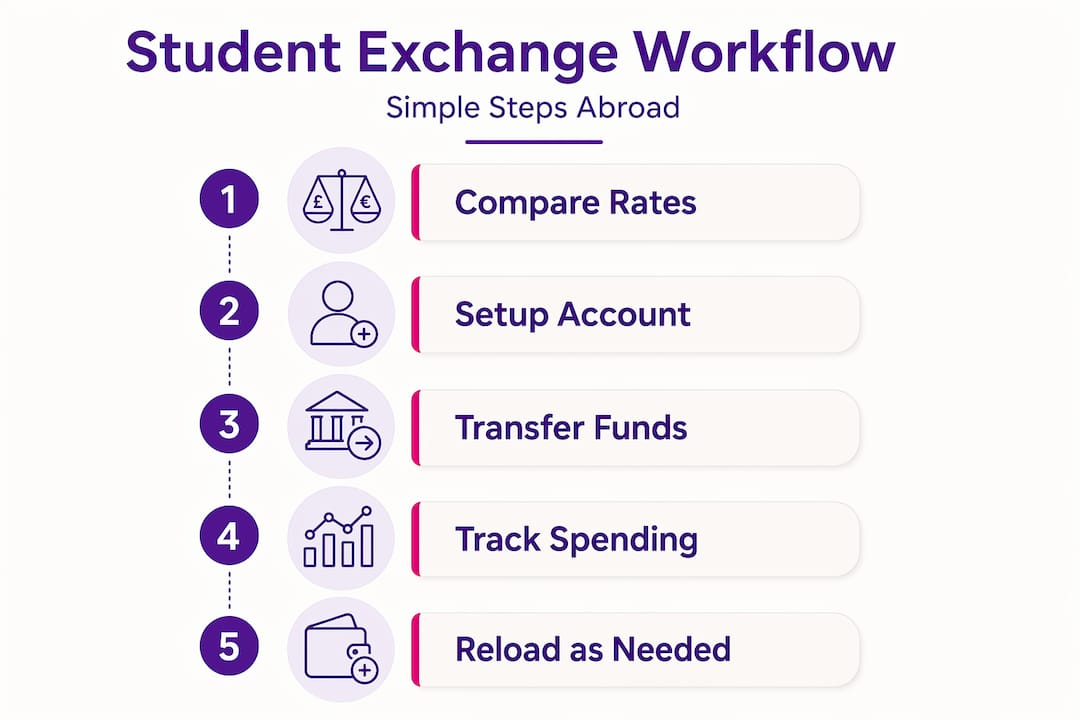

Getting your currency exchange right before studying abroad is one of the most overlooked parts of the preparation process. Students who skip this step often discover the hard way that poor exchange decisions quietly eat into their budgets. The currency exchange workflow for students is not complicated, but it does require a clear plan, the right tools, and enough lead time to act when rates are in your favour. This guide walks you through every stage, from choosing your tools before departure to managing ongoing transfers and tracking your spending throughout your studies.

Table of Contents

- Currency exchange workflow for students: tools overview

- Preparation before departure

- Executing transfers and spending abroad

- Common pitfalls in student currency exchange

- Budget verification and ongoing money management

- My honest take on student currency workflows

- Compare rates before your next transfer

- FAQ

Currency exchange workflow for students: tools overview

Before you build a workflow, you need to understand what options actually exist and which ones suit a student budget.

The most common mistake students make is defaulting to their existing high street bank. It feels familiar, but traditional banks typically charge exchange rate markups of up to 3%, plus additional transfer fees on top. For a student sending £10,000 abroad over a year, that markup alone could cost £300.

Fintech providers offer a far better starting point. Multi-currency accounts allow you to hold several currencies at once, spend locally without conversion fees, and convert funds when rates are favourable. This flexibility is genuinely useful when you are managing both tuition payments and day-to-day living costs in a foreign currency.

Here is a comparison of the main tools available to students:

| Tool | Typical fees | Best use case | Key drawback |

|---|---|---|---|

| Traditional bank transfer | 1.5–3% markup + fixed fees | Tuition payments (sometimes required) | Expensive for regular transfers |

| Wise (multi-currency account) | 0.3–0.7% fee | Regular transfers and daily spending | Limits on free ATM withdrawals |

| Revolut | Variable (free plan has limits) | Daily spending and rate alerts | Weekend rate surcharges on some plans |

| Prepaid currency card | Often “fee-free” but spreads vary | Controlled spending on a fixed budget | Hidden exchange spreads add up |

| Credit card (no FX fee) | 0% FX fee, interest if unpaid | Large purchases, fraud protection | Must pay in full each month |

| Local ATM withdrawals | 2.5–3% international fees | Emergency cash access | Fees negate rate advantages |

A few important points worth highlighting:

- Travel money cards marketed as fee-free often include hidden exchange rate spreads that end up costing more than a card with transparent fees. Read the small print before you load any funds.

