Exchanging currency used to mean queuing at a bureau de change, accepting whatever rate was posted on the board, and hoping the airport kiosk wasn’t as bad as everyone said it was. The role of fintech in travel money has changed that picture significantly. Financial technology, or fintech, is the industry term for software-driven tools that deliver banking, payments, and currency exchange services digitally. For UK holidaymakers, expats, and students heading abroad, these tools now offer real-time exchange rates, multi-currency accounts, and app-based spending that were simply not available a decade ago. This guide cuts through the noise and explains what fintech actually does for your travel money, what it costs, and where the traps still lie.

Table of Contents

- How fintech simplifies currency exchange abroad

- Comparing fintech travel money products

- Fintech behind the scenes: payment infrastructure

- Travel money strategies for different traveller types

- Fintech travel money limitations to know

- My take on fintech and travel money

- Compare your travel money options with Comparetravelcash

- FAQ

How fintech simplifies currency exchange abroad

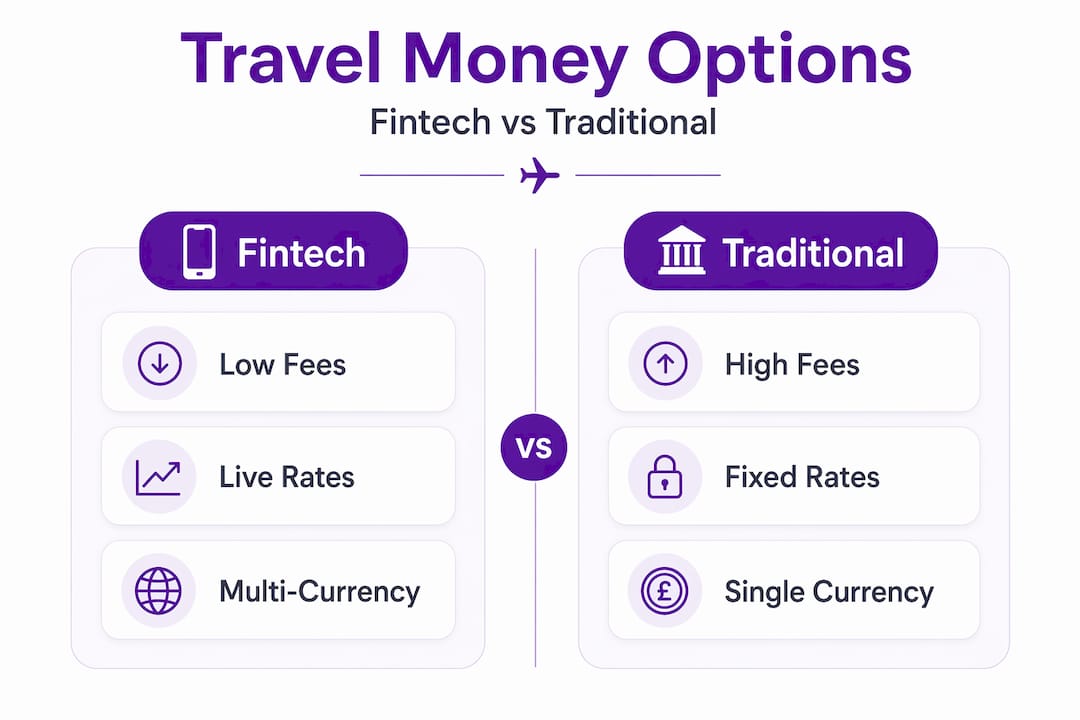

The core promise of fintech in travel money is transparency. Traditional currency exchange layers profit into the rate itself, so you rarely know how much you are actually paying. Fintech apps changed the conversation by displaying the mid-market rate, which is the real exchange rate you see on Google, and then charging fees separately rather than hiding them inside a marked-up rate.

Multi-currency wallets

Multi-currency accounts let you hold balances in different currencies at the same time. Wise supports 40+ currencies with mid-market exchange rates, meaning you can convert pounds to euros, dollars, or Thai baht at the real rate and hold that balance until you need it. That is genuinely useful if you are travelling across multiple countries or want to lock in a rate before departure.

Revolut works similarly, letting you spend directly from your sterling balance and converting at the point of purchase. The key difference is that Revolut’s rates are not always mid-market. Weekend fees apply from Friday 5pm to Sunday 6pm ET, with Standard plan users paying a 1% markup and Plus users paying 0.5%. Premium and Metal plan holders avoid weekend fees, but those plans carry a monthly subscription cost. This is the detail most travellers miss when they assume fintech always means cheap.

