Most UK travellers lose up to £100 per £1,000 exchanged at airports without ever realising it. The culprit is almost always the gap between the market exchange rate and the rate you actually receive. These two figures can look similar on the surface, but the difference quietly drains your holiday budget before you even board the plane. This guide explains what the market exchange rate really is, why it shifts constantly, and what practical steps you can take to get closer to it when buying travel money for your next trip.

Table of Contents

- Understanding the market exchange rate

- How market exchange rates are set and why they fluctuate

- Market rates vs. what UK travellers actually get

- How to get the best rate: practical strategies for UK travellers

- Our perspective: why most UK travellers pay more than they should

- Compare and save: find your best exchange rates now

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Market rate is the baseline | It’s the rate banks trade at, setting the true benchmark for fair exchanges. |

| Retail markups cost you | Banks, bureaus, and airports charge extra, meaning you always get less than the real rate. |

| Best rates need smart choices | Fee-free cards, specialist apps, and online orders get you closest to the market rate. |

| Timing and method matter | Avoid airports, decline DCC, and compare rates online to save the most. |

Understanding the market exchange rate

The market exchange rate is the rate at which banks and large financial institutions trade currencies with one another. You may also hear it called the spot rate, the mid-market rate, or the interbank rate. All these terms refer to the same thing: the purest, most accurate reflection of what one currency is worth relative to another at any given moment.

Here is the key point. This rate is not what you get at a bureau de change, a high street bank, or an airport kiosk. As Investopedia explains, the market exchange rate is the real-time rate at which banks trade currencies, and it is simply not accessible to everyday consumers. Every provider you deal with will add their own markup on top of it.

Think of the market rate as the wholesale price of a currency. Providers buy at or near that price, then sell to you at a higher rate. The difference is their profit margin. Understanding this distinction is the first step to making smarter decisions with your travel money.

Here is a quick summary of what the market exchange rate is and is not:

- It is the real-time rate used between major banks and financial institutions

- It is also known as the spot rate, mid-market rate, or interbank rate

- It is not the rate advertised on high street bank boards or airport screens

- It is not fixed by any government or central bank in most cases

- It is set by global supply and demand for currencies, changing by the second

“The market exchange rate is the benchmark against which all retail rates should be measured. If you do not know this figure, you cannot judge whether you are getting a fair deal or not.”

For a deeper understanding of how different rates compare, the types of exchange rates guide covers the full range you are likely to encounter when buying travel money in the UK.

How market exchange rates are set and why they fluctuate

Market exchange rates are not fixed. They move continuously, 24 hours a day, five days a week on the main trading markets, and they respond to a wide range of economic signals and global events. Understanding what drives these movements helps you make smarter timing decisions when converting a significant amount.

According to research by Stripe, market rates fluctuate continuously based on interest rates, inflation, economic growth, trade balances, and market sentiment. Each of these factors pushes and pulls at the value of currencies in real time.

Here are the five main drivers of exchange rate movement:

- Interest rates: When a central bank, such as the Bank of England, raises interest rates, the pound often strengthens because investors seek higher returns in sterling.

- Inflation data: Higher inflation can weaken a currency, as it erodes purchasing power and signals economic instability.

- Economic growth reports: Strong GDP figures tend to boost a currency’s value, while weak data can cause it to fall.

- Trade balances: Countries that export more than they import often see demand for their currency rise, pushing its value up.

- Market sentiment: Political uncertainty, elections, and global crises can trigger sharp, sudden moves that override the fundamentals entirely.

Key insight: A rate quote you receive today is a snapshot in time. It is not guaranteed, and it may look very different by tomorrow morning.

For UK travellers, this matters most when exchanging large sums. A 1% shift in the pound’s value against the euro on a £2,000 exchange means a £20 difference in what you receive. Understanding how rates affect your travel budget can help you decide when and how to lock in your travel money.

Worth knowing: Brexit-related uncertainty, Bank of England decisions, and US Federal Reserve announcements have all caused sharp sterling swings in recent years. Watching for these events before a major currency exchange is a simple, practical habit that costs you nothing.