- Credit cards with zero foreign transaction fees offer better fraud protection and can be cheaper for larger purchases, provided you pay the full balance each month.

- Strategically combining fintech tools covers different needs well. Use a fintech account for daily spending and a direct bank wire or specialist transfer service for large one-off payments like tuition.

Preparation before departure

A solid student currency exchange process begins several weeks before you board your flight. Leaving this until the week before departure limits your options and almost guarantees you will get a worse rate.

-

Open your fintech account at least four to six weeks early. Verification checks, card delivery, and initial KYC (know your customer) requirements can take time. Wise and Revolut both require identity verification, and some students encounter delays.

-

Order and verify your debit card, then preload a modest initial balance. You want the card active and tested before you travel. Load just enough to cover your first week of expenses.

-

Research local banking requirements in your destination country. Some universities require local bank accounts for scholarship disbursements or accommodation deposits. Find out whether you can open an account before arrival or whether you need to do it in person once there.

-

Source your arrival cash before you leave home. Pre-arrival planning should include cash for airport transport and essential first-day expenses. Order this from a reputable exchange bureau well before your departure date, and use a comparison tool to find a competitive rate rather than collecting at the airport.

-

Set up your first international money transfer in advance. Time your initial transfer for a weekday when markets are active. Avoid rushing this at the last minute.

-

Use a moving abroad budget calculator to model your year. Knowing your total expected outgoings in foreign currency helps you plan how much to transfer and when.

Pro Tip: Set a rate alert on your fintech app before you even pack your bags. Automated alerts passively capture good exchange windows better than checking rates manually each day.

Executing transfers and spending abroad

Once you arrive, the focus shifts to executing your student currency exchange process efficiently without losing money to unnecessary charges.

For tuition and large payments, use bank-to-bank wire transfers where possible. Combining a fintech account for daily spending with direct transfers for large amounts can save 1–3% in markup fees compared to running everything through a single card. On a £15,000 annual budget, that is a meaningful saving.

For regular living costs, send money in monthly batches rather than one large annual lump sum. Dollar-cost averaging your transfers smooths out exchange rate volatility. If a currency pair drops 3% in a single month, your exposure is limited to that month’s transfer rather than your entire year’s budget.

A few firm rules for day-to-day spending:

- Always pay in local currency at point of sale. Dynamic currency conversion at payment terminals can add a 3–5% markup over the standard exchange rate. When a terminal asks whether you want to pay in your home currency, always select the local option.

- Execute transfers on weekdays, Monday to Friday, to avoid weekend surcharges. Some providers apply higher rates or additional fees on Saturday and Sunday when currency markets are closed.

- Avoid airport exchange bureaux entirely. Their rates are consistently the worst available, and the convenience comes at a serious cost.

- Use ATMs strategically. International transaction fees of 2.5–3% can wipe out any rate advantage you gained from a good transfer. Use cards with worldwide ATM fee reimbursements wherever possible, and withdraw larger amounts less frequently to reduce per-transaction costs.

The single most expensive habit a student abroad can develop is making small, frequent cash withdrawals from airport or high-street ATMs using a card with foreign transaction fees. The charges accumulate faster than you expect.

Pro Tip: Monitor exchange rates through your app and schedule a larger transfer whenever rates move meaningfully in your favour. You do not need to time the market perfectly. Capturing a 1–2% improvement on a monthly transfer adds up considerably over an academic year.

Common pitfalls in student currency exchange

Even students who plan carefully make avoidable mistakes. Understanding these in advance is the most practical form of preparation.

-

“Fee-free” cards with hidden spreads. The exchange spread is the gap between the mid-market rate and the rate you actually receive. Prioritising transparency over convenience when choosing a provider protects you from cards that look cheap but quietly overcharge through the rate itself.

-

Double conversion through USD. In countries where neither your home currency nor the local currency is USD, some providers route your transaction through the US dollar first. Exchanging via USD in non-US countries leads to higher costs than direct conversion. Use specialist fintech platforms that offer direct conversion routes.

-

Large one-off transfers at the wrong time. Sending twelve months of living costs in a single transfer might feel efficient, but it exposes your entire budget to the exchange rate on one specific day. Spreading transfers across the year is a far lower-risk approach.

-

Accepting dynamic currency conversion without realising it. Some merchants default to DCC without making it obvious. Always check the terminal screen before you tap or insert your card.

