Getting maximum value from your travel money is defined by one decision made before you board: choosing the right combination of cards, cash, and loyalty points. Most UK travellers lose money not through extravagance but through avoidable fees, poor exchange rates, and missed rewards. The recommended approach for developed countries is roughly 70% card and 30% cash, shifting to a 50/50 split in cash-heavy regions. Tools like no-foreign-transaction-fee credit cards, fee-reimbursing debit cards, and airline or hotel loyalty programmes are the real ways to get maximum value from travel money. Get these right and your budget stretches considerably further.

How to choose and use travel cards for maximum value

The single most effective card strategy is pairing a no-foreign-transaction-fee credit card with a debit card that reimburses ATM fees. Cards like Chase Sapphire Preferred and the Charles Schwab debit card are widely cited as the lowest-cost combination for spending and withdrawing cash abroad. That pairing eliminates the two biggest card-related costs: the foreign transaction fee on purchases and the ATM surcharge on cash withdrawals.

Daily card use abroad requires a few firm habits:

- Always pay in local currency. Dynamic Currency Conversion adds 3–7% to every transaction. When a card terminal asks whether you want to pay in pounds or the local currency, always choose local currency.

- Carry two credit cards and two debit cards. Store one of each separately from your wallet. A lost bag or a blocked card will not strand you if you have a backup in your hotel safe.

- Use contactless and mobile payments where accepted. Over 85% of card terminals worldwide accepted contactless payments in 2026. That acceptance rate means you face fewer cash-only situations than a decade ago.

- Notify your bank before you travel. A card blocked for suspected fraud is a serious inconvenience abroad. A two-minute phone call or app notification prevents it.

Pro Tip: Set up Apple Pay or Google Pay on your phone before departure. Mobile payments are accepted at most modern terminals and add a layer of security because your actual card number is never transmitted.

The right card infrastructure matters more than the amount of cash you carry. Fees compound quickly across a two-week holiday, and the difference between a card with a 2.99% foreign transaction fee and one with no fee is measurable on any budget.

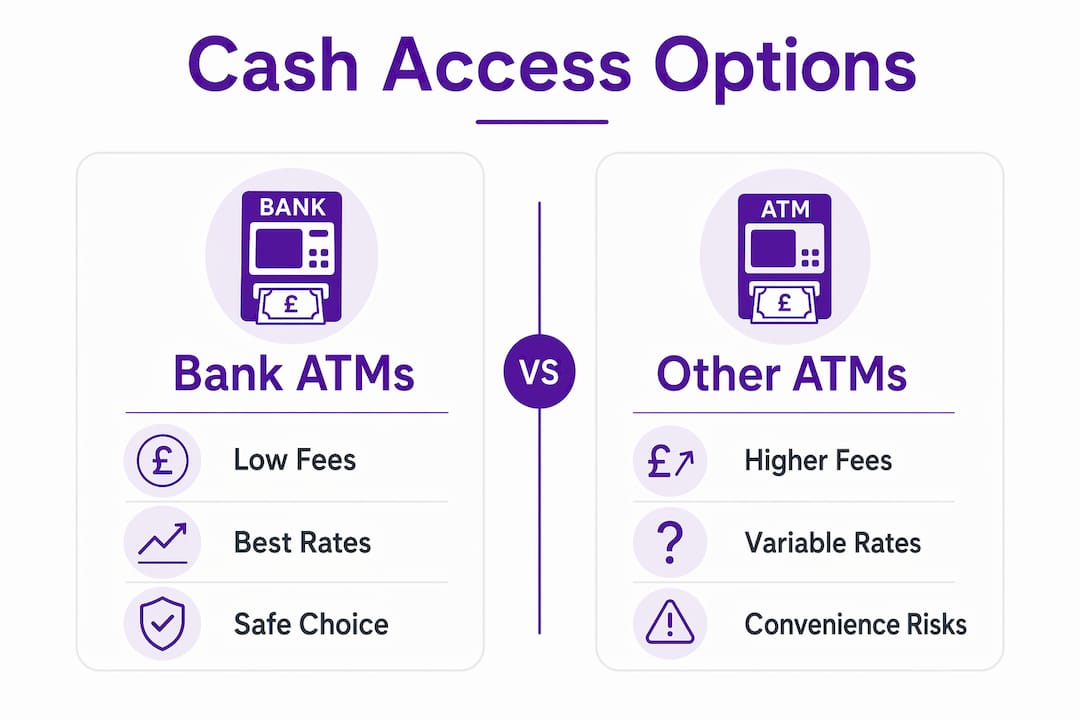

What is the best way to access cash abroad?

