Foreign cash collection is defined as the banking and financial workflow used to receive, process, and manage incoming payments denominated in foreign currencies across international borders. The term covers everything from documentary collections governed by formal banking rules to the day-to-day receipt of foreign cheques and wire transfers by businesses trading internationally. In practice, the industry standard term is international cash collection or foreign receivables management, and understanding the distinction matters. Whether you are a UK exporter waiting on payment from a buyer in Germany, or an individual managing funds from abroad, the same core principles of intermediary banks, document handling, and currency conversion apply.

What is foreign cash collection and how does it work?

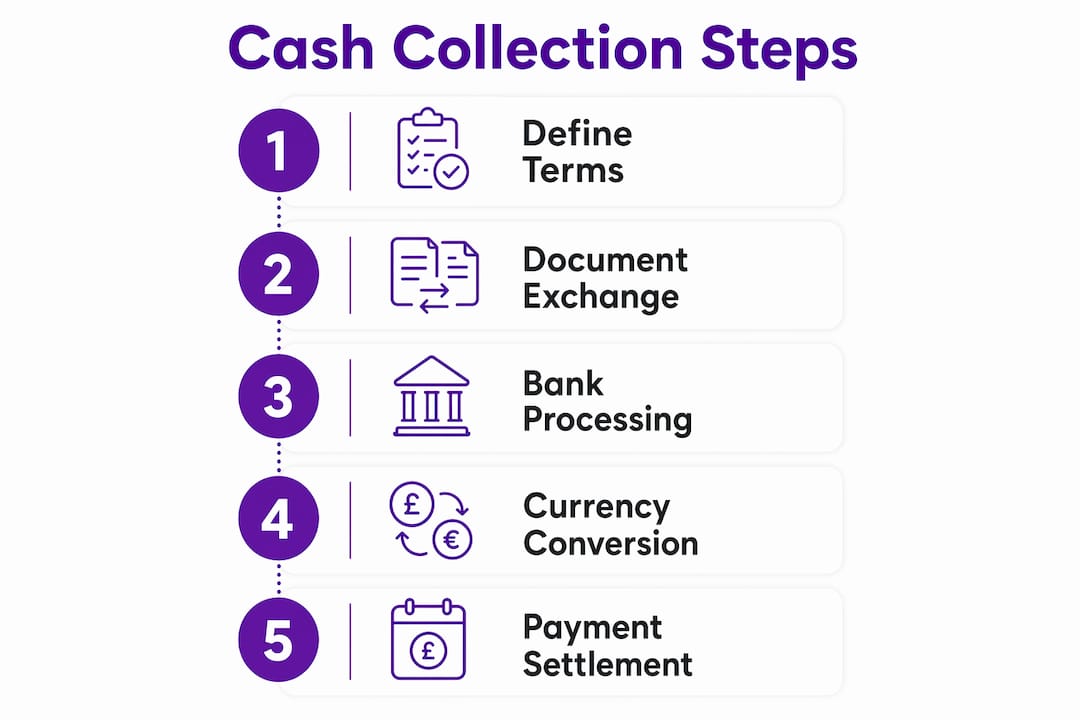

Foreign cash collection is the process by which a business or individual receives payment in a currency other than their own, typically through a bank acting as an intermediary. The bank does not simply transfer money. It manages the flow of financial documents, verifies instructions, and releases funds according to agreed terms. This places it firmly within the broader discipline of international trade finance.

The most structured form of this process is the documentary collection. Documentary collections are a bank-intermediated process in which shipping and financial documents are handled according to internationally recognised rules. Crucially, banks act as intermediaries without assuming commercial risk. That distinction is one the most commonly misunderstood aspects of the entire process.

Cross-border cash collection sits between two extremes in trade finance. Open account trading offers the buyer maximum flexibility but leaves the seller exposed. Documentary credits, such as letters of credit, offer the seller strong payment guarantees but are expensive and administratively heavy. Documentary collections occupy the middle ground, providing procedural discipline without the cost of a full letter of credit. For many businesses, this balance makes them the preferred tool for managing foreign receivables.

How foreign cash collection fits within international trade finance

The rules governing documentary collections are set out under URC 522, the Uniform Rules for Collections published by the International Chamber of Commerce. These rules define the responsibilities of the remitting bank (the seller’s bank), the collecting bank (the buyer’s bank), and the presenting bank. Every party operates within a defined role, and no bank steps outside it to guarantee payment.