-

Weekend and public holiday transfers. Currency markets are closed over weekends. Providers that still process transfers during this period apply a buffer rate that reflects their risk. You pay for that buffer.

Building a 5–10% financial buffer into your exchange budget is not excessive caution. Exchange rates can shift significantly over an academic year, and having headroom means a bad rate day never becomes a crisis.

For any overcharges you spot after the fact, contact your provider directly. Most fintech platforms have responsive customer support and will investigate disputed transactions. Keep receipts and screenshots of every significant transaction.

Reviewing your currency options using a reliable exchange options guide before you commit to any provider is always time well spent.

Budget verification and ongoing money management

Managing your budget does not stop once you arrive. The students who stay in control throughout their year abroad are the ones who check their numbers regularly.

-

Review your effective exchange rate monthly. Your fintech app will show you what rate you actually received on each transfer. Compare this against the mid-market rate on that day to understand the true cost of each transaction.

-

Use the spending analytics built into your app. Wise and Revolut both provide category breakdowns of your spending. Use these to spot patterns, not just totals. If your food budget is consistently overspent, that tells you something useful about your estimates.

-

Keep records of all significant transactions. Download monthly statements and cross-reference them against your expected fees. Errors are rare but not unheard of, particularly with international transactions routed through multiple networks.

-

Reassess your transfer schedule each term. Exchange rates shift, and a schedule you set in September may not be optimal by January. Review your approach at the start of each new term.

-

Plan your return conversion early. When your studies end, you will likely have leftover funds to convert back to sterling. Rates for buying currency back vary between providers. Checking travel money saving tips before this stage can help you recover more of your remaining budget.

Pro Tip: Set a rate alert specifically for reloading your multi-currency account when rates improve. Automated alerts mean you act on good rates even when you are busy with studies.

My honest take on student currency workflows

I have reviewed a lot of currency exchange strategies over the years, and the pattern I see most often is students over-relying on a single tool because it was the most heavily marketed to them before departure. Airline cards and branded student travel accounts are sold with convenience as the headline feature. Convenience is real. But it is also the thing providers charge you for, quietly, through spread markups rather than visible fees.

The most financially savvy students I have come across use at least two tools deliberately: one for daily transactions where low fees and good exchange rates matter most, and a separate method for large one-off transfers where even a 0.5% difference on a multi-thousand-pound payment is worth optimising.

There is also something worth saying about dynamic currency conversion that most guides understate. It is not always obvious at the point of payment. Merchants configure their terminals to default to your home currency because they receive a kickback from the conversion fee. Saying no to DCC is a skill you genuinely have to practise, because the option is sometimes buried in the terminal interface.

Finally, patience really does outperform last-minute action here. Students who set up their accounts early, configure their rate alerts, and send monthly transfers consistently end up in a significantly better financial position than those who convert large sums in a panic before a tuition deadline. The gains are not dramatic on any single transaction. They compound quietly over a full academic year.

— Jason

Compare rates before your next transfer

Planning your currency exchange well before departure is the single best financial decision you can make as a student heading abroad. Comparetravelcash makes that planning straightforward.

You can use Comparetravelcash to compare prepaid currency cards from multiple providers side by side, so you know exactly what fees and exchange spreads you are signing up for before you load a single penny. If you want a broader view of the market, the travel money comparison tool aggregates live rates from across the UK so you can act when rates are genuinely competitive. For students who need to exchange cash before departure, you can also check the latest rates from Hays Travel and similar providers to make sure you are not leaving money on the table at checkout.

FAQ

What is the best currency exchange workflow for students?

The most cost-effective approach combines a multi-currency fintech account for daily spending with direct bank-to-bank or specialist transfers for large payments like tuition. Set up accounts well before departure and schedule regular monthly transfers to reduce exposure to rate swings.

How can students avoid hidden fees when exchanging currency?

Look beyond advertised fees and check the exchange rate spread each provider applies. Cards marketed as fee-free often recoup costs through the spread. Comparing providers on a platform like Comparetravelcash shows you the true cost before you commit.

Should students use cash or a card abroad?

Cards with no foreign transaction fees are better for most daily spending. Cash remains useful for markets, small local businesses, and situations where cards are not accepted. Source your initial cash before departure from a competitive provider rather than at the airport.

What is dynamic currency conversion and why should students avoid it?

Dynamic currency conversion (DCC) is when a payment terminal converts your transaction into your home currency at the point of sale. DCC typically adds a 3–5% markup over the standard rate. Always choose to pay in local currency.

How often should students send money transfers abroad?

Monthly transfers spread throughout the academic year reduce the risk of sending your entire budget at a poor rate. Transfers scheduled across the year help protect against budget shortfalls caused by adverse currency movements.