You return from holiday with a wallet full of euros, dollars, or dirhams, and the question hits you: what do you do with it all? Currency buyback is the answer most travellers reach for, yet surprisingly few understand how it actually works before they walk up to the counter. What is currency buyback, exactly, and are you getting a fair deal when you use it? The answers matter more than most people realise, because the gap between what you expect and what you receive can quietly cost you every single time.

Table of Contents

- What is currency buyback and how does it work?

- Practical considerations and limitations

- Understanding buyback rates and hidden costs

- Alternatives to traditional currency buyback

- My honest take on currency buyback

- Find the best buyback rates before you decide

- FAQ

What is currency buyback and how does it work?

Currency buyback is straightforward in concept. A provider buys your unused foreign banknotes and pays you back in your local currency, in this case British pounds, at a rate they set on the day. You are, in effect, selling your leftover foreign cash back into the system.

The service is offered by a wide range of providers: high street exchange bureaux, post offices, some banks, airports, and online platforms. You do not always need to have bought the currency from the same provider originally. An Post in Ireland, for example, accepts foreign currency from any source at its participating branches, which shows how accessible buyback services can be when the infrastructure is in place.

Here is how the typical currency buyback process unfolds:

- You bring your leftover foreign banknotes to a participating provider.

- The provider checks which currencies and denominations they accept.

- You are quoted a buyback exchange rate for that day.

- You complete any required paperwork or application form and present identification.

- The provider pays you in pounds, either as cash or a transfer to your account.

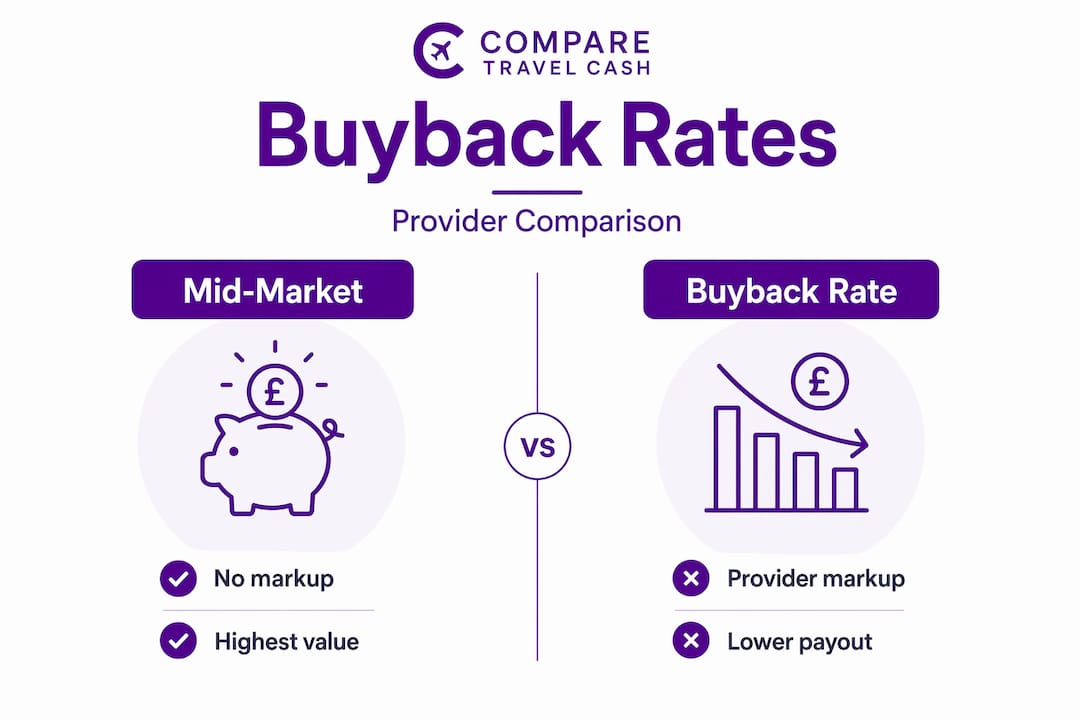

The exchange rate you receive is not the mid-market rate you see on Google or financial news sites. That figure is the true interbank rate, the midpoint between buying and selling prices on global currency markets. Buyback providers set their own sell rate, which sits below that midpoint. The difference is the spread, and it represents the provider’s margin. This is not unique to buyback. It applies whenever currency changes hands commercially. Understanding the buy/sell rate spread is central to any currency buyback explanation worth reading.

