Commission-free travel money is currency exchanged without an explicit commission fee charged at the point of sale, though the cost is almost always built into the exchange rate the provider offers you. The term is a marketing label, not a guarantee of low cost. UK travellers lose real money every year by taking “commission-free” at face value without checking the rate behind it. Understanding how exchange rate markups work is the single most effective step you can take before your next trip.

What is commission-free travel money and how does it actually work?

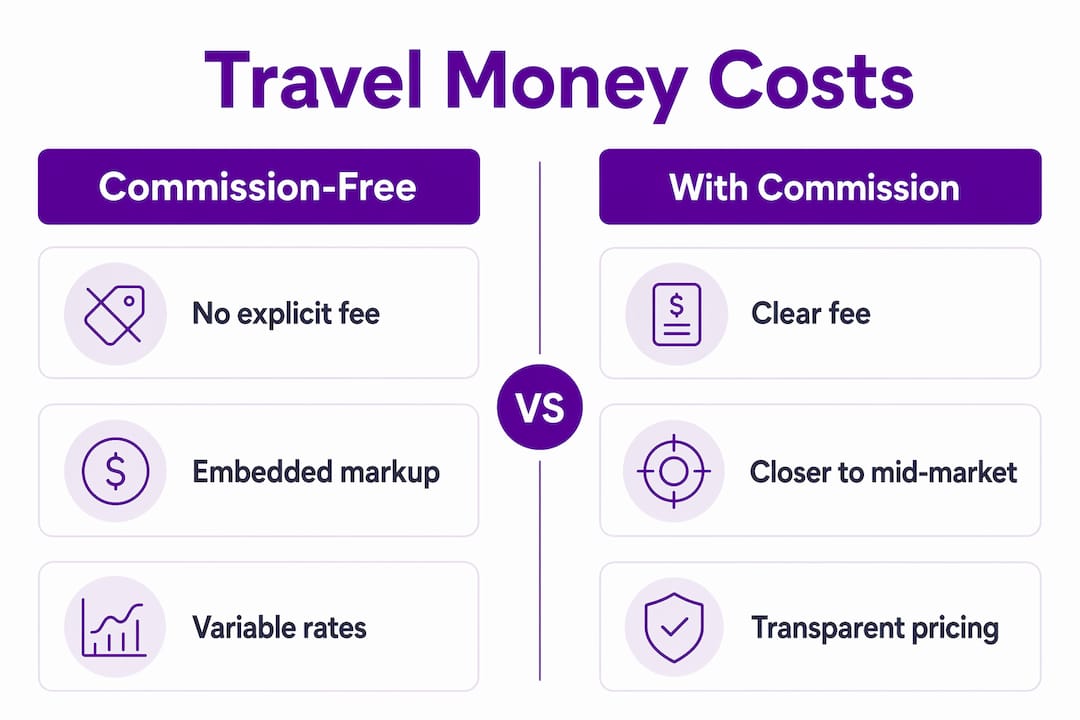

Commission-free travel money is defined as a currency exchange transaction where no separate commission line appears on your receipt. The industry term for the cost you do pay is the exchange rate margin, sometimes called the markup or spread. Providers cover their costs by offering you a rate worse than the mid-market rate, which is the real, mid-point rate between buying and selling prices on global currency markets.

Costs are embedded in the rate, not removed. A bureau de change advertising “0% commission” may still give you significantly fewer euros per pound than a specialist travel card charging the mid-market rate. The label tells you about one pricing line. It tells you nothing about the total cost.

The mid-market rate is the benchmark. Any rate worse than that is where the provider’s profit sits. The gap between the mid-market rate and the rate you receive is the true cost of your currency exchange, regardless of what the signage says.

Pro Tip: Always ask how many units of foreign currency you will receive for your specific pound amount, not whether commission is charged. That single number tells you everything.

How do hidden charges affect the real cost of your currency?

The gap between a commission-free label and actual value can be substantial. Airport bureaux typically mark up 5–15% above mid-market rates, while online currency orders usually sit 1–2% above. That difference is not trivial on a family holiday budget.

