Every year, UK travellers lose hundreds of pounds on currency exchange without realising it. The assumption is simple: you check the rate online, walk up to the counter, and get roughly what you expected. But what most people don’t know is that there are actually two rates in play at every exchange, and understanding the difference between them can save you a meaningful amount of money on every trip you take.

Table of Contents

- What are buy and sell rates?

- How do spread and the mid-market rate affect you?

- Common pitfalls for UK travellers at exchange counters

- Smart strategies: how to get the best buy and sell rates

- A fresh perspective: why chasing the lowest headline rate can backfire

- Find the best buy and sell rates for your next trip

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know both rates | Always check the buy and sell rates before exchanging currency to understand the true cost. |

| Watch the spread | A large gap between rates means higher costs, so compare providers and methods carefully. |

| Avoid high-fee exchanges | Airport and hotel counters usually offer the worst value with hidden fees and poor rates. |

| Use smart strategies | Pre-order online, choose fee-free cards, and check buyback rates for the best savings. |

| Timing matters | Exchange rates are often worse on weekends and holidays; plan your transaction for weekdays when possible. |

What are buy and sell rates?

When you approach any currency exchange counter, whether at a bank, a Post Office branch, or a bureau de change, you will usually see two numbers displayed. These are the buy rate and the sell rate. They look similar, but they work very differently depending on which direction the money is flowing.

Here is the simplest way to think about it:

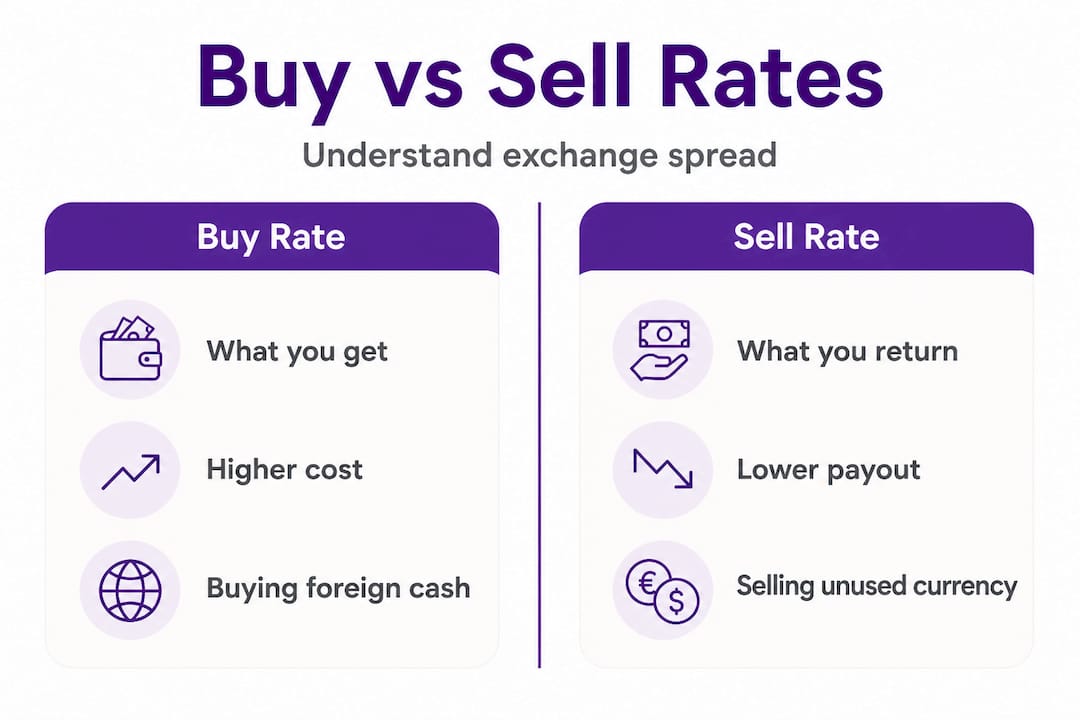

- Sell rate (offer rate): The provider sells you foreign currency. You hand over pounds, and you receive euros, dollars, or another currency. This is the rate you use before your holiday.

- Buy rate (bid rate): The provider buys foreign currency back from you. You hand over your leftover foreign notes and receive pounds in return. This is the rate you use when you return home.

As currency exchange basics confirm, the buy rate is the price at which the currency exchange provider buys foreign currency from you, while the sell rate is the price at which the provider sells foreign currency to you for travel. Both rates are always set in favour of the provider, not the customer. That is simply how the business works.