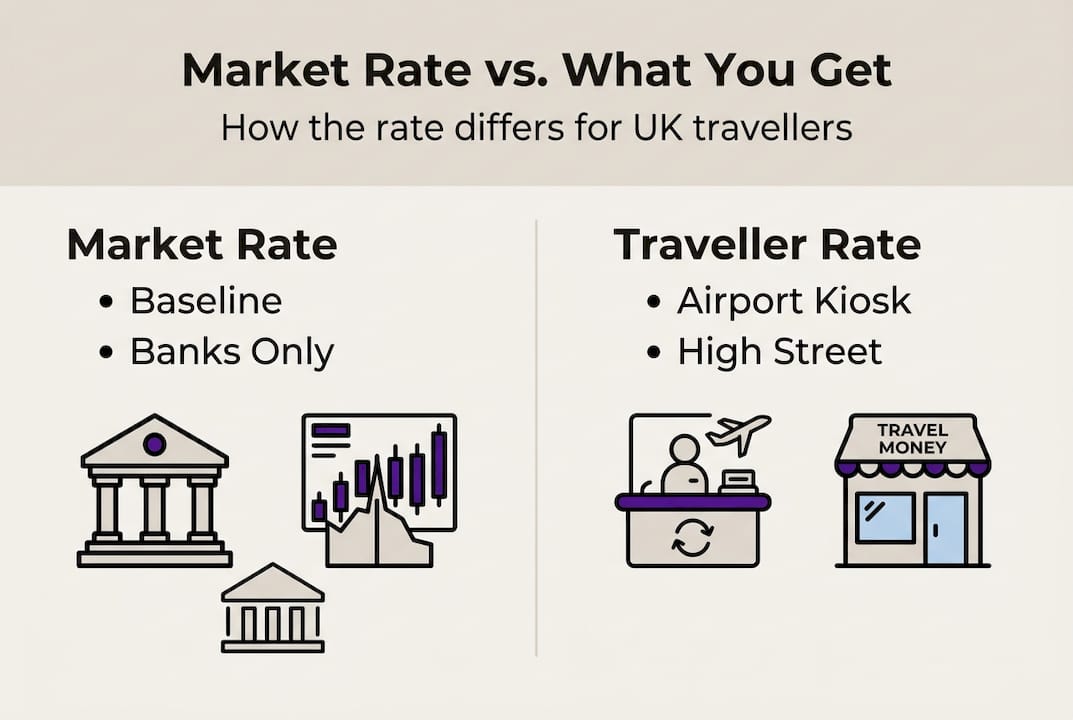

Market rates vs. what UK travellers actually get

Knowing what moves the market rate, it is time to see what this means when UK travellers actually change their money. The gap between the market rate and the retail rate you receive is where the real cost lies, and it varies enormously depending on where you exchange.

Retail rates for consumers always include a markup or spread over the market rate. The size of that markup depends on the provider. Here is how typical markups break down:

- High street banks: 3 to 4% above the market rate

- Online specialist providers: 0.8 to 1% above the market rate

- Airport kiosks: 5 to 15% above the market rate

- Hotels: Often the worst rates of all, sometimes exceeding 15%

To put this in pounds and pence, consider what happens when you exchange £1,000. Based on real-world provider comparisons, an airport exchange could cost you around £100 in lost value, a high street bank around £35, while a specialist online provider might only cost £10. That is a significant difference for doing almost the same thing.

| Provider | Typical markup | Cost on £1,000 exchange |

|---|---|---|

| Airport kiosk | 10 to 15% | £100 to £150 |

| High street bank | 3 to 4% | £30 to £40 |

| Online specialist | 0.8 to 1% | £8 to £10 |

| Fee-free travel card | 0 to 0.5% | £0 to £5 |

The table makes it clear. Convenience at the airport costs you, and it costs you a lot. Understanding why comparing exchange rates matters is the foundation of getting a good deal.

Pro Tip: Always compare the total cost of an exchange, not just the headline rate. A provider offering a slightly better rate but charging a £5 fee may still work out cheaper than a fee-free option with a worse rate. Do the maths on the full amount you intend to exchange before committing.

Also watch out for providers that advertise “0% commission” while quietly offering a far worse rate. The commission is simply baked into the exchange rate itself. Knowing the market rate before you shop is the only reliable way to see past this tactic. Learning how UK travellers get the best rates involves understanding exactly these kinds of marketing tricks.

How to get the best rate: practical strategies for UK travellers

Armed with these examples, here is how you can actually get closer to the market rate and avoid the most common traps.

The best tools available to UK travellers right now include fee-free cards and specialist apps. Fee-free cards and digital challenger banks such as Starling and Monzo offer near-interbank rates on spending abroad, with no foreign transaction fees. Wise and Revolut operate similarly, letting you convert currency at or very close to the mid-market rate, often with minimal fees on amounts up to a set limit.