To put it in concrete terms: £500 exchanged at an airport may yield around €519, whereas a specialist travel card using near-market rates could deliver around €590 for the same amount. That is over €70 lost to a markup, with no commission charged at all.

Delivery fees add another layer. Ordering cash online for home delivery often carries a postal charge, typically waived above a minimum order. High street branches may charge a collection fee or simply offer a worse rate than their own website. Card issuers add their own layer too: standard UK debit cards often charge 2–3% in non-sterling transaction fees, which stack on top of any exchange rate margin.

The table below shows how costs compare across common channels.

| Channel | Typical markup above mid-market | Explicit commission |

|---|---|---|

| Airport bureau de change | 5–15% | Often none |

| High street branch | 3–6% | Sometimes |

| Online order (cash) | 1–2% | Rarely |

| Standard UK debit card | 2–3% (transaction fee) | None |

| Specialist travel card | 0–1% | None |

The right column looks reassuring across the board. The middle column is where the real cost lives.

What are the main travel money options for UK travellers?

UK travellers have four main categories of travel money product, each with different cost structures and practical trade-offs.

-

Cash from a bureau de change or bank. Buying physical currency is familiar and accepted everywhere. The cost depends entirely on where you buy. Online orders from reputable currency providers deliver rates 1–2% above mid-market. Airport purchases can cost 5–15% more than the mid-market rate. High street branches sit somewhere between the two.

-

Specialist travel debit and credit cards. These cards charge zero foreign transaction fees and use rates close to the mid-market rate. They are widely regarded as the most cost-efficient way to spend abroad for day-to-day purchases. Some also offer fee-free ATM withdrawals up to a monthly limit.

-

Prepaid travel money cards. You load a set amount of currency before you travel, locking in a rate at the time of loading. This protects you if the pound weakens before your trip. The trade-off is that loading fees, inactivity charges, and poor rates on unspent currency can erode the benefit. Always read the full fee schedule before loading.

-

Standard bank debit and credit cards. Convenient but expensive for most travellers. The 2–3% non-sterling transaction fee applies to every purchase and ATM withdrawal. Over a two-week holiday, that adds up to a meaningful sum.

Pro Tip: Carrying a combination of a specialist travel card for daily spending and a modest amount of local cash for markets, taxis, and small vendors gives you the best of both worlds.

How can you maximise value when using commission-free travel money?

Getting the best value from your travel money requires a few deliberate choices before and during your trip. These steps are straightforward and each one saves real money.

-

Order cash online before you travel. Online currency orders from reputable providers typically sit 1–2% above mid-market rates. That is a fraction of what airports charge. Order at least a few days before departure to allow for delivery.

-

Use a specialist travel card for card payments. Cards with no foreign transaction fees and near-market exchange rates are the cheapest way to pay by card abroad. Compare prepaid card options carefully, as fee structures vary.

-

Withdraw cash in larger amounts, less often. Withdrawing larger sums less frequently reduces the number of per-transaction fees you pay, both from your card provider and from local ATM operators. A single larger withdrawal beats four small ones every time.

-

Always pay in local currency. When a card terminal abroad asks whether you want to pay in pounds or local currency, always choose local currency. Dynamic Currency Conversion (DCC) applies a worse exchange rate than your card provider’s rate. Choosing pounds hands the conversion to the merchant, and they profit from it.

-

Lock in rates with a prepaid card when sterling is strong. If the pound is performing well against your destination currency, loading a prepaid card fixes that rate. This is a genuine benefit of prepaid products, provided you use the full balance and avoid inactivity fees.

-

Compare the final amount received, not the headline rate. Use a comparison tool to check how many euros, dollars, or dirhams you actually receive for a fixed pound amount. That figure accounts for all fees and markups in one number.

For a full breakdown of how to cut costs further, the UK traveller’s savings guide covers every major strategy in detail.