The spread varies significantly between providers. One bureau might offer you £0.85 for every euro, while another offers £0.87. On £200 worth of euros, that four-pence-per-euro gap costs you around £4.70. Small amounts feel trivial; larger sums feel less so.

Practical considerations and limitations

Currency buyback is not a universal catch-all service. Providers set their own rules, and if you walk in unprepared, you may leave disappointed. Knowing the restrictions in advance saves time and avoids wasted trips.

-

Coins are almost always refused. Coins are typically not accepted by buyback providers. This is a consistent rule across the industry. Foreign coins have lower resale value and are costly to process, so providers simply do not take them.

-

Not every currency qualifies. Providers tend to focus on the most commonly traded currencies. Major ones like US dollars, euros, Australian dollars, and Canadian dollars are widely accepted. Less common currencies, such as Thai baht or Indonesian rupiah, may only be accepted by specialist providers, if at all.

-

Denomination restrictions apply. Some providers will only accept higher-value notes and refuse smaller denominations. A bundle of low-value notes might be declined outright.

-

Identity verification is standard. Most buyback services require valid photo ID. An Post requires proof of identity and stipulates that customers must be aged 16 or over. This is now standard practice across the sector for anti-money-laundering compliance.

-

Transaction limits are real. Providers often cap how much you can sell back in a single transaction. An Post, for instance, applies a transaction cap of €500, which can affect travellers returning with larger sums. Exceeding this threshold may trigger additional verification requirements and delay the process.

-

Damaged or defaced notes may be refused. Notes that are torn, written on, or in poor condition are often rejected, regardless of their technical legal status as currency.

Pro Tip: Sort your notes from your coins and check which denominations your chosen provider accepts before you leave home. Arriving with rejected currency wastes your time and theirs.

Understanding buyback rates and hidden costs

This is where the currency buyback process gets genuinely important and where many travellers lose money without realising it.

The most misleading phrase in the currency exchange industry is “0% commission.” Providers who advertise this are not lying, but they are not telling the whole story either. Their profit comes entirely from the exchange rate itself, not from a separate fee line. The spread between the mid-market rate and the rate you receive is where the cost sits. You simply do not see it presented as a charge.

“The real cost of currency buyback is rarely the fee. It is the gap between the rate you see advertised and the rate you actually receive. That gap is the markup, and comparing it across providers is the only way to know what you are truly paying.”

Consider this practical illustration:

| Scenario | Mid-market rate (£ per €1) | Buyback rate offered | Return on €300 |

|---|---|---|---|

| Mid-market (theoretical) | 0.860 | 0.860 | £258.00 |

| Competitive provider | 0.860 | 0.845 | £253.50 |

| Airport bureau | 0.860 | 0.810 | £243.00 |

| Post office | 0.860 | 0.838 | £251.40 |

The airport bureau in this example costs you £15 more than the competitive provider for the exact same €300. That is not a fee you see on a receipt. It is simply a less favourable rate.

Exchange rates fluctuate constantly in response to supply and demand in global forex markets. This means the rate you get today may be better or worse than the rate available tomorrow. If you return from holiday and wait two weeks before selling your leftover currency, the rate may have moved against you.

Pro Tip: Do not compare providers on fees alone. Always look at the actual rate being offered and calculate what you will receive in pounds. Comparetravelcash makes this easy by showing you the real return, not just the headline rate.

Hidden markups in buyback rates are one of the most consistently overlooked costs in travel finance. The zero-commission marketing works precisely because most people do not think to question the rate itself.