Here is a practical action list:

- Use a fee-free travel card (Starling, Monzo) for day-to-day spending abroad

- Pre-load a Wise or Revolut account before you travel to lock in favourable rates

- Order cash online from providers like TravelFX or Post Office click-and-collect, which typically offer better rates than in-branch

- Avoid exchanging at airports or hotels unless it is genuinely your only option

- Always pay in local currency when abroad, not GBP. Choosing GBP triggers dynamic currency conversion (DCC)

Avoiding DCC is one of the most overlooked but impactful steps. When a card machine abroad asks whether you want to pay in pounds or the local currency, always choose the local currency. Accepting DCC hands the conversion to the merchant’s bank, which typically adds 3 to 5% on top of the rate.

Also be aware of weekend markups. Some providers apply worse rates on Saturdays and Sundays because interbank markets are closed and they carry more risk. If you can, buy your travel money during the week.

Pro Tip: Check the current mid-market rate on a currency comparison site before you buy. This gives you a benchmark to measure every quote against, so you can immediately see how much any provider is adding.

For a full breakdown of your options, exploring how to compare currency exchange options gives a structured overview of cards, cash, and apps side by side. You can also find detailed guidance on avoiding fees that many travellers simply do not know to look for.

For those who prefer a specialist view, best practices for market rates from Wise covers the London market specifically and is worth reading before any larger exchange.

Our perspective: why most UK travellers pay more than they should

Here is the honest truth. Most travellers do not overpay because they lack information. They overpay because of habit. Popping into the same high street bank you have used for years or grabbing currency at the airport because it feels convenient are decisions driven by familiarity, not value.

Traditional providers have long relied on this habit. Their marketing emphasises ease and safety, not rate transparency. The word “commission-free” sounds reassuring, but it means nothing if the rate itself is poor.

The smarter approach is a hybrid one: a fee-free card for most of your spending abroad, combined with a modest amount of pre-ordered cash for situations where cards are not accepted. This combination is widely recommended but still underused by British holidaymakers.

Timing your exchange, declining DCC, and checking rates before you buy are not complicated steps. But they add up. On a £2,000 holiday exchange, the difference between the worst and best option could be £200 or more. That is money that could fund two nights of accommodation or several good meals. Treating currency exchange as a genuine shopping decision rather than an afterthought is the single most effective shift in mindset you can make.

Compare and save: find your best exchange rates now

Understanding the market exchange rate is genuinely useful, but the next step is acting on it. The difference between knowing and doing is where most travellers lose money.

CompareTravelCash.co.uk makes it straightforward to see which providers are currently offering the best rates for your chosen currency. You can instantly compare best currency card deals for spending abroad, or check specific provider rates such as Marks and Spencer exchange rates alongside the rest of the market. Whether you want cash, a prepaid card, or a mix of both, our travel money comparisons give you a clear, side-by-side view so you can book confidently and keep more of your holiday budget where it belongs.

Frequently asked questions

How is the market exchange rate different from what I get at a bureau or bank?

The market rate is the real-time rate banks use to trade currencies with each other, but bureaux and banks always add markups and fees on top, meaning you receive a less favourable rate for consumers than the true market figure.

What factors make exchange rates change every day?

Rates move constantly due to changes in interest rates, inflation, economic data, and global events, all of which affect supply and demand. As Stripe’s research confirms, these forces act simultaneously and continuously on currency values.

How can I get the exchange rate closest to the market rate on holiday?

Use fee-free travel cards, specialist apps like Wise or Revolut, or order cash online before you travel. Avoid exchanging at airports or hotels, where market rates are furthest from what you actually receive.

Is it better to exchange money before I travel or when I arrive?

Exchanging before you travel with an online specialist provider almost always gets you better rates. Ordering cash online or click-and-collect avoids expensive airport markups entirely.

What is dynamic currency conversion, and should I accept it?

Dynamic currency conversion lets you pay in GBP when abroad, but you should always decline it. Accepting DCC typically adds 3 to 5% to your transaction, making it one of the most expensive currency mistakes a traveller can make.

Recommended

- USD exchange rate: A UK traveller’s guide 2026

- Travel money exchange: How UK travellers get the best rates

- How exchange rates affect your travel budget: UK guide

- Compare currency exchange options: a guide for UK travellers

- Foreign Exchange Services – Overseas Shipping Services – OSS World Wide Movers