Bank-affiliated ATMs give you the best exchange rate available for cash withdrawals. Standalone machines and airport ATMs typically add markups of 8–15% on top of the mid-market rate. That markup is the equivalent of handing over a day’s spending money before you have even left the terminal.

The frequency of your withdrawals matters as much as the location. Withdrawing a larger sum less frequently reduces the number of flat fees you pay. If an ATM charges a flat fee of £3–£5 per transaction, withdrawing £400 once costs far less than withdrawing £100 four times. The maths is straightforward, but most travellers still make small, frequent withdrawals out of habit.

The table below compares the typical costs of different cash access methods:

| Method | Typical markup or fee | Best for |

|---|---|---|

| Bank-affiliated ATM | 0–2% plus possible flat fee | Most destinations |

| Standalone ATM | 7–15% markup | Avoid where possible |

| Airport currency booth | 8–15% markup | Emergency use only |

| Hotel exchange desk | 10–15% markup | Avoid entirely |

| Pre-ordered travel cash | 2–5% depending on provider | First 24 hours of arrival |

Pro Tip: Order a small amount of local currency before you travel to cover taxis, tips, and small purchases on arrival. This removes the pressure to use an airport machine when you land.

Carrying some local currency for your first 24 hours is sensible regardless of your card setup. Small vendors, market stalls, and rural areas in many countries still operate on a cash-only basis. A reasonable float of local notes removes that friction without requiring you to exchange large sums at poor rates. For guidance on getting the best rates before you travel, planning ahead makes a genuine difference.

How do loyalty points multiply your travel budget?

Loyalty points transferred to airline or hotel partners regularly deliver 2 to 5 times the value of redeeming the same points through a credit card’s own travel portal. That difference is not marginal. On a long-haul return flight, the gap between portal redemption and a well-chosen transfer partner can represent hundreds of pounds in effective value.

The mechanism works like this. Credit card points programmes, such as American Express Membership Rewards, allow you to transfer points to partner airlines and hotels at a set ratio. Those partners then let you book award flights or hotel nights at rates that, when converted back to a cash equivalent, far exceed what the portal would offer. The key is identifying what points specialists call “sweet spots”: routes or hotel categories where the award pricing has not kept pace with cash prices.

The most accessible programmes for UK travellers include:

- Flying Blue (Air France and KLM): Regularly runs promotional awards with reduced point costs on transatlantic and European routes.

- World of Hyatt: Consistently rated as one of the highest-value hotel programmes. Points transferred from Chase Ultimate Rewards can book category 1–4 hotels for as few as 3,500–8,000 points per night.

- Avios (British Airways Executive Club): Strong value on short-haul European routes and partner redemptions through Iberia and Aer Lingus.

- Virgin Points (Virgin Atlantic Flying Club): Particularly strong for Upper Class redemptions on Virgin Atlantic and partner airlines including Delta and ANA.

The most common mistake is trying to master every programme at once. Start with the points you already have from one card and plan one trip around redeeming them well. Effective points redemption with transfer partners can multiply your travel budget significantly beyond what portal redemptions offer. That is a principle worth acting on before your next booking.

Common travel money mistakes and how to avoid them

The most expensive travel money mistake is using a card with a foreign transaction fee for all your spending. A 2.99% fee on every purchase adds up to a significant sum across a two-week trip. Switching to a no-fee card before you travel costs nothing and saves a measurable amount.