This procedural framework is both a strength and a limitation. The strength is consistency. A UK exporter sending documents to a buyer in South Korea knows that both banks will follow the same rulebook. The limitation is that document discrepancies can delay payment release significantly. A mismatched invoice date, an incorrect bill of lading reference, or an ambiguous payment instruction can stall the entire collection. This is not a theoretical risk. It is one of the most frequent causes of delayed settlement in international trade.

- Documents against payment (D/P): The buyer’s bank releases shipping documents only when the buyer pays immediately. This is the lower-risk option for the seller.

- Documents against acceptance (D/A): Documents are released against the buyer’s written promise to pay at a future date. The seller carries more risk here.

- Clean collections: Financial documents such as cheques or promissory notes are sent without accompanying shipping documents. These are common in service-based transactions.

Pro Tip: Always confirm with your remitting bank exactly which documents are required before shipping goods. A single missing certificate of origin can freeze your collection for weeks.

What methods and technologies are used for foreign cash collection?

Modern foreign payment processing relies on a combination of banking infrastructure, specialist software, and correspondent bank networks. The goal in every case is the same: reduce the time between a payment being made and funds becoming available in your account.

-

Cash management systems. Platforms such as Oracle Banking Cash Management Cloud include dedicated collections modules that manage both cash and cheque receipts, track open receivables, and minimise float time. Reducing float time directly improves working capital, even when invoice values stay the same. For a business with £500,000 in outstanding foreign receivables, shaving two days off average collection time can free up tens of thousands of pounds in liquidity.

-

Correspondent bank networks. When your bank does not have a direct presence in the buyer’s country, it uses a correspondent bank to present documents and collect funds locally. This is standard practice for UK businesses trading with markets in Africa, South-East Asia, or Latin America. The correspondent bank charges a fee, which should be factored into your pricing from the outset.

-

Multi-currency receivables services. Specialist providers such as Fexco support over 20 currencies with same-day local crediting and transparent foreign exchange rates. Fexco notifies you when funds arrive and credits your account the same day, removing the uncertainty that plagues standard international wire transfers. This kind of payment certainty is particularly valuable for businesses managing cash flow across multiple markets simultaneously.

-

API-based collection agency integration. For businesses managing large volumes of overdue foreign receivables, API-based integration with external collection agencies replaces slow, error-prone file transfers with real-time status updates and automated reconciliation. Systems such as SAP FI-CA use this approach to give finance teams full visibility of every account in external collections, from submission through to final settlement.

Pro Tip: When evaluating cash management software, ask specifically about foreign currency collection modules. Generic accounts receivable tools often lack the multi-currency reconciliation features that international businesses need.

What challenges arise in collecting foreign currency payments?

The most significant challenge in international payment collection is not chasing invoices. It is navigating the legal, cultural, and regulatory differences between countries. A payment reminder that works in the UK may be legally ineffective or culturally counterproductive in Japan, Brazil, or Saudi Arabia.

- Differing legal systems. Debt recovery laws vary enormously. In some jurisdictions, a foreign creditor has limited legal standing without a local registered entity. In others, specific documentation formats are required before a court will recognise a claim.

- Currency conversion timing. When a foreign buyer pays in their local currency, the exchange rate at the moment of conversion determines your actual receipt. A payment agreed at one rate can arrive worth considerably less if settlement is delayed by weeks.

- Document discrepancies. As noted under URC 522, even minor errors in shipping or financial documents can block fund release. Businesses that prepare documentation without specialist knowledge frequently encounter avoidable delays.

- Regulatory compliance. Anti-money laundering rules, sanctions screening, and local central bank reporting requirements add layers of complexity to cross-border cash collection that domestic receivables management simply does not face.

Intrum, one of Europe’s largest credit management firms, combines local expertise across 20 countries with a global partner network covering 160 additional markets. That reach reflects how genuinely complex the local knowledge requirement is. No single business can maintain in-house expertise across every market it trades with, which is why outsourcing international collections to specialists with local presence is often the most cost-effective approach.

How can businesses optimise their foreign cash collection strategy?

