate. Multi-currency cards debit the matching currency wallet directly, avoiding that conversion step when the correct currency is loaded.

Are multi-currency cards free to use abroad?

Not always. Typical fees include issuance, loading, and ATM charges, plus a conversion margin when spending in a currency you have not pre-loaded. Reading the full fee schedule before choosing a card is the only way to know the true cost.

What happens if I spend in a currency I have not loaded?

The card falls back to another wallet and converts automatically, which can trigger unexpected conversion fees depending on your provider’s policy. Loading the currencies you expect to use before travel prevents this.

Is a prepaid multi-currency card safer than cash?

Yes. Chip and PIN protection and instant card blocking mean that a lost or stolen card can be secured immediately, whereas lost cash cannot be recovered. Most providers also offer a replacement card service for travellers abroad.