Alternatives to traditional currency buyback

If the buyback rate on offer looks poor, or if your leftover currency is not accepted, you have other options worth considering.

-

Online sell-back services with locked-in rates. Some online providers let you lock in an exchange rate before you send your cash, which protects you from rate movements during the posting period. Online exchange services vary in the rates they offer, so comparing before committing is worthwhile.

-

Buyback guarantee products. Some currency providers sell a buyback guarantee at the point of purchase. One such product offers protection up to £500 for a fee of £4.95, allowing you to return leftover currency at the original purchase rate. Given that the average saving is around £20, this is worth considering for higher-value purchases where rate movements are a real concern.

-

Specialist currency brokers. For larger amounts, specialist brokers sometimes offer better sell-back rates than high street providers. They tend to have lower overheads and can price more competitively.

-

Prepaid multi-currency cards. These cards let you load specific amounts of foreign currency before you travel and spend directly from the card abroad. Because you only load what you need, leftover cash becomes much less of an issue. Any unspent balance can often be converted back or held for future trips.

-

Donate unused currency. Several charities accept foreign coins and notes that buyback services would refuse. This is not a financial return, but it is a practical and worthwhile alternative for small amounts you cannot otherwise exchange.

For a fuller breakdown of your options after travel, the leftover currency guide on Comparetravelcash covers five practical approaches worth reading before your next trip.

My honest take on currency buyback

I have spent years watching travellers make the same costly mistake: they treat buyback as an afterthought. They buy currency without a plan for what happens to whatever is left, and then accept whatever rate the first counter offers them because they just want it done.

The convenience of buyback services is real. Walking into a post office or airport bureau and leaving with pounds in your hand five minutes later is genuinely useful. But that convenience comes at a price, and the price is not always visible until you do the maths yourself.

What I have found from experience is that the travellers who get the best outcomes treat their leftover currency the same way they treat their initial purchase. They compare rates, they know which providers accept their currency, and they plan in advance rather than scrambling at the airport. It takes twenty minutes of preparation and can easily save you £20 to £40 on a typical holiday.

Buyback guarantees make sense when you are buying a large amount of currency for a longer trip and the exchange rate is volatile. Buyback guarantees provide real protection from rate shifts, but they are an upfront cost that only pays off if the market moves against you. For a short city break with modest cash needs, they are probably unnecessary.

My honest advice: decide your currency disposal strategy before you travel, not at the departure gate on the way home.

— Jason

Find the best buyback rates before you decide

If you have leftover foreign currency and want to know what it is actually worth before you walk up to any counter, Comparetravelcash does the comparison work for you.

The currency buyback comparison tool on Comparetravelcash shows you real rates from multiple providers side by side, so you can see immediately which one will put the most pounds back in your pocket. If you are also thinking ahead to your next trip, you can compare travel money rates across dozens of providers at once, or explore prepaid multi-currency cards as a way to sidestep the leftover cash problem entirely. Trusted providers, transparent rates, and no guesswork.

FAQ

What is currency buyback in simple terms?

Currency buyback is a service where a provider exchanges your unused foreign banknotes back into your local currency. You hand over the foreign cash and receive pounds at the provider’s current buyback exchange rate.

Why is the buyback rate lower than the mid-market rate?

Providers add a markup to the mid-market rate to cover their costs and generate profit. This spread means the rate you receive is always lower than the interbank mid-market rate you see quoted online.

Are coins accepted in currency buyback?

Coins are almost universally refused by buyback providers. Most services only accept banknotes, and some will also reject damaged or lower-denomination notes.

What currencies can I sell back?

Major currencies such as euros, US dollars, Australian dollars, and Canadian dollars are most widely accepted. Less common currencies may only be accepted by specialist providers, and some may not be buyable at all.

What is a buyback guarantee and is it worth it?

A buyback guarantee lets you return leftover currency at your original purchase rate, protecting you from unfavourable rate movements. It typically costs a small upfront fee and is most useful for large currency purchases or when exchange rates are particularly volatile.