Improving foreign cash flow management requires action at two distinct stages: before a payment is due and after it becomes overdue. Both stages depend on the quality of your documentation and the clarity of your payment instructions.

| Strategy | What it does | Best suited for |

|---|---|---|

| Multi-currency accounts | Receive payments in local currency without forced conversion | Businesses with regular income in 3+ currencies |

| Documentary collections (URC 522) | Structured bank intermediation with document control | Exporters shipping physical goods internationally |

| Specialist receivables services (e.g. Fexco) | Same-day crediting, transparent FX rates, payment certainty | SMEs managing foreign invoices across multiple markets |

| Local collection agency outsourcing (e.g. Intrum) | Local legal and cultural expertise for overdue accounts | Businesses with high-value or high-volume overdue foreign debt |

| API-integrated collection software (e.g. SAP FI-CA) | Real-time status tracking and automated reconciliation | Finance teams managing large external collections portfolios |

Pre-due-date discipline is where most businesses underinvest. Clear payment terms, invoices in the buyer’s local currency where possible, and explicit bank details reduce the friction that causes late payment. Post-due-date recovery is where local expertise becomes non-negotiable.

Maintaining visibility of open receivable items until final settlement is a core operational control. Receivables posted to an agency account should remain visible in your accounting system until the customer’s payment to the agency actually clears. Closing the item prematurely creates reconciliation errors that are time-consuming and costly to unwind.

Pro Tip: If you use a trade finance partner for documentary collections, request a pre-shipment document check. Most banks offer this service and it catches discrepancies before they cause delays.

For individuals managing foreign currency from abroad, the principles are simpler but the costs are just as real. Understanding how to exchange money abroad efficiently reduces unnecessary conversion losses on every transaction.

What I have learned about foreign cash collection after years in the field

The single biggest misconception I encounter is the belief that handing documents to a bank in a documentary collection means the bank will ensure you get paid. It does not. The bank will follow its instructions precisely. If those instructions are ambiguous or the documents contain errors, the bank will not improvise on your behalf. It will wait, and the clock will keep running.

The second misconception is that technology alone solves the problem. Oracle, SAP, and Fexco are excellent tools, but they amplify whatever process you feed into them. A business with poor invoice discipline will generate poor data in any system. The technology surfaces problems faster. It does not fix the underlying behaviour that creates them.

What actually works, in my experience, is combining operational discipline with the right local partners. A well-prepared invoice, sent to a buyer who has been given clear payment instructions in their own language, through a bank that has a correspondent relationship in that market, will clear faster than any amount of software applied to a poorly prepared transaction. The foreign currency providers and specialist services available today are genuinely useful. But they reward businesses that have already done the foundational work.

The final pitfall worth naming is reconciliation complacency. Once a receivable goes to an external agency, many finance teams mentally write it off. That is a mistake. Keeping the item live in your system until funds actually clear is not bureaucratic pedantry. It is the only way to know whether your collection strategy is actually working.

— Jason

Compare your foreign currency options with Comparetravelcash

Managing foreign currency does not have to mean accepting poor rates or opaque fees. Comparetravelcash is a UK-based comparison platform that helps you find the best exchange rates from providers across the country, whether you are buying travel money, managing leftover foreign cash, or looking for a prepaid multi-currency card.

From comparing travel money rates across dozens of providers to finding the best currency buyback rates when you return home, Comparetravelcash puts the information you need in one place. If you regularly handle payments in multiple currencies, a prepaid multi-currency card could reduce your conversion costs significantly. Check the latest rates and options before your next transaction.

FAQ

What is the difference between foreign cash collection and a letter of credit?

A letter of credit guarantees payment from the buyer’s bank, shifting the payment risk away from the seller. Foreign cash collection through a documentary collection does not provide this guarantee. Banks act as intermediaries only, following document release instructions under URC 522 without assuming commercial risk.

How do banks handle foreign currency cheques?

Foreign currency cheques are typically processed through correspondent bank networks, where the presenting bank clears the cheque locally and credits the remitting bank. This process can take several days, which is why cash management software that minimises float time is valuable for businesses receiving regular foreign cheques.

What is URC 522 and why does it matter?

URC 522 is the Uniform Rules for Collections published by the International Chamber of Commerce. It sets out the responsibilities of all banks involved in a documentary collection and governs how documents are handled and released. Any business using documentary collections for cross-border trade operates under these rules, whether they know it or not.

Can individuals use foreign cash collection services?

Individuals typically access simpler versions of the same process, such as receiving international wire transfers or using multi-currency accounts. Specialist receivables services like those offered by Fexco are primarily designed for businesses, but the underlying principle of receiving foreign currency payments efficiently applies equally to individuals managing funds from abroad.

What is the fastest way to collect foreign currency payments?

Specialist multi-currency receivables services, such as those provided by Fexco, offer same-day local crediting in over 20 currencies. For businesses, combining clear invoice documentation with a correspondent bank network and a cash management platform reduces collection time more reliably than any single tool alone.