It helps to understand how foreign exchange works before you exchange a single pound. The more you know about what drives these numbers, the less likely you are to accept a poor deal without question.

“The rate you see advertised is rarely the rate that benefits you most. There are always two sides to every currency transaction, and providers are in the business of profiting from both.”

The key takeaway here is that neither the buy rate nor the sell rate is neutral. Both are intentionally set at a distance from the true market rate, and that gap is where providers make their money.

How do spread and the mid-market rate affect you?

The gap between the buy rate and the sell rate is called the spread. Think of it as the provider’s built-in margin. The wider the spread, the more you pay relative to the fair market value of the currency.

According to currency exchange forex data, the spread represents the provider’s profit margin and costs, with interbank spreads sitting far lower (around 0.1 to 1 pip) compared to retail spreads which can reach 0.5 to 2 pips for major currencies. For everyday travellers, this translates directly into less currency in your pocket.

Now, there is a third rate that rarely gets advertised: the mid-market rate. This is the midpoint sitting exactly between the buy and sell rates. It is the rate you see when you search on Google or check a currency app like XE. It represents the truest snapshot of what one currency is worth relative to another at any given moment.

The problem? You cannot buy currency at the mid-market rate at a retail counter. As forex fundamentals explain, the mid-market rate is used as a benchmark, but retail rates typically add a 2 to 5% markup via a widened spread or additional fees. For understanding the market exchange rate properly, it is worth bookmarking that benchmark so you can measure any quote against it.

Here is a practical illustration of how this plays out on a typical £1,000 exchange to euros:

| Provider type | Approx. markup | Euros received (at €1.16 mid-market) | Cost vs mid-market |

|---|---|---|---|

| Mid-market rate | 0% | €1,160 | £0 |

| Specialist online provider | 0.5% | €1,154 | £5 approx. |

| High street bank | 3.5% | €1,119 | £35 approx. |

| Airport bureau de change | 12% | €1,021 | £115 approx. |

The figures above make plain just how significant the spread can be. That airport exchange is not merely inconvenient; it is expensive in a measurable, avoidable way.

Key stat: On a £1,000 exchange, a provider with a 5% markup costs you £50 more than one with a 1% markup. Over a family holiday budget of £3,000 in foreign currency, that difference grows to £120 or more.

Common pitfalls for UK travellers at exchange counters

Knowing the theory is one thing. Recognising the traps in practice is another. Many travellers still make costly mistakes simply because they are in a rush, unprepared, or unaware of what to look out for.

Here are the most common pitfalls to avoid:

- Airport and hotel exchanges: These consistently offer the worst available rates, typically running 10 to 15% worse than competitive high street or online providers. Captive audiences mean less competition, and less competition means worse rates.

- Dynamic Currency Conversion (DCC): When a foreign ATM or card terminal asks whether you’d like to pay in pounds rather than the local currency, always choose the local currency. Accepting DCC hands the exchange calculation to the merchant’s bank, which routinely adds 3 to 6% in extra costs.

- Holiday ATM fees: Some overseas ATMs charge flat withdrawal fees on top of the rate. Using local bank ATMs rather than standalone machines in tourist areas often reduces these charges.

- Last-minute walk-ups: If you show up at any counter without a pre-ordered rate, you take whatever spread is on offer that day. These walk-up rates are nearly always worse than pre-ordered or online rates.

For practical guidance on tips for getting the best rate, planning ahead is consistently the single most effective action you can take. Those who book currency online even a few days before they travel routinely secure better rates than those who leave it to the airport.

Pro Tip: Before you travel, spend five minutes spotting bad exchange rates by comparing the quoted rate against the mid-market rate on Google. If the gap is more than 3%, keep looking.

A practical example: a family exchanging £2,000 at an airport bureau de change instead of using an online specialist could easily lose £200 or more in the spread alone. That money could pay for a decent meal out or a day trip at your destination.

Smart strategies: how to get the best buy and sell rates

Now that you can recognise the problem, the solution becomes clearer. There are several practical steps you can take to consistently secure better rates, whether you are buying currency before departure or selling leftover notes when you return.

-

Use a specialist online provider. Banks typically apply markups of 2 to 4% on exchanges, with an average of around 3.68% to USD. Specialist online providers and travel money comparison services typically operate at 0.5 to 1%, a substantial difference on larger amounts.

-

Consider a fee-free travel card. Cards such as Wise, Monzo, and Starling convert at or close to the mid-market rate, adding only a small, transparent fee. For regular travellers, these cards are among the most cost-effective ways to spend abroad without worrying about poor exchange rates at each transaction.

