Most UK travellers assume they know what they’ll pay when spending abroad. They check the exchange rate, convert a rough figure in their head, and move on. The problem is that currency conversion fees rarely work that cleanly. Hidden markups, transaction charges, and costly traps like Dynamic Currency Conversion can quietly add 3% to 12% on top of every foreign purchase. This guide exists to explain currency conversion fees properly, so you stop guessing and start making decisions that actually protect your money.

Table of Contents

- What currency conversion fees really are

- Dynamic currency conversion: the expensive “convenience”

- Comparing fees across payment methods

- Practical strategies to reduce your conversion costs

- Regulation, transparency, and what you can demand

- My honest take on currency conversion fees in 2026

- Find the best rates with Comparetravelcash

- FAQ

What currency conversion fees really are

The phrase “currency conversion fee” sounds straightforward. In practice, it covers several distinct charges that can stack on top of each other without you ever seeing a single itemised bill.

The mid-market rate is the starting point. This is the midpoint between the global buying and selling price for two currencies, the rate you see on Google or XE. No retail provider actually gives you this rate. Every bank, bureau, and card issuer adds a margin above it, and that margin is where most of the real cost lives.

Here is how the charges typically break down:

- Exchange rate markup: The gap between the mid-market rate and the rate you actually receive. Traditional banks mark up exchange rates by 2% to 5% above mid-market, costing travellers hundreds of pounds on larger transfers.

- Non-sterling transaction fee: A separate percentage charged by your bank or card issuer for processing a foreign currency payment. Standard UK bank cards charge 2.75% to 3% on top of an already marked-up rate.

- ATM withdrawal fee: A flat fee or percentage applied when withdrawing cash from a foreign cash machine, separate from the exchange rate used.

- Service or handling fee: Some bureaux charge a flat fee per transaction, regardless of the amount exchanged.

The real cost to most travellers is the poor rate spread embedded silently in prices rather than explicit fees, which most people underestimate. A card that advertises “no fees” may still embed a 3% to 5% margin inside its exchange rate. You would only spot this by comparing the rate offered against the mid-market rate at that moment.

Pro Tip: Before any major foreign transaction, check the mid-market rate on Google, then compare it against the rate your provider is offering. Any gap wider than 1.5% is worth questioning.

Dynamic currency conversion: the expensive “convenience”

Dynamic Currency Conversion, known as DCC, is one of the most expensive traps in international travel. It appears at card terminals and ATMs abroad, framed as a helpful option: would you like to pay in pounds rather than the local currency?

The answer should always be no. Here is why.

When you accept DCC, the merchant or ATM operator applies their own exchange rate rather than your card network’s rate. DCC commonly adds a 4% to 6% hidden markup at the point of transaction, making it significantly more expensive than simply paying in local currency and letting your own bank handle the conversion.

Consider a real scenario. You are at a restaurant in Barcelona. Your bill is €120. The terminal offers to charge you £108.50 in pounds. That sounds reassuring because you can see the sterling figure. But the actual mid-market equivalent of €120 might be £101.40. You are effectively paying £7.10 extra for the “convenience” of seeing a familiar currency. Multiply that across a two-week holiday and the total becomes material.

Here is how to refuse DCC confidently and consistently:

- When prompted at a card terminal, always select the local currency option, not pounds or your home currency.

- At an ATM, choose “charge in local currency” or the equivalent wording when asked.

- If the screen is confusing, use the script: say “local currency please” clearly and firmly.

- If the terminal has already defaulted to DCC, ask the staff to cancel the transaction and redo it in local currency.

- Keep your receipt. If you were charged in sterling without consent, you can raise a dispute with your card issuer.

“DCC is optional by law. You are never required to accept it. The right to pay in local currency is yours, and exercising it routinely is one of the most straightforward ways to reduce the currency conversion cost breakdown on any trip abroad.” Visa guidance on DCC

Some terminals are designed to make DCC feel like the default or the safer choice. Declining DCC requires firm communication because some machines are built to pressure acceptance and blur the distinction between home and local currency options. Stay alert.