Spending abroad with fintech cards

Fintech cards generally beat traditional debit and credit cards for overseas spending. Most high-street banks still apply foreign transaction fees of 2.75% to 3% on every purchase abroad. Fintech options typically remove that charge entirely within their free-use thresholds.

The catch is that free-use thresholds exist. Revolut’s Standard plan includes a monthly fee-free ATM withdrawal allowance, beyond which fees apply. Plan-dependent FX limits mean heavy users can find their “free” product becomes quite costly if they exceed those caps. Always check the small print before you travel.

Pro Tip: Convert currency mid-week, before Friday evening, if you use Revolut on a Standard or Plus plan. You will avoid the weekend markup entirely.

Comparing fintech travel money products

Understanding the differences between fintech platforms matters as much as choosing one. They are not all built the same way, and the cheapest option for a short city break might be the wrong choice for a three-month stint abroad.

| Feature | Revolut (Standard) | Revolut (Premium+) | Wise |

|---|---|---|---|

| Exchange rate | Mid-market (weekdays) | Mid-market (always) | Mid-market (always) |

| Weekend markup | 1% surcharge | None | None |

| Monthly fee | Free | £7.99+ per month | None (pay-per-use) |

| ATM withdrawals | Limited free allowance | Higher free allowance | £200 free per month |

| FSCS protection | Yes (banking licence) | Yes (banking licence) | Safeguarded (not FSCS) |

| Cash withdrawal fee (over limit) | 2% | 2% | 1.75% |

Revolut’s UK banking licence now means deposits are protected by the Financial Services Compensation Scheme (FSCS) up to £120,000. That is a meaningful shift in trust for anyone keeping larger travel money balances in the app. Wise operates differently. It holds client money in safeguarded accounts under the FCA’s e-money rules, which offers protection but is not the same as FSCS deposit insurance. For most travellers holding a few hundred pounds, this distinction is unlikely to matter. For expats holding thousands, it is worth knowing.

Wise’s pay-per-use pricing with mid-market rates and no hidden weekend surcharges suits irregular travellers well. There is no subscription to justify. You pay a small, clearly displayed fee per transfer and that is it. For frequent travellers or those making regular transfers, Revolut’s paid tiers can work out cheaper at higher volumes.

Pro Tip: If you are unsure which plan suits you, add up your expected monthly foreign currency spend and compare it against the subscription cost. The maths is usually straightforward.

Fintech behind the scenes: payment infrastructure

Most travellers only think about fintech at the point of spending. But there is a layer of financial technology working behind the scenes that directly affects your experience as a customer, specifically on booking platforms and travel websites.

Payment orchestration is the technical term for systems that manage how payments are routed, processed, and recovered when things go wrong. Juspay reduced payment declines and refund times for a major global travel platform by consolidating fragmented payment flows into a single system. That is what payment orchestration does for travellers:

- It supports 300+ local payment methods, meaning you can pay using local wallets, bank transfers, or cards depending on where you are booking from.

- Dynamic routing increases authorisation rates by up to 10%, so fewer legitimate transactions are declined at checkout.

- Faster refund processing means money comes back to you quicker when a booking falls through.

- Consolidation reduces technical failures during high-traffic booking periods, such as holiday sales.

The benefit to you as a traveller is often invisible. You simply experience fewer payment errors, faster confirmations, and more payment options at checkout. Behind every smooth transaction on a travel booking site, there is usually a fintech infrastructure provider making that possible.

Travel money strategies for different traveller types

Getting value from fintech tools depends on how you travel. A package holiday to Spain for two weeks looks nothing like an expat managing salary conversions in Dubai. Here is how to approach travel money management for your situation.

-

Short-break holidaymakers: Load your fintech card before you leave and convert mid-week to avoid any weekend markups. Take a small amount of local cash from a fee-free ATM on arrival. Keep your home bank card as a backup in case of technical issues. Planning weekend exchanges separately and carrying backup cards is the simplest form of travel money risk management.

-

Longer-stay travellers: If you are away for a month or more, your ATM usage will likely exceed the free monthly allowance on standard fintech plans. Check whether upgrading to a paid tier saves money versus paying per-transaction fees. Keep an eye on your monthly spend limits. Use your fintech card for day-to-day spending and rely on a traditional debit card for larger cash needs if the fees are lower at that volume.