-

Time your exchange wisely. Spreads widen at weekends and public holidays, adding approximately 0.5 to 1% extra compared to weekday rates. The most competitive rates are available during weekday trading hours, particularly during the overlap of the London and New York markets.

-

Pre-order currency online. Locking in a rate online and collecting in branch or arranging delivery eliminates the walk-up premium. Many high street names including the Post Office and M&S offer better rates for pre-ordered currency than for over-the-counter purchases.

-

Compare before you commit. Rather than accepting the first rate you see, use a currency exchange comparison guide to see multiple providers side by side. Rate differences between providers on the same day can be significant.

Here is a summary of typical costs by method:

| Exchange method | Typical markup above mid-market | Notes |

|---|---|---|

| Fee-free travel card (Wise, Starling) | 0.35 to 0.6% | Best for regular travellers |

| Specialist online provider | 0.5 to 1% | Good for cash purchases |

| High street bureau (pre-ordered) | 1 to 2% | Improved by booking ahead |

| High street bank | 2 to 4% | Convenient but costly |

| Airport bureau de change | 8 to 15% | Worst option |

For a clear overview of the exchange process for best rates, following these steps in order will consistently produce better outcomes than reacting at the last moment.

Pro Tip: Always compare the sell-back (buy rate) before you choose a provider. A provider offering an attractive sell rate when you buy currency might offer a much worse buy rate when you return. Consider the full round-trip cost, not just one side of the transaction.

A fresh perspective: why chasing the lowest headline rate can backfire

Most currency guides tell you to find the best rate and go with it. That advice is fine as far as it goes, but it misses something important. The headline rate is only one part of the total cost picture.

Providers are aware that travellers compare headline rates. Some deliberately display competitive buy or sell rates to attract attention, then recoup margin elsewhere through flat service fees, minimum exchange requirements, or poor buyback rates. You might secure an attractive rate on the way out only to find that the same provider offers a genuinely poor buy rate when you return with leftover currency.

There is also the question of how exchange rates affect your travel budget over the full duration of your trip. A provider offering a rate that is 0.3% lower than the best on the market but charges zero fees and offers a competitive buyback rate might actually be better value across the entire journey than the apparent market leader.

The uncomfortable truth is that total value requires looking at three things together: the sell rate when you buy currency, any associated transaction or service fees, and the buy rate on offer when you exchange leftover notes afterwards. Only when you factor in all three do you get an accurate picture.

Travellers who focus purely on the day-one rate sometimes return home and sell leftover currency at a rate so poor it cancels out the savings they made at the start. Taking ten minutes to evaluate the complete offering of a provider, including their buyback terms, is a habit that pays for itself repeatedly over the years.

Find the best buy and sell rates for your next trip

Knowing how buy and sell rates work puts you firmly in the driving seat when it comes to getting more from your travel money. Putting that knowledge into action is straightforward when you have the right tools at your disposal.

CompareTravelCash.co.uk brings together live rates from dozens of providers so you can see exactly where your money goes furthest. You can compare M&S travel money rates alongside other major providers in seconds, all in one place. If you prefer the flexibility of spending abroad without carrying cash, multi-currency travel cards allow you to lock in competitive rates and avoid the worst exchange counters entirely. And when you return home with unspent foreign notes, checking the selling leftover currency buyback rates available on the platform ensures you get a fair deal on the way back too.

Frequently asked questions

Why am I quoted different rates when buying and selling currency?

Providers set separate buy and sell rates to cover their costs and make a profit, meaning the rate for buying foreign currency is always less favourable than the rate for selling it back. The gap between the two is where the provider’s margin sits.

What is the spread, and how does it impact my trip?

The spread between rates is the difference between what the provider will pay you for foreign currency and what they charge you to buy it, representing their built-in profit margin. The wider the spread, the less currency you receive for your pounds.

How can I avoid the worst exchange rates while travelling?

Airport and hotel rates are consistently 10 to 15% worse than competitive alternatives, so pre-ordering online, using fee-free travel cards, or comparing providers before you travel will always produce better results. Avoiding Dynamic Currency Conversion when paying abroad is equally important.

Why do rates change at weekends or holidays?

Weekend and holiday spreads are wider due to reduced liquidity in the currency markets, meaning providers protect themselves by increasing their margin. Exchanging during weekday business hours typically produces more competitive rates.

What’s the mid-market rate and can I get it?

The mid-market rate is the benchmark midpoint between buy and sell rates that you see on Google or XE, but retail providers add 2 to 5% on top through fees and widened spreads. Fee-free travel cards come closest to this rate, though a small fee still applies in most cases.