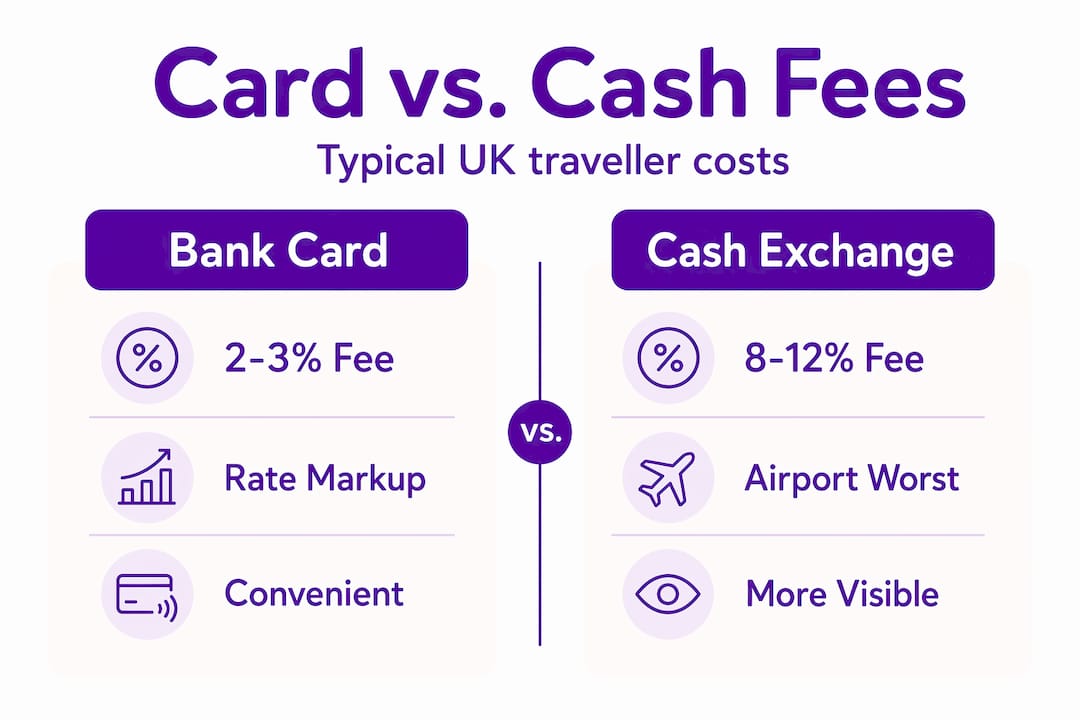

Comparing fees across payment methods

Understanding what you are charged is only half the picture. Knowing which payment method minimises those charges is where the savings actually happen.

| Payment method | Typical conversion markup | Transaction fee | Best use case |

|---|---|---|---|

| Standard UK bank card | 2% to 5% above mid-market | 2.75% to 3% | Not recommended abroad |

| Specialist travel card (e.g. Wise, Revolut) | Near mid-market | 0% on most transactions | Everyday spending abroad |

| Cash from airport bureau | 8% to 12% above mid-market | Sometimes additional | Avoid unless emergency |

| Cash from high street bureau | 2% to 4% above mid-market | May apply | Small amounts, planned ahead |

| ATM abroad with travel card | Near mid-market | Free up to a monthly limit | Cash withdrawals abroad |

Airport exchange bureaux often charge 8% to 12% above mid-market, making them consistently the worst option available. The only reason to use them is genuine urgency.

Specialist travel cards deserve a closer look. Cards from providers such as Wise or Revolut typically offer rates very close to mid-market with 0% foreign transaction fees on standard plans. However, there is one nuance worth knowing. Travel cards apply a weekend premium of around 0.5% to 1% due to currency markets being closed, so large weekend transactions will cost slightly more than weekday ones.

Explore the options available through a full types of currency providers guide if you want a deeper breakdown before your trip.

Practical strategies to reduce your conversion costs

Knowing how conversion fees work is only useful if it changes what you do. These habits make a measurable difference.

- Always pay in local currency. Refuse DCC at every terminal. Using a no-foreign-transaction-fee card and paying in local currency consistently produces the best outcome for travellers.

- Plan your ATM withdrawals. Withdrawing larger, less frequent amounts reduces the number of times any flat fees apply. Check your travel card’s free ATM withdrawal limit before you go.

- Avoid airports for cash. If you need physical cash, order it online before you travel. Rates are substantially better and delivery to your home or local branch is often free. Learn more about why to exchange money before travel for specific timing advice.