-

Expats and overseas students: Your needs go well beyond a spending card. Digital money transfers for salary conversions, rent payments, and sending money home are where fintech genuinely earns its place. Wise in particular is well-regarded for regular international transfers at mid-market rates. Revolut’s subscription plans can offer additional benefits if you are transferring frequently. Having multiple fintech accounts is not overkill. It gives you flexibility when one provider has limitations for a specific currency or country.

-

Students studying abroad: Budget carefully using the spending tracking features built into most fintech apps. Set monthly spending limits within the app before you arrive. Use the currency card for everyday purchases and avoid drawing large sums of cash in countries where card payments are widely accepted. You can also read Comparetravelcash’s tips on exchanging money abroad for practical rate advice before you go.

Fintech travel money limitations to know

Fintech makes travel money better in most cases. It does not make it perfect. The products have real boundaries, and some travellers discover them at the worst possible time.

The biggest risk is assuming one app covers everything. Fee structures differ between spending, withdrawals, and transfers, even within the same app. Revolut charges differently depending on whether you are paying a merchant, withdrawing cash, or sending money to another account. Travellers relying on one fintech app risk surprises from these product boundaries, particularly at the end of the month when fair-usage limits reset. There are also countries and currencies where fintech apps struggle. Some destinations are cash-only. Some currencies are not supported. In those cases, ordering physical currency in advance from a competitive provider remains the right call. Fintech has not replaced cash. It has just reduced how much you need it.

Pro Tip: Before any trip, open your fintech app and check the fee schedule specifically for your destination currency. What applies in Europe may not apply in Asia or South America.

Travel money demand is increasingly tied to convenient distribution points, and fintech is amplifying that, bringing pre-order and app-based travel money closer to the customer. But convenient does not always mean cheapest. Always compare.

My take on fintech and travel money

I’ve seen a lot of travellers get excited about fintech apps and then get caught out by the details. The transparency is real. The savings are real too, in many cases. But what I’ve found over the years is that the people who benefit most are the ones who read the fee schedule before they travel, not after their card gets charged more than they expected.

The shift I’ve noticed most is in how expats and students think about money across borders. A few years ago, sending £500 home or converting a salary meant bank transfer fees and exchange rates you had no control over. Now those same people are using digital transfer services with mid-market rates and paying a fraction of what they used to. That is a genuine improvement in financial access.

My recommendation for most holidaymakers is to use a fintech card for day-to-day spending and supplement it with a small amount of local cash. For expats and students, I’d say go further. Build a proper multi-app setup with at least two fintech providers and understand the limits on each. The goal is having options, not depending on any single product.

Where I’d push back on the fintech hype is around the idea that these products are always cheaper than traditional exchange. They often are. But not always. A high-street travel money provider with competitive rates, particularly for popular currencies like euros and dollars, can still beat a fintech card on the day if you shop around. The smartest move is to compare live exchange rates before you commit to any single method.

— Jason

Compare your travel money options with Comparetravelcash

Understanding how fintech works is only half the equation. Getting the best deal still requires comparing what is actually on offer before you travel.

Comparetravelcash makes it straightforward to see live exchange rates from multiple UK providers side by side, so you can decide whether a fintech card, a prepaid currency card, or a traditional bureau de change gives you the best value for your trip. You can compare travel money rates across dozens of providers in seconds, or check out the prepaid currency card comparison if you want to weigh up multi-currency card options specifically. Whether you are heading to Europe, the US, or further afield, Comparetravelcash helps you avoid the guesswork and make a decision backed by actual numbers.

FAQ

What is the role of fintech in travel money?

Fintech improves travel money by providing multi-currency accounts, app-based real-time exchange rates, and lower-cost card spending abroad. It replaces opaque markups with transparent fees and gives travellers more control over when and how they convert currency.

Are fintech travel cards always cheaper than traditional exchange?

Not always. Fintech cards are often competitive, but weekend markups, plan limits, and ATM fees can add up. Comparing fintech card rates against bureau de change providers before you travel helps you identify the genuinely better deal.

Is my money safe in a fintech travel app?

Revolut now holds a UK banking licence with FSCS protection up to £120,000. Wise operates under FCA e-money rules with safeguarded client accounts. Both offer meaningful protection, though the specifics differ from traditional bank deposit insurance.

Can expats and students use fintech for regular transfers?

Yes. Services like Wise support transfers across 40+ currencies at mid-market rates, making them well-suited for salary conversions, rent payments, and regular remittances at lower costs than most traditional banks.

What are the main fintech travel money pitfalls to avoid?

Weekend currency markups, fair-usage limits on free plans, and varying fees between spending, withdrawals, and transfers are the most common surprises. Reading the fee schedule for your specific destination currency before travel avoids most of them.