A numbered list of the most common errors, and their fixes:

- Accepting Dynamic Currency Conversion. Always decline it. Pay in local currency every time. The 3–7% extra cost benefits the merchant’s bank, not you.

- Making frequent small ATM withdrawals. Each withdrawal triggers a flat fee. Withdraw larger amounts less often to reduce the total fee burden.

- Exchanging currency at the airport. Airport bureaux de change apply markups of 8–15%. Order currency in advance or use a bank ATM at your destination instead.

- Travelling with only one card. Cards get lost, blocked, or damaged. Carry at least one backup credit card and one backup debit card stored separately.

- Failing to notify your bank. Banks flag unusual foreign transactions as potential fraud. A quick notification before you travel prevents your card being blocked mid-trip.

- Ignoring buyback rates. If you return with leftover foreign currency, the rate at which you sell it back matters. Comparing currency buyback rates before you travel tells you which provider offers the best deal on both ends of the transaction.

Recognising these errors before your trip is the practical difference between a travel money strategy that works and one that quietly drains your budget. For a deeper look at identifying poor offers, Comparetravelcash has a dedicated guide on spotting bad exchange rates that is worth reading before you book.

My honest view on travel money in 2026

I have watched the travel money conversation shift dramatically over the past decade. When I started travelling regularly, the debate was almost entirely about which bureau de change offered the best rate on the high street. Today, that conversation feels outdated.

The real opportunity for UK travellers now lies in payment infrastructure, not physical cash. The future of travel money is built around having the right cards, the right apps, and a basic understanding of how loyalty points work. Physical cash still matters, particularly in parts of Asia, Africa, and rural Europe, but it is no longer the centrepiece of a sound travel money plan.

What I find most underused is the points transfer strategy. Most UK travellers with an American Express card are sitting on points they redeem for statement credits or Amazon vouchers. Those same points, transferred to Flying Blue or Avios, could cover a return flight to New York or a week in a Hyatt hotel. The complexity is real but manageable. One well-researched redemption changes how you think about every future trip.

My practical advice: spend thirty minutes before your next trip comparing exchange rates, checking your card’s foreign transaction fee, and looking at what your loyalty points are actually worth when transferred. That thirty minutes will almost certainly save you more money than any other pre-travel task.

— Jason

Compare your options before you travel with Comparetravelcash

Knowing the strategies is one thing. Finding the best rates available right now is another. Comparetravelcash aggregates live exchange rates from providers across the UK, so you can see exactly who is offering the most competitive deal before you commit.

Whether you need to compare travel money rates across multiple providers, find the best deal on a prepaid currency card, or check prepaid multi-currency cards side by side, Comparetravelcash gives you the tools to make an informed decision in minutes. Rates change daily, and the difference between providers can be significant on larger amounts. Check the current rates at Comparetravelcash before your next trip and make sure you are not leaving money on the table.

FAQ

What is the best card to use for spending abroad?

A no-foreign-transaction-fee credit card paired with a fee-reimbursing debit card gives you the lowest overall cost. Cards like Chase Sapphire Preferred and Charles Schwab debit are frequently cited as the most cost-effective combination for international travel.

Should I use cash or card when travelling abroad?

The recommended split for developed countries is roughly 70% card and 30% cash. In cash-heavy regions, a 50/50 balance is more practical to cover markets, small vendors, and areas with limited card acceptance.

What is Dynamic Currency Conversion and why should I avoid it?

Dynamic Currency Conversion is when a foreign card terminal offers to charge you in pounds rather than the local currency. It adds 3–7% to the transaction cost and benefits the merchant’s bank. Always choose to pay in local currency.

Where is the worst place to exchange currency?

Airport currency booths and hotel exchange desks apply markups of 8–15% above the mid-market rate. Order currency in advance from a reputable provider or use a bank-affiliated ATM at your destination for a far better rate.

How much more value do loyalty points give when transferred to partners?

Points transferred to airline or hotel partners typically deliver 2 to 5 times the value of redeeming through a credit card’s own travel portal. Programmes like Flying Blue, World of Hyatt, and Avios offer some of the strongest redemption rates for UK travellers.