- Time large purchases on weekdays. Because timing transactions on weekdays avoids the weekend surcharge that travel card providers apply to buffer market risk, it can save a noticeable amount on bigger spends.

- Carry a backup card. A single travel card can be blocked or lost. Having a backup card on a different network (Visa vs Mastercard, for example) protects you from being stranded without payment options.

- Compare live rates before major exchanges. Before converting a large sum, check at least three providers. Rates shift daily and a better deal is rarely far away.

Pro Tip: A card marketed as “fee-free” may still embed a significant margin in its exchange rate. Always compare the rate offered against the current mid-market rate, not just the listed fees.

Regulation, transparency, and what you can demand

The UK’s Financial Conduct Authority has introduced Consumer Duty rules requiring providers to be clear and accessible in communicating costs to customers. In practice, this means any provider regulated by the FCA must present fee information in a way that a reasonable consumer can understand.

“The FCA’s Consumer Duty requires accessible cost disclosure, but it does not eliminate hidden exchange rate markups. Travellers cannot rely on regulation alone to protect them from poor-value conversion rates.” FCA Consumer Duty guidance

What this means for you is straightforward. You can and should ask any provider to explain the full cost of a transaction, including the exchange rate being applied and how it compares to mid-market. If cost disclosure is not clearly communicated, the safest assumption is that you are paying more than you need to.

Regulation sets a floor, not a ceiling. Providers can still legally embed large margins in their exchange rates as long as they disclose them. Consumer vigilance remains the most reliable protection available.

My honest take on currency conversion fees in 2026

I have spent years watching UK travellers lose money on currency conversion in ways that are entirely avoidable. The most common mistake is not DCC, though that is a close second. The most common mistake is trust. People trust that a bank they have used for decades will give them a fair rate abroad. Often it does not.

In my experience, the biggest shift in thinking comes when travellers realise the exchange rate is the fee. The explicit charge on your statement might be zero, but a 2% to 5% bank markup on a £3,000 holiday spend is between £60 and £150 quietly transferred away. That is a decent dinner in most European cities.

The specialist travel card market has matured considerably. For most holidaymakers, using a card like Wise or Revolut for day-to-day spending abroad, combined with a small amount of pre-ordered cash for places that do not accept cards, genuinely delivers a much lower cost than any traditional approach.

What I find encouraging is that the tools to make smart decisions are now more accessible than ever. Currency comparison platforms, rate alerts, and transparent fee structures exist. The cost of being uninformed has stayed the same. The cost of being informed has dropped to almost nothing. There is no good reason to keep paying more than you should.

— Jason

Find the best rates with Comparetravelcash

Now that you understand how currency exchange fees work, the next step is finding the providers who charge the least.

Comparetravelcash pulls together live rates from multiple UK travel money providers in one place, so you can see exactly who is offering the best deal before you commit. Whether you want to compare travel money rates across high street bureaux and online providers, explore the best prepaid currency card deals, or check buyback rates when you return with leftover foreign cash, the platform gives you the information you need to act with confidence. Transparent, up-to-date, and built specifically for UK travellers.

FAQ

What is a currency conversion fee?

A currency conversion fee is a charge applied when a payment is made or money is exchanged in a foreign currency. It typically includes a markup on the exchange rate, a non-sterling transaction fee, and sometimes a flat service charge.

How do I avoid currency conversion fees abroad?

Use a specialist travel card that offers 0% foreign transaction fees, always pay in local currency to refuse DCC, and avoid airport bureaux. Comparing providers before you travel using a rate comparison tool will also reduce costs significantly.

What is dynamic currency conversion and why should I avoid it?

Dynamic currency conversion (DCC) lets a foreign merchant charge you in sterling instead of local currency. It typically adds 4% to 6% to the transaction cost because the merchant applies their own unfavourable rate.

Are travel cards always better than bank cards abroad?

For most travellers, yes. Standard UK bank cards charge 2.75% to 3% non-sterling fees plus a rate markup. Specialist travel cards typically offer near mid-market rates with no transaction fee, which represents a clear saving on most foreign spending.

Do “no fee” travel cards really have zero costs?

Not always. A card with no explicit transaction fee may still embed a margin inside its exchange rate. Compare the rate offered against the mid-market rate to assess the true cost before using any card abroad.