Why “commission-free” is a marketing term, not a promise of value

Most travellers misunderstand “commission-free” as meaning no cost. Providers embed their profit in the exchange rate instead. The label is technically accurate and commercially misleading at the same time.

“Commission-free travel money means no separate commission fee. It does not mean no cost. The true cost is the combined impact of any fees plus the exchange rate markup — not just the commission line.”

Several tactics make this harder to spot:

- Rate displays without context. A rate of 1.14 euros per pound looks reasonable until you know the mid-market rate is 1.19. Without that reference point, the markup is invisible.

- Minimum order thresholds. Some providers offer better rates above a certain order value, which can pressure travellers into buying more currency than they need.

- Buyback rate gaps. The rate at which a provider buys back your unused currency is almost always worse than the rate at which you bought it. That gap is another cost that never appears on a commission line.

- Card fee complexity. Some prepaid cards charge loading fees, ATM withdrawal fees, and monthly maintenance fees, none of which are commissions. Understanding all types of foreign currency fees is the only way to compare products fairly.

The only reliable comparison method is to calculate the final foreign currency amount received for a fixed sterling sum, factoring in every charge. That single number cuts through all marketing language.

My honest view on commission-free travel money after years of watching travellers get it wrong

The phrase “commission-free” has done more to confuse UK travellers than almost any other term in personal finance. I have watched people walk past genuinely good online rates to queue at an airport bureau because the sign said “0% commission.” They paid for that choice in euros they never received.

The travellers who consistently get the best value do two things. They order the bulk of their cash online a week before departure, and they carry a specialist travel card for everything else. That combination covers almost every spending scenario abroad without paying a convenience premium.

The one mistake I see repeatedly is buying currency at the airport as a backup. It feels sensible. You are already there, the rate looks acceptable, and the sign says commission-free. But airport bureaux remain the least cost-effective option precisely because they know you have no alternative at that point. Plan ahead and you will never need to use them.

Smart travellers combine cash and card strategies rather than relying on one product. Cash for small vendors and local markets, a specialist card for restaurants and shops, and a comparison tool used before departure. That is the whole system. It is not complicated, but it does require five minutes of planning before you pack.

— Jason

How Comparetravelcash helps you find genuinely good rates

Knowing what commission-free travel money really means is only half the job. The other half is finding providers who actually offer competitive rates once all costs are included.

Comparetravelcash aggregates live rates from multiple UK currency providers so you can compare the final foreign currency amount you receive for a set pound sum. That means the comparison already accounts for exchange rate margins, delivery fees, and card charges in one place. Whether you are looking for the best travel money rates before a summer holiday, checking prepaid card options, or finding the best rate to sell back unused currency via the buyback comparison tool, Comparetravelcash gives you the numbers you need to make a genuinely informed decision.

FAQ

What does commission-free travel money actually mean?

Commission-free travel money means no separate commission fee is charged at the point of exchange. The provider’s cost is recovered through the exchange rate margin instead, so the total cost depends on how far the offered rate sits below the mid-market rate.

Is commission-free travel money always cheaper?

Not necessarily. A provider charging a small explicit commission but offering a rate close to mid-market can work out cheaper than a commission-free provider with a large rate markup. Always compare the final foreign currency amount received for your pound sum.

Where is the cheapest place to get travel money in the UK?

Online currency orders from reputable providers typically offer the best rates, sitting 1–2% above mid-market rates. Airport bureaux de change are consistently the most expensive option, with markups of 5–15% above mid-market rates.

What is Dynamic Currency Conversion and why should I avoid it?

Dynamic Currency Conversion (DCC) is when a card terminal abroad offers to convert your payment into pounds at the point of sale. The conversion rate applied is almost always worse than your card provider’s rate, so you should always choose to pay in local currency.

How do I compare travel money options fairly?

Calculate the exact amount of foreign currency you receive for a fixed pound sum, such as £500, from each provider. That single figure captures all fees and rate markups together, making it the only reliable basis for comparison. Comparetravelcash does this calculation automatically across multiple providers.